|

|

市場調査レポート

商品コード

1741002

サーボモーターとドライブの市場機会と促進要因、産業動向分析、2025~2034年予測Servo Motors and Drives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| サーボモーターとドライブの市場機会と促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月29日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

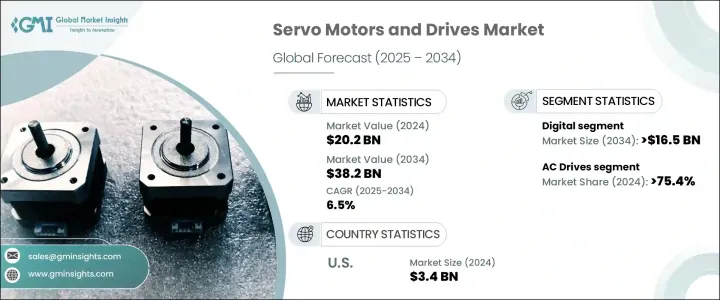

サーボモーターとドライブの世界市場規模は、2024年に202億米ドルとなり、CAGR 6.5%で成長し、2034年には382億米ドルに達すると予測されています。

産業界が運用コストを削減しながら生産性を向上させようと努力する中で、高い速度精度と位置精度を提供する高度なモーション・コントロール・システムの採用がますます重要になっています。特に産業オートメーションとスマート・マニュファクチャリングにおける研究開発投資の増加が、この成長の推進に大きな役割を果たしています。企業は、エネルギー消費を削減し、環境への影響を最小限に抑える技術を優先しており、この動向は、世界的に導入された厳しい効率化義務や排出規制によってさらに後押しされています。こうした変化は、長期的な市場拡大のための強固な基盤を作りつつあります。

需要が拡大するにつれて、従来の機器に代わる、よりスマートでコスト効率の高いものへのシフトが顕著になっています。サーボモーターとドライブのイノベーションは、変動する条件下で卓越した精度と一貫した性能を必要とする最新の製造・物流システムのニーズに応えています。さらに、産業界のデジタル化の進展とスマートファクトリー構想の普及により、さまざまな分野でサーボ技術の導入が加速しています。企業は、動的な作業負荷に適応でき、遠隔監視が可能で、他のインテリジェント・サブシステムとシームレスに統合できるシステムを求めています。このような開発により競合環境が形成され、メーカー各社は製品の効率、精度、柔軟性を向上させ、関連性を維持する必要に迫られています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 202億米ドル |

| 予測金額 | 382億米ドル |

| CAGR | 6.5% |

市場はカテゴリー別にデジタルタイプとアナログタイプに区分されます。デジタルサーボモーターとドライブは牽引役となっており、2034年までに165億米ドルを超えると予測されています。その人気の高まりは、機能性の向上、優れた保持力、高度なフィードバックと制御機能を提供できることに起因しています。これらのシステムは、リアルタイムのモニタリングと迅速な調整を必要とするアプリケーションに適しており、進化するオートメーション・ニーズに理想的に適合しています。デジタル・セグメントは、自動化された生産設備への投資が増加し、ダウンタイムとメンテナンス・コストの削減が重視されるようになっていることから利益を得ています。

ドライブの観点からは、市場はACドライブとDCドライブに分けられます。ACドライブは、2024年には市場全体の75.4%以上を占める大きなシェアを占め、2034年まで安定した成長が予測されます。ACサーボドライブの需要は、産業界における自動化の普及とインダストリー4.0技術の採用拡大により急増しています。これらのドライブは、優れたエネルギー効率、高度な産業用プロトコルとの互換性、さまざまな動作条件での柔軟性により支持されています。リアルタイムのデータ分析や予知保全機能など、継続的な技術向上がACドライブ・ソリューションの拡大をさらに後押ししています。

米国では、サーボモーターとドライブ市場が前年比で一貫した成長を示しています。2022年の評価額は30億米ドルだったが、2023年には32億米ドルに上昇し、2024年には34億米ドルに達しました。同国の成長軌道は、産業用IoT、スマート製造技術の採用拡大、完全自動化生産ラインの台頭によって支えられています。研究開発に重点を置く連邦政府および民間のイニシアティブは、産業環境におけるAI統合の支援と並んで、この分野の開発のための肥沃な土壌を作り出しています。

市場の集中度は依然として緩やかで、上位5社の合計シェアは約25%です。これらの大手企業は、製品のイノベーションに投資しているだけでなく、産業オートメーション・エコシステム一式を包含するように範囲を広げています。戦略的パートナーシップを形成し、補完的技術との互換性を強化することで、従来のドライブ・システムを超えた包括的ソリューションを提供する体制を整えています。主な発展には、サーボシステムへの人工知能、機械学習アルゴリズム、IoT対応機能の統合があり、自己制御とリアルタイム最適化が可能なスマートな適応型システムの開発に役立っています。

