|

市場調査レポート

商品コード

1750268

フラン系ポリマーの市場機会、成長促進要因、産業動向分析、予測、2025~2034年Furan-based Polymer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| フラン系ポリマーの市場機会、成長促進要因、産業動向分析、予測、2025~2034年 |

|

出版日: 2025年05月06日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

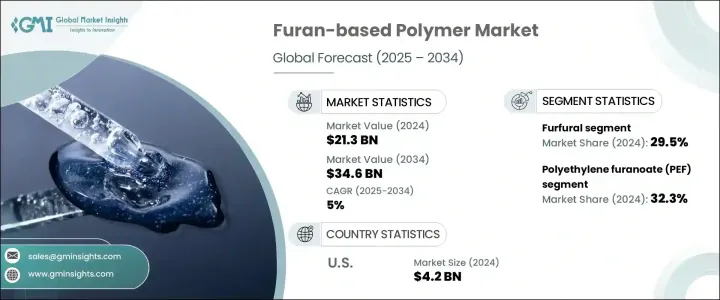

世界のフラン系ポリマー市場は、2024年に213億米ドルと評価され、5%のCAGRで成長し、2034年までに346億米ドルに達すると予測されています。

フラン系ポリマーは、主にトウモロコシの芯やサトウキビの搾りかすなどの農業残渣などの再生可能資源から生産されます。フルフラールや5-ヒドロキシメチルフルフラール(HMF)のような中間体から生産されるフラン系ポリマーは、その持続可能性と環境に優しい材料を求める世界的な動向との整合性から、人気を集めています。

フラン系ポリマーは、様々な産業、特に飲食品分野での採用が顕著で、従来の包装材料の持続可能な代替品として人気が高まっています。これらのポリマーは、農業残渣のような再生可能な資源に由来するため、石油系プラスチックに比べて環境に優しい選択肢を提供します。このポリマーの使用は、より環境に優しい製品や包装ソリューションを求める消費者や規制当局の高まりと一致しています。持続可能性に加え、フラン系ポリマーは優れた耐熱性を誇り、過酷な条件下での高い耐久性が求められる用途に最適です。鋳造セクターのような産業では、これらのポリマーは特に使用価値があります。例えば、フラン樹脂は、性能を損なうことなく高温に耐えることができるため、砂型鋳造の中子結合剤に広く使用されています。毒性が少なく、熱的性質が安定しているため、精密鋳造金属やその他の高性能用途の生産に不可欠です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 213億米ドル |

| 予測金額 | 346億米ドル |

| CAGR | 5% |

ポリエチレンフラノエート(PEF)の需要は特に強く、このポリマーセグメントの2024年のシェアは32.3%です。PEFのリサイクル性、バリア性、バイオベースの性質は、飲食品包装においてポリエチレンテレフタレート(PET)の代替品として好まれています。もう1つの注目すべき用途はコーティングと複合材料で、ポリフルフリルアルコールの耐腐食性が化学処理などの産業で安定した需要を確保しています。フランベースのポリアミドは、その耐久性、強度、熱安定性を高める能力により、自動車製造での使用が増加しており、燃費を向上させています。

市場は、5-ヒドロキシメチルフルフラール(HMF)、フルフラール、フルフリルアルコール、2,5-フランジカルボン酸(FDCA)などの誘導体でセグメント化され、フルフラールが2024年に29.5%のシェアを占め、セグメントをリードしています。フルフラールは樹脂、溶剤、潤滑油などの工業用途に幅広く使用されており、市場の要として位置づけられています。農業残渣からの生産は、再生不可能な資源への依存を減らすという、より広範なバイオエコノミーの目標に沿ったものです。

米国のフラン系ポリマー2024年の市場規模は42億米ドルでした。同国はバイオエコノミー政策、近代的バイオリファイナリーシステム、官民出資の増加に注力しており、フラン系ポリマーの成長を支援する環境が醸成されています。米国市場は、バイオベース製品の使用を奨励する米国農務省のBioPreferred Programのようなプログラムも後押ししており、持続可能なソリューションを求める産業にとって、フラン系ポリマーは競争力があり経済的に実行可能な選択肢となっています。

