|

市場調査レポート

商品コード

1750269

トラック搭載型ナックルブームクレーンの世界市場:機会、成長促進要因、業界動向分析、予測(2025年~2034年)Truck Mounted Knuckle Boom Cranes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| トラック搭載型ナックルブームクレーンの世界市場:機会、成長促進要因、業界動向分析、予測(2025年~2034年) |

|

出版日: 2025年05月08日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

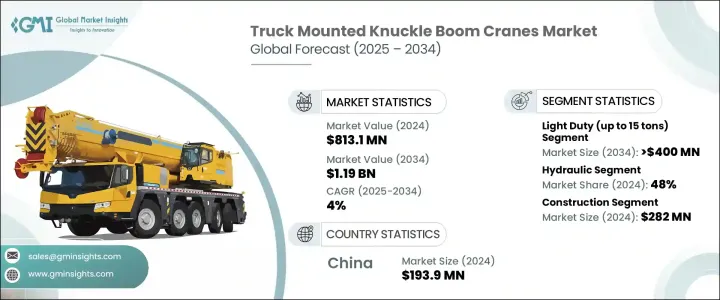

世界のトラック搭載型ナックルブームクレーンの市場規模は、2024年には8億1,310万米ドルと評価され、ユーティリティ、物流、建設など様々な分野におけるコンパクトで効率的なリフティング機器に対する需要の高まりにより、CAGR4%で成長し、2034年には11億9,000万米ドルに達すると予測されています。

これらのクレーンはトラックに搭載されるため、都市部や遠隔地のプロジェクトで高い機動性と機能性を発揮します。多関節アームの設計により、スペースに制約のある場所での機動性が向上し、現代のインフラストラクチャーや公共事業の運営に不可欠なものとなっています。

業界の自動化と合理化が進むにつれ、技術的に強化されたクレーンシステムが標準になりつつあります。遠隔操作機能、改良された荷重管理、統合された安全システムなどの機能は、現場のパフォーマンスを最適化しています。これらのツールは、生産性と作業精度を向上させながら、手作業を減らすのに役立っています。企業は、複数の作業をこなし、労働力への依存を減らすことができる多機能機械への投資を増やしており、ナックルブームクレーンの能力とよく合致しています。さらに、精密なハンドリング、リアルタイムのモニタリング、エネルギー効率の高い性能をサポートする機器に対する市場の関心も高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 8億1,310万米ドル |

| 予測金額 | 11億9,000万米ドル |

| CAGR | 4% |

2024年、小型クレーンセグメントは注目すべき40%のシェアを占め、2034年には4億米ドルに達すると予測されています。小型トラック搭載型ナックルブームクレーンは、一般的に吊り上げ能力が15トン未満で、都市開発プロジェクト、電気通信のアップグレード、自治体での作業に好んで選ばれています。そのコンパクトな構造、シンプルなセットアップ、低い運用コストは、小規模な請負業者や地方自治体にとって魅力的です。これらのクレーンは、大型の設備が実用的でない人口密集地やアクセス制限区域で特に好まれています。新興市場では、通信インフラや電化計画への投資の増加がクレーンの採用を後押ししています。

油圧駆動システムは、その強度、精度、適応性が広く認められているため、2024年のシェアは48%でした。最新のセンサーや負荷制御技術との互換性により、重量物の持ち上げ、正確な位置決め、反復作業など、要求の厳しい作業でより優れた性能を発揮することができます。ユーザーは、スムーズな操作、エネルギー使用の改善、機械的負担の軽減といったメリットを享受できるため、油圧クレーンはさまざまな用途に適しています。

中国のトラック搭載型ナックルブームクレーンの市場規模は、2024年に1億9,390万米ドルで、急速な都市拡大と大規模なインフラ投資が原動力となっています。国のインセンティブと国内の製造能力が、この地域のこの分野の力強い成長を支え続けています。同国は工業化とスマートインフラ構想を積極的に推進しており、トラック搭載型ナックルブームクレーンなどの高度なリフティングソリューションの需要に拍車をかけています。政府が支援する補助金と、物流と建設能力の強化を目的としたプロジェクトがこのセグメントを強化し、中国はこれらのクレーンの生産と消費の両方でリーダーとなっています。

