|

市場調査レポート

商品コード

1740992

ケーブルアセンブリ市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測Cable Assembly Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ケーブルアセンブリ市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月15日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

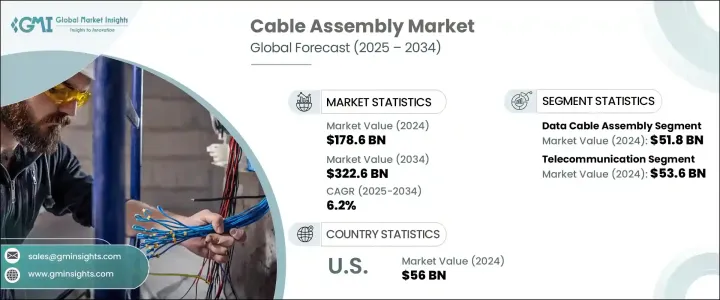

ケーブルアセンブリの世界市場規模は、2024年に1,786億米ドルとなり、家電需要の急増と5Gネットワークの急速な拡大に牽引され、CAGR 6.2%で成長し、2034年には3,226億米ドルに達すると推定されています。

ケーブルアセンブリは、高速通信、効率的なデータ伝送、シームレスな接続性のバックボーンとなっており、業界全体で重要なものとなっています。世界がデジタルトランスフォーメーション、スマートマニュファクチャリング、コネクテッドカー、IoT対応デバイスへとシフトする中、高度なケーブル技術への依存はますます強まっています。光ファイバー、ハイブリッドケーブル、高周波同軸ケーブルの人気が高まっているのは、大量のデータを処理し、超低遅延アプリケーションをサポートできる、より高速で信頼性の高いソリューションに対するニーズの高まりを反映しています。産業界は現在、インフラのアップグレードに多額の投資を行っており、次世代技術を可能にする革新的なケーブルアセンブリに対するかつてない需要を煽っています。AI、クラウドコンピューティング、スマートシティが世界的に拡大し続ける中、ケーブルアセンブリ市場は、接続された高速な未来を実現する上で極めて重要な役割を果たす態勢を整えています。

5G技術の拡大により、信頼性の高いデータ伝送、電力供給、大容量接続に不可欠な光ファイバー、同軸、ハイブリッドソリューションなどの高性能ケーブルの需要が急増しています。これらのケーブルアセンブリは、より高速な通信速度、低遅延、指数関数的に増大するデータ量の管理をサポートするために不可欠です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,786億米ドル |

| 予測金額 | 3,226億米ドル |

| CAGR | 6.2% |

米国が実施した通商政策と関税は、ケーブルアセンブリ業界を大きく混乱させ、特に中国からの部品や原材料の輸入に影響を与えました。この混乱は米国メーカーのコスト上昇を招き、代替調達戦略を模索したり、関税の影響に対抗するためにベトナムやメキシコといった国への事業移転を余儀なくされました。当初は一部の国内企業が恩恵を受けたが、市場全体がボラティリティの高まりに直面しているため、企業はサプライ・チェーンを多様化し、長期的な回復力を高めるために地域生産を検討する必要に迫られています。

データケーブルアセンブリ分野は、5Gインフラ、光ファイバーネットワーク、イーサネットシステムに不可欠な高速データケーブルの需要急増に後押しされ、2024年に518億米ドルを創出しました。クラウドコンピューティングの拡大とハイパースケールデータセンターの急速な普及により、広帯域幅ケーブルのニーズが引き続き高まっています。さらに、スマートフォン、ゲーム機、ウェアラブル技術、スマートホームデバイスの採用が拡大しており、市場の成長にさらに弾みがついています。

通信は、より高速なデータ伝送と低遅延通信の必要性に支えられ、2024年には536億米ドルと評価される主要な応用分野に浮上しました。5G展開のブーム、スマート監視のようなIoTアプリケーション、自動化システムの増加が、この分野における高度なケーブルソリューションの需要を促進しています。AIを搭載したクラウドベースのデータセンターの拡大が、この成長をさらに加速させています。

米国のケーブルアセンブリ市場は2024年に560億米ドルを生み出し、家電部門の活況、自動化動向、5Gインフラの拡大がその原動力となっています。スマート製造とデータセンター接続への依存の高まりが、最先端のケーブルアセンブリ需要をさらに加速させています。

世界のケーブルアセンブリ市場の主要企業には、TE Connectivity、Amphenol Corporation、Prysmian Spa、Nexans SA、RF Industries Ltd.、Smiths Group Plc、Samtec Inc.、Corning Inc.、Minnesota Wire &Cable Co.、Fischer Connectors Holding SA、BizLink Holding Inc.、W. L. Gore &Associates Inc.などがあります。これらのプレーヤーは、関税の不確実性に対処し、長期的な成長を確保するために、製品の革新、製造能力の拡大、次世代ソリューションのための研究開発への投資、電気通信やデータセンターのリーダーとの戦略的パートナーシップの形成、サプライチェーンの強化に注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 主要部品の価格変動

- サプライチェーン再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 家電製品の需要増加

- 5Gネットワークの拡大

- 再生可能エネルギー部門の成長

- データセンターインフラの拡大

- モノのインターネット(IoT)の導入増加

- 業界の潜在的リスク&課題

- 原材料費の上昇

- サプライチェーンの混乱による収益損失

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021 –2034

- 主要動向

- 電源ケーブルアセンブリ

- データケーブルアセンブリ

- 信号ケーブルアセンブリ

- リボンケーブルアセンブリ

- カスタムケーブルアセンブリ

- 同軸ケーブルアセンブリ

- その他

第6章 市場推計・予測:業種別、2021 –2034

- 主要動向

- 自動車

- 通信

- 家電

- 航空宇宙および防衛

- ヘルスケア

- エネルギー・公益事業

- その他

第7章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第8章 企業プロファイル

- Amphenol Corporation

- Aptiv

- BizLink Holding Inc

- Carrio Cabling Corp.