Avantium、Bitrez、Swicofil、Sulzer、Shengquan Groupなどの企業がフラン系ポリマー市場の最前線にいます。これらの企業は、高度なバイオリファイナリー技術への投資や再生可能ベースの材料の生産能力の拡大など、市場での存在感を高めるために様々な戦略を採用しています。AvantiumとBitrezは、バイオベースポリマーの生産規模の拡大と費用対効果の改善に注力しており、SwicofilとShengquan Groupは戦略的パートナーシップを通じて市場範囲を拡大しています。Sulzerは、さまざまな産業分野に対応する持続可能なソリューションを取り入れることで、製品ポートフォリオを強化しています。これらの企業が一体となってイノベーションを推進し、フラン系ポリマーの採用を世界的に加速しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 混乱

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国

- 主要輸入国

- 利益率分析

- 主なニュースと取り組み

- 技術の進歩と革新

- 規制情勢

- 世界のバイオ系ポリマー規制

- バイオ系材料に関する国際規格

- ASTM規格

- ISO規格

- EN規格

- 生分解性と堆肥化性基準

- 地域規制枠組み

- 環境規制

- 炭素排出量規制

- 廃棄物管理規制

- 使用済み廃棄物の規制

- 規制影響分析

- 製品開発への影響

- 市場参入障壁への影響

- 価格戦略への影響

- 影響要因

- 促進要因

- フレキシブルエレクトロニクスとウェアラブル技術の採用増加

- エネルギー貯蔵デバイス、特にスーパーキャパシタと全ポリマー電池の用途拡大

- 電気自動車の成長に伴う自動車用途での需要増加

- スマートテキスタイルとバイオメディカル用途への関心の高まり

- 業界の潜在的リスク・課題

- 原料供給の変動

- 既存のポリマーとの競合

- 規制上のハードル

- 市場機会

- 持続可能な材料への需要の高まり

- 包装業界の変革

- 政府の支援とインセンティブ

- 企業の持続可能性への取り組み

- 新たな用途開発

- 技術的進歩

- 促進要因

- 成長可能性分析

- 価格分析、2021~2034年

- 価格に影響を与える要因

- 原材料費

- エネルギーコスト

- 生産規模

- 技術の成熟度

- 市場競争

- 石油系代替品の価格設定

- 価格に影響を与える要因

- 業界の動向と最終用途の好み

- 持続可能な材料への移行

- 包装業界の動向

- 自動車業界の動向

- 建設業界の動向

- 消費財の動向

- ポーター分析

- PESTEL分析

- バリューチェーン分析

- COVID-19の市場への影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業ヒートマップ分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

- 競合情勢

- 市場集中分析

- 競争上のポジショニングと戦略

- 合併、買収、戦略的提携

- 新製品の発売とイノベーション

- マーケティングとプロモーション戦略

- 主要プレーヤーによる最近の動向と影響分析

- 企業分類

- 参加者の概要

- 財務実績

- ソースベンチマーク

第5章 市場推計・予測:タイプ別、2021~2034年

- 主要動向

- ポリエチレンフラノエート(PEF)

- ポリフルフリルアルコール(PFA)

- フラン樹脂

- ポリ(2,5-フランジメチレンサクシネート)(PFS)

- フラン系ポリエステル

- フラン系ポリアミド

- その他

第6章 市場推計・予測:誘導体別、2021~2034年

- 主要動向

- 5-ヒドロキシメチルフルフラール(HMF)

- 2,5-フランジカルボン酸(FDCA)

- フルフラール

- フルフリルアルコール

- その他

第7章 市場推計・予測:バイオマス原料別、2021~2034年

- 主要動向

- 農業残渣

- 林業残渣

- 食品廃棄物

- サトウキビ搾りかす

- トウモロコシの芯

- その他

第8章 市場推計・予測:用途別、2021~2034年

- 主要動向

- 包装

- ボトル・容器

- フィルム・ラミネート

- 食品包装

- 飲料包装

- その他

- 複合材

- 自動車用複合材

- 建設用複合材

- 航空宇宙用複合材

- 海洋複合材

- その他

- コーティング剤と接着剤

- 工業用コーティング

- 木材コーティング

- 木材製品用接着剤

- その他

- 鋳造

- 砂結合材

- 鋳型・中子製造

- その他

- 繊維

- テクニカルテキスタイル

- 衣服

- その他

- 自動車

- 内装部品

- エンジンルーム内部品

- 外装部品

- その他

- エレクトロニクス

- 回路基板

- 電子部品

- その他

- 医療・ヘルスケア

- 医療機器

- 医薬品包装

- その他

- その他

- 農業

- 消費財

- 新たな用途

- その他

第9章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- AVA Biochem

- Avantium

- Bitrez

- Globe Carbon Industries

- KANTO CHEMICAL

- Origin Materials

- Penn A Kem

- Shengquan Group

- Sulzer

- Swicofil

- TransFurans Chemicals

The Global Furan-based Polymer Market was valued at USD 21.3 billion in 2024 and is estimated to grow at a CAGR of 5% to reach USD 34.6 billion by 2034, as bio-derived polymers are primarily produced from renewable sources such as agricultural residues, including corn cobs and sugarcane bagasse. Furan-based polymers, produced from intermediates like furfural and 5-hydroxymethylfurfural (HMF), are gaining traction due to their sustainability and alignment with the global trend towards eco-friendly materials.

