|

市場調査レポート

商品コード

1750270

半導体整流器の世界市場:機会、成長促進要因、業界動向分析、予測(2025年~2034年)Semiconductor Rectifiers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 半導体整流器の世界市場:機会、成長促進要因、業界動向分析、予測(2025年~2034年) |

|

出版日: 2025年05月08日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

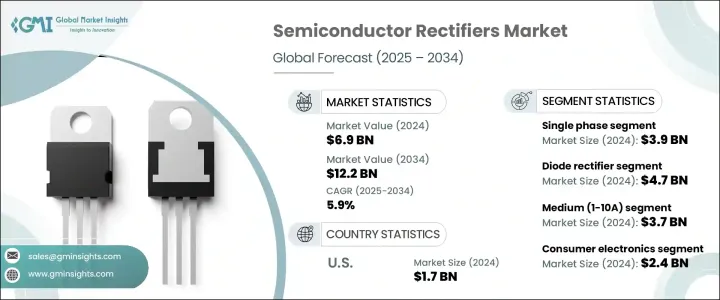

世界の半導体整流器の市場規模は、2024年に69億米ドルと評価され、2034年に122億米ドルに達するまでCAGR5.9%で成長すると予測されています。

クリーンエネルギーシステムで直流電流を生成するデバイスは交流電流への変換が必要であり、整流器はパワーインバータやコンバータで重要な役割を果たしています。

しかし、貿易政策、特にトランプ政権時代に中国から輸入される半導体部品に課された関税は、世界のサプライチェーンに大きな動揺をもたらしました。これらの関税は輸入コストを上昇させただけでなく、一貫性のない価格設定、製品展開サイクルの長期化、利益率の圧迫など、業界全体に波及効果をもたらしました。その対応策として、多くのメーカーがサプライヤーのネットワークを多様化し、リスクを最小化するためにニアショアリング戦略を模索し始めました。国内生産を活性化させ、輸入品への依存度を下げることが目的でしたが、短期的な結果としては、市場の勢いを鈍らせ、生産計画を複雑にする不安定な時期が続きました。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 69億米ドル |

| 予測金額 | 122億米ドル |

| CAGR | 5.9% |

製品セグメント別では、単相整流器セグメントは2024年に39億米ドルを生み出しました。家電や住宅セットアップにおけるその広範な使用は、低電力変換を処理する効率、コンパクトなフットプリント、標準化された回路設計への統合の容易さに起因します。その手頃な価格と柔軟性により、性能を犠牲にすることなくコストと簡便性を優先する大衆市場向け用途に理想的に適合しています。

一方、ダイオード整流器は、2024年の評価額が47億米ドルで、タイプ別ではリードしています。これらの部品は、最小限の設計と高いエネルギー効率により、幅広い低~中電力システムに不可欠であり続けています。太陽光発電インバータや電気自動車用充電器など、再生可能エネルギー発電インフラでの利用が拡大していることから、信頼性とスペース効率が要求される次世代電力ソリューションの拡大における役割が強調されています。

米国の半導体整流器の市場規模は、2024年に17億米ドルで、これは航空宇宙、防衛、通信など、高性能で長寿命の電子部品に依存する産業を支える成熟した産業基盤に起因します。このリーダーシップをさらに後押ししているのが、国産半導体製造を促進する連邦政府のインセンティブであり、これは重要技術分野における自立を強化し、地政学的な供給途絶を緩和することを目的としています。

テキサス・インスツルメンツ、オン・セミコンダクター、STマイクロエレクトロニクス、インフィニオン・テクノロジーズ、ルネサスエレクトロニクス、東芝など、半導体整流器の世界市場の主要企業は、市場での地位を強化するために多方面にわたる戦略を採用しています。これらの企業は、整流器技術の効率を高め、フォームファクターを小さくするために研究開発に投資しています。有利な貿易条件のある地域での製造能力の拡大も進行中です。ABBやNXP Semiconductorのような企業は、用途ポートフォリオを拡大するために戦略的提携を結んでおり、Microchip TechnologyやIXYSはAI統合パワーソリューションを模索しています。さらに、ローム・セミコンダクターや三菱電機のような企業は、サプライチェーンのリスクを軽減し、需要の高い分野での安定供給を確保するため、垂直統合と地理的分散に注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 主要部品の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 家電製品の需要増加

- 自動車の電動化の進展

- 再生可能エネルギーインフラの拡大

- 5Gと次世代通信ネットワーク

- データセンターとクラウドコンピューティングの急増

- 業界の潜在的リスクと課題

- 高度な整流器の初期コストが高め

- 熱管理と信頼性の問題

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別(2021年~2034年)

- 主要動向

- 単相

- 三相

第6章 市場推計・予測:タイプ別(2021年~2034年)

- 主要動向

- ダイオード整流器

- サイリスタ整流器

第7章 市場推計・予測:出力別(2021年~2034年)

