|

市場調査レポート

商品コード

1741022

カーシェアリングテレマティクスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Car Sharing Telematics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| カーシェアリングテレマティクスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月28日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

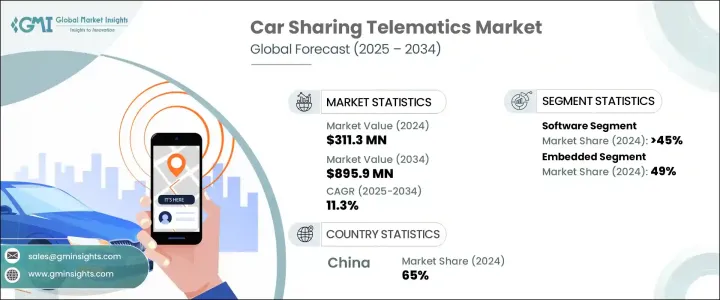

カーシェアリングテレマティクスの世界市場規模は、2024年に3億1,130万米ドルとなり、CAGR11.3%で成長し、2034年までには8億9,590万米ドルに達すると予測されています。

市場は、モビリティランドスケープの再構築を目指した革新的な戦略でこの分野に参入する企業の増加により、勢いを増しています。環境悪化や交通渋滞に対する懸念の高まりが、従来の自動車所有から共有車両モデルへのシフトに拍車をかけています。都市住民は、道路を走る車の数を減らすだけでなく、二酸化炭素排出量の削減と交通流の緩和に貢献する、持続可能な代替交通手段に対する認識を深めています。自治体は、グリーン交通政策や排出削減目標を実施することで、こうした変化を促し、シェアモビリティ事業者に電気自動車の導入を促しています。この移行は、都市インフラの最適化と環境負荷の低減を目指す、より広範なスマートシティイニシアチブと一致しています。

デジタル化され環境に配慮した輸送の推進は、テレマティクスシステムの設計と導入方法に大きな影響を及ぼしています。カーシェアリングが主流になるにつれ、テレマティクスソフトウェアが最も重要なコンポーネントとして台頭し、自動車をコネクテッドデータハブに変貌させています。2024年には、ソフトウェア分野が市場シェア全体の45%以上を占め、予測期間中も大幅な成長が見込まれています。これらのプラットフォームにより、事業者は車両性能の追跡、メンテナンススケジュールの監視、ユーザー行動の分析、車両全体の効率改善を行うことができます。テレマティクスソフトウェアに人工知能が採用されたことで、システムはリアルタイムの需要に基づいて車両サイズを動的に調整できるようになり、運用コストの削減とサービス品質の向上が可能になりました。キーレスビークルエントリー、リモートロック、課金自動化、ユーザーフレンドリーなインターフェースなどの機能はすべて、高度なソフトウェア機能から生まれています。同時に、アップグレードされた暗号化プロトコルとクラウドベースのインフラにより、データ保護とサイバーセキュリティが確保され、プラットフォームはより堅牢で、規制基準に準拠しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 3億1,130万米ドル |

| 予測金額 | 8億9,590万米ドル |

| CAGR | 11.3% |

市場をコンポーネント別に分類すると、GPSレシーバー、加速度計、エンジンインターフェースモジュール、SIMカード、ソフトウェアが含まれます。これらのコンポーネントが連携することで、シームレスな接続性と正確な分析が可能になります。ソフトウェアの重要性は引き続きリードしており、車両管理者にリアルタイムの可視性と運行管理を提供しています。クラウドネットワークと統合することで、ソフトウェアモジュールは、ユーザー認証、ジオフェンシング、予測診断などの高度な機能も可能にし、安全性を確保し、車両の稼働率を最大化します。

市場はまた、形態別に組み込み型、テザリング型、統合型テレマティクスに区分されます。2024年の市場シェアは組み込み型が49%を占め、予測期間中は組み込み型が優位を占めると予想されます。これらのシステムは、メーカーが車両に直接取り付け、その電子機器に深く組み込まれています。組み込みシステムの統合レベルは、車両とバックエンドシステム間の即時データ転送を可能にし、リアルタイムの性能洞察とリモートコントロール機能を促進します。車両のコネクティビティに対する要求が高まる中、組み込みシステムはカーシェアリングプログラムの業界標準になりつつあります。

ビジネスモデルの観点からは、サブスクリプションベースモデルが主要セグメントとして際立っています。都市部のユーザーがこのモデルを好むのは、予測可能な月額または年額料金で車両フリートへの一貫したアクセスを提供するためです。このアプローチは、透明で予算に見合った価格設定を提供し、自動車所有の煩わしさを解消することで、長期的なユーザーエンゲージメントをサポートします。このモデルで事業を展開する企業は、サービスの信頼性により高い顧客維持率を享受しています。