Furan-based polymers have seen significant adoption in various industries, especially in the food and beverage sector, where they are becoming increasingly popular as sustainable alternatives to conventional packaging materials. These polymers offer a more environmentally friendly option compared to petroleum-based plastics, as they are derived from renewable resources like agricultural residues. Their use aligns with the growing consumer and regulatory push for greener products and packaging solutions. In addition to their sustainability, furan-based polymers also boast impressive thermal resistance, making them ideal for applications that require high durability in extreme conditions. In industries like the foundry sector, these polymers are particularly valuable. Furan resins, for example, are widely used in sand casting core binding due to their ability to withstand high temperatures without compromising performance. Their minimal toxicity and stable thermal properties make them essential in the production of precision casting metals and other high-performance applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.3 Billion |

| Forecast Value | $34.6 Billion |

| CAGR | 5% |

The demand for polyethylene furanoate (PEF) is particularly strong, with this polymer segment accounting for a 32.3% share in 2024. PEF's recyclability, barrier properties, and bio-based nature make it a favorable alternative to polyethylene terephthalate (PET) in food and beverage packaging. Another notable application is in coatings and composites, where polyfurfuryl alcohol's resistance to corrosion ensures its stable demand in industries like chemical processing. Furan-based polyamides are increasingly being used in automotive manufacturing due to their durability, strength, and ability to enhance thermal stability, which in turn boosts fuel efficiency.

The market is segmented by derivatives such as 5-hydroxymethylfurfural (HMF), furfural, furfuryl alcohol, and 2,5-furandicarboxylic acid (FDCA), with furfural leading the segment, holding 29.5% share in 2024. Furfural's extensive use in industrial applications like resins, solvents, and lubricants has positioned it as a cornerstone in the market. Its production from agricultural residues aligns with the broader bioeconomy goals of reducing dependency on non-renewable resources.

United States Furan-based Polymer Market generated USD 4.2 billion in 2024. The country's focus on bioeconomy policies, modern biorefinery systems, and increasing public-private funding has fostered a supportive environment for the growth of furan-based polymers. The U.S. market is also driven by programs like the USDA's BioPreferred Program, which encourages the use of biobased products, making furan-based polymers a competitive and economically viable option for industries seeking sustainable solutions.

Companies like Avantium, Bitrez, Swicofil, Sulzer, and Shengquan Group are at the forefront of the furan-based polymer market. These companies are adopting various strategies to strengthen their market presence, including investments in advanced biorefinery technologies and expanding their production capabilities for renewable-based materials. Avantium and Bitrez are focused on scaling up the production of bio-based polymers and improving their cost-effectiveness, while Swicofil and Shengquan Group are expanding their market reach through strategic partnerships. Sulzer is enhancing its product portfolio by incorporating sustainable solutions that cater to a variety of industrial sectors. Together, these companies are driving innovation and accelerating the adoption of furan-based polymers globally.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Technological advancements and innovations

- 3.7 Regulatory landscape

- 3.7.1 Global bio-based polymers regulations

- 3.7.2 International standards for bio-based materials

- 3.7.2.1 ASTM standards

- 3.7.2.2 ISO standards

- 3.7.2.3 EN standards

- 3.7.2.4 Biodegradability and compostability standards

- 3.7.3 Regional regulatory frameworks

- 3.7.4 Environmental regulations

- 3.7.4.1 Carbon footprint regulations

- 3.7.4.2 Waste management regulations

- 3.7.4.3 End-of-life disposal regulations

- 3.7.5 Regulatory impact analysis

- 3.7.5.1 Impact on product development

- 3.7.5.2 Impact on market entry barriers

- 3.7.5.3 Impact on pricing strategies

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising adoption in flexible electronics and wearable technology

- 3.8.1.2 Expanding applications in energy storage devices, particularly supercapacitors and all-polymer batteries