技術の進歩が製造業の情勢を絶えず変化させる中、業界各社は、リアルタイムの応答性、より高い効率レベル、より広範な接続性をサポートするサーボモーターとドライブの開発にリソースを注いでいます。これらの進歩は、インテリジェント・オートメーションへの大きなシフトを反映し、多様な産業アプリケーションにわたって柔軟性、長寿命、拡張性を提供するシステムに対するニーズの高まりを支えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 規制情勢

- 貿易への影響

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 市場規模・予測:カテゴリー別、2021-2034

- 主要動向

- デジタル

- アナログ

第5章 市場規模・予測:車で、2021-2034

- 主要動向

- ACドライブ

- DCドライブ

第6章 市場規模・予測:用途別、2021-2034

- 主要動向

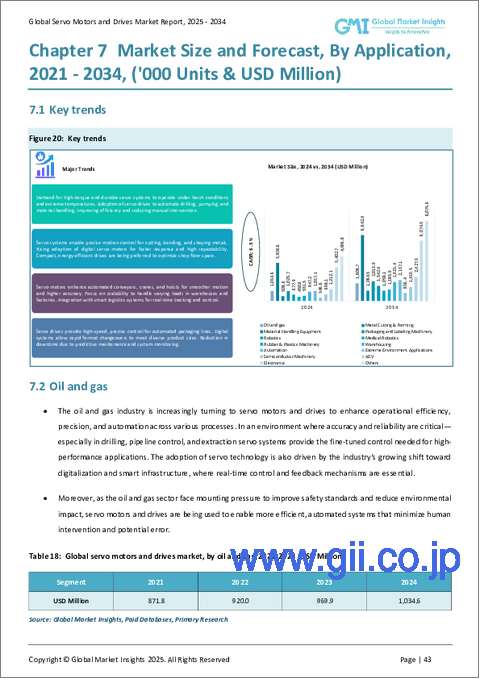

- 石油・ガス

- 金属切断および成形

- マテリアルハンドリング機器

- 包装およびラベリング機械

- ロボット工学

- 医療ロボット

- ゴム・プラスチック機械

- 倉庫

- オートメーション

- 極限環境アプリケーション

- 半導体製造装置

- 無人搬送車

- エレクトロニクス

- その他

第7章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ノルウェー

- スウェーデン

- デンマーク

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- タイ

- マレーシア

- フィリピン

- インドネシア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- ナイジェリア

- エジプト

- アルジェリア

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

第8章 企業プロファイル

- ABB

- Advanced Motion Controls

- Allied Motion

- Baumueller

- Bosch Rexroth

- Danfoss

- Delta Electronics

- Fuji Electric

- Hitachi

- Ingenia Cat

- KEB Automation

- Kollmorgen

- Mitsubishi Electric

- Nidec

- Panasonic

- Rockwell Automation

- Schneider Electric

- Siemens

- Yaskawa Electric

The Global Servo Motors and Drives Market was valued at USD 20.2 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 38.2 billion by 2034, fueled by the rising integration of automation, robotics, and energy-efficient technologies in industrial settings. The adoption of advanced motion control systems that offer high precision in speed and positional accuracy is becoming more critical as industries strive to enhance productivity while cutting operational costs. Increasing investment in research and development, especially in industrial automation and smart manufacturing, is playing a major role in driving this growth. Businesses are prioritizing technologies that reduce energy consumption and minimize environmental impact, a trend further supported by stringent efficiency mandates and emission control regulations introduced globally. These changes are creating a strong foundation for long-term market expansion.

As demand grows, there is a noticeable shift toward smarter, cost-effective alternatives to traditional equipment. Innovations in servo motors and drives are meeting the needs of modern manufacturing and logistics systems that require exceptional accuracy and consistent performance under variable conditions. Additionally, rising industrial digitization and the proliferation of smart factory initiatives are accelerating the deployment of servo technologies across multiple sectors. Companies are looking for systems that can adapt to dynamic workloads, offer remote monitoring, and integrate seamlessly with other intelligent subsystems. These developments are shaping a competitive environment where manufacturers are compelled to improve product efficiency, precision, and flexibility to stay relevant.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $20.2 Billion |

| Forecast Value | $38.2 Billion |

| CAGR | 6.5% |

The market is segmented based on category into digital and analog types. Digital servo motors and drives are gaining traction and are anticipated to surpass USD 16.5 billion by 2034. Their increasing popularity is attributed to enhanced functionality, better holding power, and the ability to provide advanced feedback and control features. These systems are well-suited for applications that demand real-time monitoring and rapid adjustments, making them an ideal fit for evolving automation needs. The digital segment benefits from increased investment in automated production facilities and a growing emphasis on reducing downtime and maintenance costs.