市場シェアとブランドの存在感を高めるため、Palfinger、Hiab、HMF Group、Manitex Internationalなどの主要企業は、スマート安全システムやテレマティクスを統合した高度なクレーン技術に投資しています。Amco VebaやCPS Groupは、グローバルパートナーシップや現地生産戦略を通じて事業を拡大し、アクセスの向上とコスト削減を図っています。Action Construction EquipmentとMikron Hidrolikは、進化する顧客のニーズに応えるため、製品ラインの多様化に注力しています。ATLAS GroupとSANYは、高効率で軽量なクレーンを開発するための研究開発を重視し、世界市場での競争力をさらに強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- スペアパーツプロバイダー

- 製造業者

- 車両シャーシサプライヤー

- 部品および技術サプライヤー

- 販売代理店

- 最終用途

- 利益率分析

- サプライヤーの情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 戦略的な業界対応

- サプライチェーンの再構成

- 貿易への影響

- 価格設定と製品戦略

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- テレマティクスと車両管理の統合

- 油圧効率の向上

- 遠隔クレーンの操作と制御

- 荷物監視および転倒防止システム

- 新興技術

- 電動化とハイブリッド推進システム

- 自律クレーン操作

- メンテナンスとトレーニングのための拡張現実(AR)

- 先進的な材料と軽量設計

- 現在の技術動向

- 特許分析

- 規制情勢

- ユースケース

- 主なニュースと取り組み

- 価格動向

- 運転方式

- 地域

- コスト内訳分析

- 規制情勢

- 影響要因

- 促進要因

- 高度な自動化と遠隔制御システムの統合

- コンパクトで軽量な設計革新の提供

- 多機能油圧システムの開発

- 改良された負荷監視と安全機能

- 業界の潜在的リスクと課題

- 初期投資と維持費が高め

- システム統合とオペレータートレーニングの複雑さ

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:揚重能力別(2021年~2034年)

- 主要動向

- 小型(15トン以下)

- 中型(15~100トン)

- 大型(50トン超)

第6章 市場推計・予測:運転方式(2021年~2034年)

- 主要動向

- 油圧

- 電気

- ディーゼル

第7章 市場推計・予測:最終用途別(2021年~2034年)

- 主要動向

- 建設

- 物流と輸送

- ユーティリティ

- 鉱業

- 林業

- その他

第8章 市場推計・予測:流通チャネル別(2021年~2034年)

- 主要動向

- 直接販売

- 販売代理店

第9章 市場推計・予測:地域別(2021年~2034年)

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Action Construction Equipment

- Amco Veba

- ATLAS Group

- Century Cranes

- Cormach

- CPS Group

- Fassi Gru

- FURUKAWA UNIC

- Heila Cranes

- Hiab

- Hidrokon

- HMF Group

- Iowa Mold Tooling

- JomacLTD

- Manitex International

- Mikron Hidrolik

- Nandan GSE

- Palfinger

- SANY

- Xuzhou BOB-LIFT Construction Machinery

The Global Truck Mounted Knuckle Boom Cranes Market was valued at USD 813.1 million in 2024 and is estimated to grow at a CAGR of 4% to reach USD 1.19 billion by 2034, driven by rising demand for compact and efficient lifting equipment across multiple sectors such as utilities, logistics, and construction. These cranes are mounted on trucks, enabling high mobility and functionality in urban and remote project locations. Their articulated arm design allows for better maneuverability in space-constrained areas, making them indispensable in modern infrastructure and utility operations.

As industries continue to automate and streamline their processes, technologically enhanced crane systems are becoming the standard. Features like remote-control functionality, improved load management, and integrated safety systems are optimizing job site performance. These tools help reduce manual workload while increasing productivity and job accuracy. Businesses are increasingly investing in multifunctional machines that can perform multiple tasks and reduce labor dependency, aligning well with the capabilities of knuckle boom cranes. Additionally, market interest is rising for equipment that supports precision handling, real-time monitoring, and energy-efficient performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $813.1 Million |

| Forecast Value | $1.19 Billion |

| CAGR | 4% |

In 2024, the light-duty crane segment held a notable 40% share and is forecasted to reach USD 400 million by 2034. Light-duty truck-mounted knuckle boom cranes, typically with a lifting capacity under 15 tons, are the preferred choice for urban development projects, telecom upgrades, and municipal work. Their compact build, simple setup, and lower operational costs make them attractive to small contractors and local authorities. These cranes are particularly favored in densely populated or restricted-access areas where larger equipment is impractical. In emerging markets, increased investment in telecom infrastructure and electrification programs boosts their adoption.