- 主要動向

- 低(1A未満)

- 中(1~10A)

- 高(10A超)

第8章 市場推計・予測:最終用途産業別(2021年~2034年)

- 主要動向

- 自動車

- 家電

- 電力とユーティリティ

- ITと通信

- その他

第9章 市場推計・予測:地域別(2021年~2034年)

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- ABB

- ASI semiconductor

- Infineon technologies

- IXYS

- Microchip technology

- Mitsubishi electric

- NXP semiconductor

- ON semiconductor

- Renesas electronics

- Rohm semiconductor

- STMicroelectronics

- Taiwan semiconductor

- Texas instruments

- Toshiba

The Global Semiconductor Rectifiers Market was valued at USD 6.9 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 12.2 billion by 2034, fueled by increasing global consumption of consumer electronics and a surge in renewable energy deployment. Devices generating direct current in clean energy systems require conversion to alternating current-an area where rectifiers play a crucial role in power inverters and converters.

However, trade policies- notably the tariffs imposed on semiconductor components imported from China during the Trump administration-introduced substantial turbulence into the global supply chain. These tariffs not only increased import costs but also caused ripple effects across the industry, including inconsistent pricing, prolonged product deployment cycles, and squeezed profit margins. As a response, many manufacturers began diversifying their supplier networks and exploring nearshoring strategies to minimize risk. While the intent was to stimulate domestic production and reduce reliance on imports, the short-term consequence was a period of volatility that slowed market momentum and complicated production planning.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.9 Billion |

| Forecast Value | $12.2 Billion |

| CAGR | 5.9% |

Based on product segmentation, single-phase rectifiers segment generated USD 3.9 billion in 2024. Their extensive use in consumer electronics and residential setups stems from their efficiency in handling low-power conversions, compact footprint, and ease of integration into standardized circuit designs. Their affordability and flexibility make them an ideal fit for mass-market applications that prioritize cost and simplicity without sacrificing performance.

Meanwhile, diode rectifiers led by type with a valuation of USD 4.7 billion in 2024. These components remain integral to a broad range of low-to-mid power systems due to their minimalistic design and high energy efficiency. Their growing use in renewable energy infrastructure, including solar power inverters and electric vehicle chargers, underscores their role in scaling next-generation power solutions that demand reliability and space efficiency.

United States Semiconductor Rectifiers Market generated USD 1.7 billion in 2024, attributed to a mature industrial base that supports sectors like aerospace, defense, and telecommunications-industries that depend on high-performance and long-lasting electronic components. Further boosting this leadership are federal incentives promoting domestic semiconductor fabrication, which aim to enhance self-reliance in critical technology areas and mitigate geopolitical supply disruptions.

Key players in the Global Semiconductor Rectifiers Market, including Texas Instruments, ON Semiconductor, STMicroelectronics, Infineon Technologies, Renesas Electronics, and Toshiba, are adopting multi-pronged strategies to reinforce their market position. These companies invest in R&D to enhance efficiency and reduce form factor in rectifier technologies. Expansion of manufacturing capacities in regions with favorable trade conditions is also underway. Firms like ABB and NXP Semiconductor are entering strategic collaborations to broaden their application portfolios, while Microchip Technology and IXYS are exploring AI-integrated power solutions. Additionally, players like Rohm Semiconductor and Mitsubishi Electric focus on vertical integration and geographic diversification to mitigate supply chain risks and ensure stable delivery in high-demand sectors.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising demand for consumer electronics

- 3.3.1.2 Growing electrification of automobiles

- 3.3.1.3 Expansion of renewable energy infrastructure

- 3.3.1.4 5G and next-gen communication networks

- 3.3.1.5 Surge in data centres and cloud computing

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High initial cost of advanced rectifiers

- 3.3.2.2 Thermal management and reliability issues

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 (USD Billion & Billion Units)

- 5.1 Key trends

- 5.2 Single phase

- 5.3 Three phase

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion & Billion Units)

- 6.1 Key trends

- 6.2 Diode rectifiers

- 6.3 Thyristor rectifiers

Chapter 7 Market Estimates and Forecast, By Power Rating, 2021 - 2034 (USD Billion & Billion Units)

- 7.1 Key trends

- 7.2 Low (less than 1 A)

- 7.3 Medium (1-10 A)

- 7.4 High (over 10 A)

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion & Billion Units)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Consumer electronics

- 8.4 Power and utility

- 8.5 It and telecom

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion & Billion Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 ASI semiconductor

- 10.3 Infineon technologies

- 10.4 IXYS

- 10.5 Microchip technology

- 10.6 Mitsubishi electric

- 10.7 NXP semiconductor

- 10.8 ON semiconductor

- 10.9 Renesas electronics

- 10.10 Rohm semiconductor

- 10.11 STMicroelectronics

- 10.12 Taiwan semiconductor

- 10.13 Texas instruments

- 10.14 Toshiba