バイオハザードバッグ市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Biohazard Bags Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日

- 商品コード

- 1741042

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

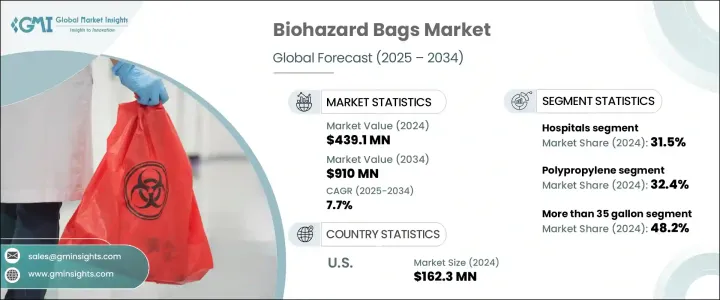

世界のバイオハザードバッグ市場は、2024年に4億3,910万米ドルと評価され、CAGR 7.7%で成長し、2034年には9億1,000万米ドルに達すると予測されています。

この成長は、安全な廃棄物処理ソリューションに対する需要の高まりと、世界の廃棄物管理プロトコルの厳格な実施によって促進されています。世界中のヘルスケアシステムは、医療廃棄物や実験室廃棄物の生産量の増加に伴い、バイオハザードバッグへの依存度を高めています。日常的な医療処置から複雑な診断検査に至るまで、バイオハザード廃棄物は大量に発生し、信頼性の高い封じ込めソリューションに対する一貫したニーズが高まっています。感染性廃棄物や有害廃棄物の安全な処理に関する規制は多くの地域で強化されており、施設は標準化されたコンプライアンスに準拠した廃棄物処理方法を採用する必要に迫られています。こうした規則は、生物学的・化学的汚染物質を安全に封じ込めるために認証バッグの使用を義務付けることで、市場の拡大を直接的に支えています。ヘルスケア・セクターだけでもこの需要に大きく貢献しており、毎日大量の汚染物が発生するため、安全に管理する必要があります。施設の近代化と拡大に伴い、乱暴な取り扱いや化学物質への暴露に耐えるバイオハザードバッグへのニーズは高まり続けています。

2024年には、容量が35ガロンを超えるバイオハザードバッグのセグメントが最大のシェアを占め、市場全体の48.2%を占める。これらの大容量バッグは、より効率的な収集と輸送を可能にするため、廃棄物の排出量が多い施設に好まれています。使用する小袋の数を減らすことで、材料費を削減できるだけでなく、物流プロセスも簡素化できます。大量の廃棄物を処理できるため、作業効率が重要な大規模事業で特に役立ちます。手術器具やPPE、実験室廃棄物など、大量の汚染物質を処理する施設では、衛生・安全基準の遵守を維持するため、このサイズのバッグに大きく依存しています。大容量バッグが広く好まれるのは、廃棄物処理を合理化し、廃棄物収集の頻度を最小限に抑えるという役割も影響しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 4億3,910万米ドル |

| 予測金額 | 9億1,000万米ドル |

| CAGR | 7.7% |

素材別に分類すると、市場はポリプロピレンベースのバッグが支配的で、2024年のシェアは32.4%を占めました。この素材は、高い耐久性、耐薬品性、圧力下での卓越した強度で支持されています。ポリプロピレン製バッグは、オートクレーブ滅菌で一般的に使用される高温に耐えることができるため、滅菌が必要な場面で特に有用です。耐薬品性に優れているため、構造上の完全性を損なうことなくバイオハザードを封じ込めるのに理想的です。非常に効果的であることに加え、このバッグは製造コストが低く、毎日大量に消費される環境でも広く使用することができます。また、穿刺や生物学的物質への暴露に対する耐性があるため、ヘルスケアや研究の現場でも使用されています。ポリプロピレンは、信頼性が高く、コンプライアンスに準拠した廃棄方法への要求が高まる中、予算重視の購買決定をサポートしながら、業界標準を満たし続けています。

最終用途の観点からは、病院が2024年に市場の31.5%を占める主要消費者に浮上しました。このような施設では常に患者が押し寄せ、様々な種類の感染性廃棄物が発生するため、厳しい規制に従って廃棄しなければならないです。使用済みの注射器、汚染された手袋、包帯、その他の医療用品などは毎日回収されるため、病院では高性能のバイオハザードバッグが不可欠となります。このような環境では、廃棄物を明確に分別し、健康リスクや環境への危険を回避するために管理する必要があります。多様な廃棄物の流れが継続的に発生するため、病院からの需要は依然として高く、それぞれが安全ガイドラインに準拠した特殊な封じ込めソリューションを必要としています。一貫性のある安全な廃棄物管理へのニーズから、病院はバイオハザードバッグ市場の数量促進要因となっています。