地域別では、アジア太平洋が2024年の市場をリードし、中国が地域市場シェアの約65%を占め、7,420万米ドルの売上を計上しました。中国の主導的地位は、急速な都市化、広範な自動車生産能力、コネクテッドビークルインフラの技術的進歩によってもたらされました。スマートモビリティと車両電化の促進を目的とした国家開発政策により、共有電気自動車やハイブリッド車へのテレマティクスシステムの広範な展開が可能になりました。さらに、5Gネットワーク、クラウドコンピューティング、モノのインターネット(IoT)プラットフォームへの投資が、高度なカーシェアリングエコシステムの拡大を支えています。バッテリー管理システム、AIベースの車両追跡、リアルタイムの車両分析が共有モビリティサービスに統合され、日本はこの分野の世界リーダーとなっています。

世界のカーシェアリングテレマティクス業界を形成する主要プレーヤーには、リアルタイム追跡、行動分析、予知保全技術のプロバイダーが含まれます。これらのシステムは現在、高度なセンサーアレイ、集中制御ユニット、国境を越えたデータ交換とクラウドベースの診断を提供する5G対応eSIMを特徴としています。市場の進化は、都市のライフスタイルと持続可能性の目標に合わせた、よりスマートで安全、かつ効率的な輸送ソリューションへのニーズによって牽引され続けています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 カーシェアリングテレマティクスの業界考察

- 業界エコシステム分析

- サプライヤーの情勢

- 部品供給業者

- 自動車メーカー

- テクノロジープロバイダー

- システムインテグレーター

- 最終用途

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(顧客へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 成長促進要因

- 運輸業界におけるIoTとAIの統合

- 持続可能な輸送手段への需要の高まり

- シェアードモビリティを促進する支援的な規制と政府の取り組み

- 業界の潜在的リスク・課題

- データプライバシーに関する懸念

- 多額の初期費用と継続費用

- 成長促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:サービス別、2021年~2034年

- 主要動向

- 自動衝突通知(ACN)

- 緊急時対応

- ナビゲーション

- アシスタンス・アクセス

- 診断

- 車両管理

- 請求

- その他

第6章 市場推計・予測:形態別、2021年~2034年

- 主要動向

- 埋め込み型

- テザリング型

- 統合型

第7章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- GPS受信機

- 加速度計

- エンジンインターフェース

- SIMカード

- ソフトウェア

- その他

第8章 市場推計・予測:ビジネスモデル別、2021年~2034年

- 主要動向

- サブスクリプションモデル

- 従量課金モデル

- 企業の車両管理

- OEMとのパートナーシップ

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- CalAmp

- cambio Mobilitatsservice

- Cantamen

- Carmine

- Citiz Reseau

- CityBee Solutions

- Continental Aftermarket &Services

- Fleetster(Next Generation Mobility)

- Geotab

- INVERS

- Mobility Tech Green

- Mojio

- Octo Group

- Ridecell

- Samsara

- Targa Telematics

- Turo

- Verizon Communications

- Vulog

- WeGo

The Global Car Sharing Telematics Market was valued at USD 311.3 million in 2024 and is estimated to grow at a CAGR of 11.3% to reach USD 895.9 million by 2034. The market is gaining momentum due to the increasing number of companies entering the sector with innovative strategies aimed at reshaping the mobility landscape. Rising concerns over environmental degradation and traffic congestion are fueling the shift from traditional car ownership to shared vehicle models. Urban populations are becoming more aware of sustainable transportation alternatives that not only reduce the number of vehicles on the road but also contribute to lowering carbon emissions and easing traffic flow. Municipal governments are encouraging these changes by implementing green transportation policies and emission-reduction targets, pushing shared mobility operators to adopt electric vehicles in their fleets. This transition aligns with broader smart city initiatives that aim to optimize urban infrastructure and reduce environmental impact.