- 3.8.1.3 Increasing demand in automotive applications, especially with the growth of electric vehicles

- 3.8.1.4 Growing interest in smart textiles and biomedical applications

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Feedstock supply variability

- 3.8.2.2 Competition from established polymers

- 3.8.2.3 Regulatory hurdles

- 3.8.3 Market opportunities

- 3.8.3.1 Growing demand for sustainable materials

- 3.8.3.2 Packaging industry transformation

- 3.8.3.3 Government support and incentives

- 3.8.3.4 Corporate sustainability commitments

- 3.8.3.5 Emerging applications development

- 3.8.3.6 Technological advancements

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Pricing analysis (USD/Tons) 2021 - 2034

- 3.10.1 Factors affecting pricing

- 3.10.1.1 Raw material costs

- 3.10.1.2 Energy costs

- 3.10.1.3 Production scale

- 3.10.1.4 Technology maturity

- 3.10.1.5 Market competition

- 3.10.1.6 Petroleum-based alternatives pricing

- 3.10.1 Factors affecting pricing

- 3.11 Industry trends and end use preferences

- 3.11.1 Shift towards sustainable materials

- 3.11.2 Packaging industry trends

- 3.11.3 Automotive industry trends

- 3.11.4 Construction industry trends

- 3.11.5 Consumer goods trends

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Value chain analysis

- 3.15 Impact of COVID-19 on the market

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Company heat map analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Competitive landscape

- 4.7.1 Market concentration analysis

- 4.7.2 Competitive positioning and strategies

- 4.7.3 Mergers, acquisitions, and strategic partnerships

- 4.7.4 New product launches and innovations

- 4.7.5 Marketing and promotional strategies

- 4.8 Recent developments & impact analysis by key players

- 4.8.1 Company categorization

- 4.8.2 Participant’s overview

- 4.8.3 Financial performance

- 4.9 Source benchmarking

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyethylene furanoate (PEF)

- 5.3 Polyfurfuryl alcohol (PFA)

- 5.4 Furan resins

- 5.5 Poly(2,5-furandimethylene succinate) (PFS)

- 5.6 Furan-based polyesters

- 5.7 Furan-based polyamides

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Derivatives , 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 5-Hydroxymethylfurfural (HMF)

- 6.3 2,5-Furandicarboxylic acid (FDCA)

- 6.4 Furfural

- 6.5 Furfuryl alcohol

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Biomass Feedstock Source, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Agricultural residues

- 7.3 Forestry residues

- 7.4 Food waste

- 7.5 Sugarcane bagasse

- 7.6 Corn cobs

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Packaging

- 8.2.1 Bottles and containers

- 8.2.2 Films and laminates

- 8.2.3 Food packaging

- 8.2.4 Beverage packaging

- 8.2.5 Others

- 8.3 Composites

- 8.3.1 Automotive composites

- 8.3.2 Construction composites

- 8.3.3 Aerospace composites

- 8.3.4 Marine composites

- 8.3.5 Others

- 8.4 Coatings and adhesives

- 8.4.1 Industrial coatings

- 8.4.2 Wood coatings

- 8.4.3 Adhesives for wood products

- 8.4.4 Others

- 8.5 Foundry

- 8.5.1 Sand binders

- 8.5.2 Mold and core making

- 8.5.3 Others

- 8.6 Textiles and Fibers

- 8.6.1 Technical Textiles

- 8.6.2 Apparel

- 8.6.3 Others

- 8.7 Automotive

- 8.7.1 Interior components

- 8.7.2 Under-the-hood

- 8.7.3 Exterior components

- 8.7.4 Others

- 8.8 Electronics

- 8.8.1 Circuit boards

- 8.8.2 Electronic components

- 8.8.3 Others

- 8.9 Medical and healthcare

- 8.9.1 Medical devices

- 8.9.2 Pharmaceutical packaging

- 8.9.3 Others

- 8.10 Others

- 8.10.1 Agriculture

- 8.10.2 Consumer goods

- 8.10.3 Emerging applications

- 8.10.4 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AVA Biochem

- 10.2 Avantium

- 10.3 Bitrez

- 10.4 Globe Carbon Industries

- 10.5 KANTO CHEMICAL

- 10.6 Origin Materials

- 10.7 Penn A Kem

- 10.8 Shengquan Group

- 10.9 Sulzer

- 10.10 Swicofil

- 10.11 TransFurans Chemicals