地域別では、米国が2024年の北米市場をリードし、約1億6,230万米ドルの収益貢献がありました。同国の包括的なヘルスケアインフラと医療廃棄物処理法の厳格な施行が、この優位性の主な要因です。国内のガイドラインは、すべてのバイオハザード物質を承認された容器で廃棄することを保証しており、病院、診療所、研究所全体の需要を押し上げています。ヘルスケア施設の数が増え続けるにつれて、信頼できる廃棄方法に対するニーズも高まっています。全国的に医療介入の頻度が高いため、安全でコンプライアンスに準拠した廃棄物管理システムへの要求がさらに高まり、バイオハザードバッグは施設全体の定番となっています。

市場競争は依然として激しく、国際的なブランドと国内ブランドが混在し、進化する廃棄物処理ニーズに合わせたソリューションを提供しています。業界大手は現在、合計で約40%の市場シェアを持ち、製品の品質、法規制への対応、価格効率で競い合っています。新興国の地元メーカーは、市場の関連性を維持するために、手頃な価格でありながら信頼性の高い製品を提供するよう、世界・プレーヤーを後押ししています。カスタマイズ、素材の革新、競争力のある価格設定が、この分野の主要プレーヤーの戦略的方向性を形成し続けると思われます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- バイオハザードバッグの需要が世界的に増加

- 効果的な廃棄物管理のための好ましい規制ガイドライン

- 特に新興諸国におけるヘルスケア産業の成長

- 業界の潜在的リスク&課題

- 医療廃棄物に関連する健康被害に関する認識の欠如

- 医療廃棄物の適切な処分に関する訓練の欠如

- 促進要因

- 成長可能性分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界バリューチェーン分析

- 原材料分析

- 規制情勢

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 競合ダッシュボード

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:容量別、2021-2034

- 主要動向

- 15ガロン未満

- 15~35ガロン

- 35ガロン以上

第6章 市場推計・予測:材質別、2021-2034

- 主要動向

- ポリプロピレン

- ポリエチレン

- プラスチック

- HDPE(高密度ポリエチレン)

- その他の素材の種類

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 研究所と研究センター

- 製薬会社およびバイオテクノロジー企業

- 診療所および診断センター

- その他の用途

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ポーランド

- スイス

- スウェーデン

- オランダ

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- インドネシア

- タイ

- ベトナム

- ラテンアメリカ

- メキシコ

- ブラジル

- メキシコ

- アルゼンチン

- チリ

- コロンビア

- ペルー

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- イラン

- イラク

- イスラエル

第9章 企業プロファイル

- Abdos Labtech

- Action Health

- Bel-Art Products

- Cole-Parmer Instrument Company

- Desco Medical

- Heathrow Scientific

- Lithey

- Medegen Medical Products

- Sharps Compliance

- Stericycle

- ThermoFisher Scientific

- Tilak Polypack

- Transcendia

- TUFPAK

- VWR International

目次

The Global Biohazard Bags Market was valued at USD 439.1 million in 2024 and is estimated to grow at a CAGR of 7.7% to reach USD 910 million by 2034. This growth is being fueled by a rising demand for secure waste disposal solutions and the implementation of strict global waste management protocols. Healthcare systems worldwide are becoming more reliant on biohazard bags as medical and laboratory waste production increases. From routine medical procedures to complex diagnostic testing, biohazardous waste is being generated in substantial quantities, driving the consistent need for reliable containment solutions. Regulations around the safe disposal of infectious and hazardous waste have tightened in many regions, compelling facilities to adopt standardized, compliant waste-handling practices. These rules directly support the market's expansion by enforcing mandatory usage of certified bags to contain biological and chemical contaminants safely. The healthcare sector alone contributes significantly to this demand, generating massive volumes of contaminated items daily that must be securely managed. As facilities modernize and expand, the need for biohazard bags that can withstand rough handling and chemical exposure continues to rise.