The push for digitized and eco-conscious transportation has significantly influenced how telematics systems are designed and deployed. As car sharing becomes more mainstream, telematics software is emerging as the most crucial component, transforming vehicles into connected data hubs. In 2024, the software segment held more than 45% of the total market share, and it is expected to witness substantial growth during the forecast period. These platforms allow operators to track vehicle performance, monitor maintenance schedules, analyze user behavior, and improve overall fleet efficiency. The adoption of artificial intelligence in telematics software now enables systems to adjust fleet sizes dynamically based on real-time demand, reducing operational costs and boosting service quality. Features such as keyless vehicle entry, remote locking, billing automation, and user-friendly interfaces all stem from advanced software capabilities. At the same time, upgraded encryption protocols and cloud-based infrastructure ensure data protection and cybersecurity, making the platforms more robust and compliant with regulatory standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $311.3 Million |

| Forecast Value | $895.9 Million |

| CAGR | 11.3% |

When segmented by component, the market includes GPS receivers, accelerometers, engine interface modules, SIM cards, and software. These components work together to offer seamless connectivity and precise analytics. Software continues to lead in importance, offering real-time visibility and operational control for fleet managers. By integrating with cloud networks, software modules also enable advanced functions like user authentication, geo-fencing, and predictive diagnostics, which ensure safety and maximize fleet availability.

The market is also segmented by form into embedded, tethered, and integrated telematics. Embedded systems accounted for 49% of the market share in 2024 and are expected to dominate over the forecast timeline. These systems are installed by manufacturers directly into the vehicle and are integrated deeply into its electronics. The level of integration in embedded systems allows instant data transfer between the vehicle and backend systems, facilitating real-time performance insights and remote control capabilities. With increasing vehicle connectivity demands, embedded systems are becoming the industry standard for car sharing programs.

From a business model perspective, the subscription-based model stands out as the leading segment. Urban users gravitate toward this model because it offers consistent access to vehicle fleets at predictable monthly or annual rates. This approach supports long-term user engagement by providing transparent, budget-friendly pricing and eliminating the hassles of car ownership. Businesses operating under this model enjoy higher customer retention rates due to the dependable nature of the service.

Regionally, Asia Pacific led the market in 2024, with China holding around 65% of the regional market share and generating USD 74.2 million in revenue. China's leadership position is driven by its rapid urbanization, extensive car production capabilities, and technological advancements in connected vehicle infrastructure. National development policies aimed at promoting smart mobility and vehicle electrification have enabled widespread deployment of telematics systems across shared electric and hybrid vehicles. Additionally, investments in 5G networks, cloud computing, and Internet of Things (IoT) platforms support the expansion of sophisticated car sharing ecosystems. Battery management systems, AI-based vehicle tracking, and real-time fleet analytics are being integrated into shared mobility services, making the country a global leader in this sector.

The major players shaping the global car sharing telematics industry include providers of real-time tracking, behavior analysis, and predictive maintenance technologies. These systems now feature advanced sensor arrays, centralized control units, and 5G-enabled eSIMs that offer cross-border data exchange and cloud-based diagnostics. The market's evolution continues to be driven by a need for smarter, safer, and more efficient transportation solutions tailored to urban lifestyles and sustainability goals.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Car Sharing Telematics Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component providers

- 3.2.2 Automotive manufacturers

- 3.2.3 Technology provider

- 3.2.4 System integrators

- 3.2.5 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news and initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Integration of IOT and AI in transportation industry

- 3.9.1.2 Rising demand for sustainable transportation

- 3.9.1.3 Supportive regulations and government initiatives promoting shared mobility

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Concerns about data privacy

- 3.9.2.2 Significant upfront and ongoing costs

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Service, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Automatic Crash Notification (ACN)

- 5.3 Emergency

- 5.4 Navigation

- 5.5 Assistance & access

- 5.6 Diagnostics

- 5.7 Fleet management

- 5.8 Billing

- 5.9 Others

Chapter 6 Market Estimates & Forecast, By Form, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Embedded

- 6.3 Tethered

- 6.4 Integrated

Chapter 7 Market Estimates & Forecast, By Component, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 GPS receiver

- 7.3 Accelerometer

- 7.4 Engine interface

- 7.5 Sim card

- 7.6 Software

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Business Model, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Subscription-based model

- 8.3 Pay-per-use model

- 8.4 Corporate fleet management

- 8.5 Partnerships with OEMs

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 U.K.

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 CalAmp

- 10.2 cambio Mobilitatsservice

- 10.3 Cantamen

- 10.4 Carmine

- 10.5 Citiz Reseau

- 10.6 CityBee Solutions

- 10.7 Continental Aftermarket & Services

- 10.8 Fleetster (Next Generation Mobility)

- 10.9 Geotab

- 10.10 INVERS

- 10.11 Mobility Tech Green

- 10.12 Mojio

- 10.13 Octo Group

- 10.14 Ridecell

- 10.15 Samsara

- 10.16 Targa Telematics

- 10.17 Turo

- 10.18 Verizon Communications

- 10.19 Vulog

- 10.20 WeGo