From the drive perspective, the market is divided into AC and DC drives. AC drives are expected to dominate with a significant share, accounting for over 75.4% of the total market in 2024, and are projected to grow steadily through 2034. The demand for AC servo drives has risen sharply, driven by widespread automation across industries and the growing adoption of Industry 4.0 technologies. These drives are favored due to their superior energy efficiency, compatibility with advanced industrial protocols, and flexibility in various operational conditions. Continued technological upgrades, including real-time data analytics and predictive maintenance capabilities, are further supporting the expansion of AC drive solutions.

In the United States, the servo motors and drives market has shown consistent year-on-year growth. Valued at USD 3 billion in 2022, it climbed to USD 3.2 billion in 2023 and reached USD 3.4 billion in 2024. The country's growth trajectory is underpinned by the increasing adoption of industrial IoT, smart manufacturing technologies, and the rising presence of fully automated production lines. Federal and private initiatives focused on R&D, alongside support for AI integration in industrial environments, are creating fertile ground for the sector's development.

Market concentration remains moderate, with the top five manufacturers holding a combined share of approximately 25%. These leading firms are not only investing in product innovation but are also broadening their scope to include complete industrial automation ecosystems. By forming strategic partnerships and enhancing compatibility with complementary technologies, they are positioning themselves to deliver comprehensive solutions that go beyond traditional drive systems. Key areas of focus include the integration of artificial intelligence, machine learning algorithms, and IoT-enabled features into servo systems, which helps develop smart, adaptive systems capable of self-regulation and real-time optimization.

With technological advancements continuously reshaping the manufacturing landscape, industry players are channeling resources into developing servo motors and drives that support real-time responsiveness, higher efficiency levels, and broader connectivity. These advancements reflect a larger shift toward intelligent automation and support the rising need for systems that offer flexibility, longevity, and scalability across diverse industrial applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.2 Retaliatory measures

- 3.2.3 Impact on the industry

- 3.2.3.1 Supply-side impact (raw materials)

- 3.2.3.1.1 Price volatility in key materials

- 3.2.3.1.2 Supply chain restructuring

- 3.2.3.1.3 Production cost implications

- 3.2.3.2 Demand-side impact (selling price)

- 3.2.3.2.1 Price transmission to end markets

- 3.2.3.2.2 Market share dynamics

- 3.2.3.2.3 Consumer response patterns

- 3.2.3.1 Supply-side impact (raw materials)

- 3.2.4 Key companies impacted

- 3.2.5 Strategic industry responses

- 3.2.5.1 Supply chain reconfiguration

- 3.2.5.2 Pricing and product strategies

- 3.2.5.3 Policy engagement

- 3.2.6 Outlook and future considerations

- 3.2.7 Regulatory landscape

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

Chapter 4 Market Size and Forecast, By Category, 2021 - 2034, ('000 Units & USD Million)

- 4.1 Key trends

- 4.2 Digital

- 4.3 Analog

Chapter 5 Market Size and Forecast, By Drive, 2021 - 2034, ('000 Units & USD Million)

- 5.1 Key trends

- 5.2 AC drive

- 5.3 DC drive

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034, ('000 Units & USD Million)

- 6.1 Key trends

- 6.2 Oil and gas

- 6.3 Metal cutting & forming

- 6.4 Material handling equipment

- 6.5 Packaging and labeling machinery

- 6.6 Robotics

- 6.7 Medical robotics

- 6.8 Rubber & plastics machinery

- 6.9 Warehousing

- 6.10 Automation

- 6.11 Extreme environment applications

- 6.12 Semiconductor machinery

- 6.13 AGV

- 6.14 Electronics

- 6.15 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034, ('000 Units & USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Norway

- 7.3.7 Sweden

- 7.3.8 Denmark

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Thailand

- 7.4.7 Malaysia

- 7.4.8 Philippines

- 7.4.9 Indonesia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 South Africa

- 7.5.5 Nigeria

- 7.5.6 Egypt

- 7.5.7 Algeria

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Advanced Motion Controls

- 8.3 Allied Motion

- 8.4 Baumueller

- 8.5 Bosch Rexroth

- 8.6 Danfoss

- 8.7 Delta Electronics

- 8.8 Fuji Electric

- 8.9 Hitachi

- 8.10 Ingenia Cat

- 8.11 KEB Automation

- 8.12 Kollmorgen

- 8.13 Mitsubishi Electric

- 8.14 Nidec

- 8.15 Panasonic

- 8.16 Rockwell Automation

- 8.17 Schneider Electric

- 8.18 Siemens

- 8.19 Yaskawa Electric