Hydraulic-powered systems segment held a 48% share in 2024 as these systems are widely recognized for their strength, precision, and adaptability. Their compatibility with modern sensors and load-control technologies enables better performance in demanding tasks like heavy lifting, accurate positioning, and repetitive operations. Users benefit from smooth operation, improved energy usage, and reduced mechanical strain, making hydraulic cranes suitable across several applications.

China Truck Mounted Knuckle Boom Cranes Market generated USD 193.9 million in 2024, driven by rapid urban expansion and significant infrastructure investment. National incentives and domestic manufacturing capacity continue to support the strong growth of this sector in the region. The country's aggressive push for industrialization and smart infrastructure initiatives has spurred demand for advanced lifting solutions such as truck-mounted knuckle boom cranes. Government-backed subsidies and projects aimed at enhancing logistics and construction capabilities have bolstered the sector, making China a leader in both production and consumption of these cranes.

To boost market share and brand presence, leading companies like Palfinger, Hiab, HMF Group, and Manitex International are investing in advanced crane technologies with smart safety systems and telematics integration. Amco Veba and CPS Group are expanding through global partnerships and localized manufacturing strategies to enhance accessibility and reduce costs. Action Construction Equipment and Mikron Hidrolik focus on diversifying product lines to meet evolving client needs. ATLAS Group and SANY emphasize R&D to develop high-efficiency, lightweight cranes, further reinforcing their competitive positions in the global market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Spare parts providers

- 3.1.1.2 Manufacturers

- 3.1.1.3 Vehicle chassis suppliers

- 3.1.1.4 Component and Technology Suppliers

- 3.1.1.5 Distributors

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.1 Impact on trade

- 3.3 Pricing and product strategies

- 3.4 Technology & innovation landscape

- 3.4.1 Current Technological Trends

- 3.4.1.1 Telematics and fleet management integration

- 3.4.1.2 Hydraulic efficiency enhancements

- 3.4.1.3 Remote crane operation and control

- 3.4.1.4 Load monitoring and anti-tipping systems

- 3.4.2 Emerging Technologies

- 3.4.2.1 Electrification and hybrid propulsion systems

- 3.4.2.2 Autonomous crane operation

- 3.4.2.3 Augmented Reality (AR) for maintenance and training

- 3.4.2.4 Advanced materials and lightweight design

- 3.4.1 Current Technological Trends

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Use cases

- 3.8 Key news & initiatives

- 3.9 Price trend

- 3.9.1 Drive

- 3.9.2 Region

- 3.10 Cost breakdown analysis

- 3.11 Regulatory landscape

- 3.12 Impact on forces

- 3.12.1 Growth drivers

- 3.12.1.1 Integration of advanced automation and remote-control systems

- 3.12.1.2 Availability of compact and lightweight design innovations

- 3.12.1.3 Development of multi-functional hydraulic systems

- 3.12.1.4 Improved load monitoring and safety features

- 3.12.2 Industry pitfalls & challenges

- 3.12.2.1 High initial investment and maintenance costs

- 3.12.2.2 Complexity in system integration and operator training

- 3.12.1 Growth drivers

- 3.13 Growth potential analysis

- 3.14 Porter's analysis

- 3.15 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Lifting Capacity, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Light duty (up to 15 tons)

- 5.3 Medium duty (15-100 tons)

- 5.4 Heavy duty (above 50 tons)

Chapter 6 Market Estimates & Forecast, By Drive, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Hydraulic

- 6.3 Electric

- 6.4 Diesel

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Construction

- 7.3 Logistics and transportation

- 7.4 Utilities

- 7.5 Mining

- 7.6 Forestry

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Distributors

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 North America

- 9.1.1 U.S.

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Russia

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 South Korea

- 9.3.6 Southeast Asia

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 South Africa

- 9.5.2 Saudi Arabia

- 9.5.3 UAE

Chapter 10 Company Profiles

- 10.1 Action Construction Equipment

- 10.2 Amco Veba

- 10.3 ATLAS Group

- 10.4 Century Cranes

- 10.5 Cormach

- 10.6 CPS Group

- 10.7 Fassi Gru

- 10.8 FURUKAWA UNIC

- 10.9 Heila Cranes

- 10.10 Hiab

- 10.11 Hidrokon

- 10.12 HMF Group

- 10.13 Iowa Mold Tooling

- 10.14 JomacLTD

- 10.15 Manitex International

- 10.16 Mikron Hidrolik

- 10.17 Nandan GSE

- 10.18 Palfinger

- 10.19 SANY

- 10.20 Xuzhou BOB-LIFT Construction Machinery