In 2024, the segment for biohazard bags with a capacity of more than 35 gallons held the largest share, accounting for 48.2% of the total market. These large-capacity bags are preferred by facilities with high waste output, as they allow for more efficient collection and transportation. Reducing the number of smaller bags used not only cuts material costs but also simplifies logistical processes. Their ability to handle bulk waste makes them especially useful in large-scale operations where operational efficiency is critical. Facilities producing significant volumes of contaminated material such as surgical tools used PPE, and laboratory waste rely heavily on bags of this size to maintain compliance with hygiene and safety standards. The widespread preference for larger-capacity bags is also influenced by their role in streamlining waste handling and minimizing the frequency of waste collection.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $439.1 Million |

| Forecast Value | $910 Million |

| CAGR | 7.7% |

When categorized by material, the market is dominated by polypropylene-based bags, which accounted for a 32.4% share in 2024. This material is favored for its high durability, chemical resistance, and exceptional strength under pressure. Polypropylene bags are especially useful in situations requiring sterilization, as they can withstand high temperatures commonly used in autoclaving. Their chemical resistance makes them ideal for containing biohazards without compromising structural integrity. In addition to being highly effective, these bags are cost-efficient to produce, allowing widespread use in environments where large quantities are consumed daily. Their ability to resist punctures and exposure to biological substances also makes them a go-to option for healthcare and research settings. As demands grow for reliable and compliant disposal methods, polypropylene continues to meet industry standards while supporting budget-conscious purchasing decisions.

From an end-use perspective, hospitals emerged as the leading consumers in 2024, representing 31.5% of the market. These facilities handle a constant influx of patients, generating various types of infectious waste that must be disposed of according to stringent regulations. Items such as used syringes, contaminated gloves, bandages, and other medical supplies are collected daily, making it essential for hospitals to rely on high-performance biohazard bags. In these settings, waste must be clearly segregated and managed to avoid health risks and environmental hazards. The demand from hospitals remains high due to the continuous generation of diverse waste streams, each requiring specialized containment solutions in compliance with safety guidelines. With their need for consistent, secure waste management, hospitals are the primary drivers of volume in the biohazard bags market.

In terms of regional performance, the United States led the North American market in 2024, with a revenue contribution of approximately USD 162.3 million. The country's comprehensive healthcare infrastructure and strict enforcement of medical waste disposal laws are key contributors to this dominance. Domestic guidelines ensure that all biohazardous materials are disposed of in approved containers, pushing demand across hospitals, clinics, and labs. As the number of healthcare establishments continues to grow, so does the need for dependable disposal methods. The high frequency of medical interventions across the nation further fuels the requirement for secure and compliant waste management systems, making biohazard bags a staple across facilities.

Market competition remains strong, with a mix of international and domestic brands offering tailored solutions to meet evolving waste disposal needs. Industry leaders currently hold a combined market share of about 40%, competing on product quality, regulatory compliance, and price efficiency. Local manufacturers in emerging economies are pushing global players to provide affordable yet reliable products to retain market relevance. Customization, material innovation, and competitive pricing will continue to shape the strategic direction of key players in this sector.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for biohazard bags globally

- 3.2.1.2 Favorable regulatory guidelines for effective waste management

- 3.2.1.3 Growing healthcare industry especially in developing countries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of awareness regarding health hazards associated with medical waste

- 3.2.2.2 Lack of training for proper disposal of medical waste

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on the Industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Industry value chain analysis

- 3.6 Raw material analysis

- 3.7 Regulatory landscape

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive dashboard

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Capacity Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Less than 15 gallon

- 5.3 15 to 35 gallon

- 5.4 More than 35 gallon

Chapter 6 Market Estimates and Forecast, By Material Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Polypropylene

- 6.3 Polyethylene

- 6.4 Plastic

- 6.5 HDPE (high-density polyethylene)

- 6.6 Other material types

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Laboratories and research centers

- 7.4 Pharmaceutical and biotech companies

- 7.5 Clinics and diagnostic centers

- 7.6 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Poland

- 8.3.7 Switzerland

- 8.3.8 Sweden

- 8.3.9 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Indonesia

- 8.4.7 Thailand

- 8.4.8 Vietnam

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Mexico

- 8.5.4 Argentina

- 8.5.5 Chile

- 8.5.6 Colombia

- 8.5.7 Peru

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Iran

- 8.6.5 Iraq

- 8.6.6 Israel

Chapter 9 Company Profiles

- 9.1 Abdos Labtech

- 9.2 Action Health

- 9.3 Bel-Art Products

- 9.4 Cole-Parmer Instrument Company

- 9.5 Desco Medical

- 9.6 Heathrow Scientific

- 9.7 Lithey

- 9.8 Medegen Medical Products

- 9.9 Sharps Compliance

- 9.10 Stericycle

- 9.11 ThermoFisher Scientific

- 9.12 Tilak Polypack

- 9.13 Transcendia

- 9.14 TUFPAK

- 9.15 VWR International

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 140 Pages

- 納期

- 2~3営業日