- Copartner Tech Corp.

- Corning Inc.

- Dongguan Luxshare Technology Co.、Ltd.

- Fischer Connectors Holding SA

- Minnesota Wire &Cable Co.

- Nexans SA

- Prysmian Spa

- RF Industries Ltd.

- Samtec Inc.

- Smiths Group Plc

- TE Connectivity

- W. L. Gore &Associates Inc.

The Global Cable Assembly Market was valued at USD 178.6 billion in 2024 and is estimated to grow at a CAGR of 6.2% to reach USD 322.6 billion by 2034, driven by the soaring demand for consumer electronics and the rapid expansion of 5G networks. Cable assemblies have become the backbone of high-speed communication, efficient data transmission, and seamless connectivity, making them critical across industries. As the world shifts towards digital transformation, smart manufacturing, connected vehicles, and IoT-enabled devices, the reliance on advanced cable technologies is intensifying. The growing popularity of fiber optics, hybrid cables, and high-frequency coaxial cables reflects the rising need for faster, more reliable solutions capable of handling large data volumes and supporting ultra-low latency applications. Industries are now investing heavily in upgrading infrastructure, fueling unprecedented demand for innovative cable assemblies that enable next-generation technologies. As AI, cloud computing, and smart cities continue to scale globally, the cable assembly market is poised to play a pivotal role in enabling a connected, high-speed future.

The expansion of 5G technology has triggered a sharp rise in demand for high-performance cables such as fiber optics, coaxial, and hybrid solutions, crucial for reliable data transmission, power delivery, and high-capacity connectivity. These cable assemblies are vital for supporting faster communication speeds, lower latency, and the management of exponentially growing data volumes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $178.6 Billion |

| Forecast Value | $322.6 Billion |

| CAGR | 6.2% |

Trade policies and tariffs implemented by the U.S. have significantly disrupted the cable assembly industry, particularly impacting the import of components and raw materials from China. This disruption has led to elevated costs for U.S. manufacturers, compelling them to explore alternative sourcing strategies and relocate operations to countries like Vietnam and Mexico to counter tariff effects. Although a few domestic players benefited initially, the broader market faces heightened volatility, prompting companies to diversify supply chains and consider regional production to enhance long-term resilience.

The data cable assembly segment generated USD 51.8 billion in 2024, propelled by skyrocketing demand for high-speed data cables essential for 5G infrastructure, fiber optic networks, and Ethernet systems. Cloud computing expansion and the rapid proliferation of hyperscale data centers continue to boost the need for high-bandwidth cables. Additionally, the growing adoption of smartphones, gaming consoles, wearable tech, and smart home devices adds further momentum to market growth.

Telecommunications emerged as a major application area, valued at USD 53.6 billion in 2024, supported by the need for faster data transmission and low-latency communication. The boom in 5G rollouts, IoT applications like smart surveillance, and the rising number of automated systems are driving demand for advanced cable solutions in this sector. Expansion of AI-powered and cloud-based data centers further amplifies this growth.

The U.S. Cable Assembly Market generated USD 56 billion in 2024, fueled by the booming consumer electronics sector, automation trends, and 5G infrastructure expansion. Increased reliance on smart manufacturing and data center connectivity further accelerates demand for cutting-edge cable assemblies.

Key companies in the Global Cable Assembly Market include TE Connectivity, Amphenol Corporation, Prysmian Spa, Nexans SA, RF Industries Ltd., Smiths Group Plc, Samtec Inc., Corning Inc., Minnesota Wire & Cable Co., Fischer Connectors Holding SA, BizLink Holding Inc., and W. L. Gore & Associates Inc. These players are focusing on product innovation, expanding manufacturing capabilities, investing in R&D for next-gen solutions, forming strategic partnerships with telecom and data center leaders, and strengthening supply chains to address tariff uncertainties and ensure long-term growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump Administration Tariffs

- 3.2.1 Impact on Trade

- 3.2.1.1 Trade Volume Disruptions

- 3.2.1.2 Retaliatory Measures

- 3.2.2 Impact on the Industry

- 3.2.2.1 Supply-Side Impact

- 3.2.2.1.1 Price Volatility in Key Components

- 3.2.2.1.2 Supply Chain Restructuring

- 3.2.2.1.3 Production Cost Implications

- 3.2.2.2 Demand-Side Impact (Selling Price)

- 3.2.2.2.1 Price Transmission to End Markets

- 3.2.2.2.2 Market Share Dynamics

- 3.2.2.2.3 Consumer Response Patterns

- 3.2.2.1 Supply-Side Impact

- 3.2.3 Key Companies Impacted

- 3.2.4 Strategic Industry Responses

- 3.2.4.1 Supply Chain Reconfiguration

- 3.2.4.2 Pricing and Product Strategies

- 3.2.4.3 Policy Engagement

- 3.2.5 Outlook and Future Considerations

- 3.2.1 Impact on Trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising demand for consumer electronics

- 3.3.1.2 Expansion of 5G networks

- 3.3.1.3 Growth in renewable energy sector

- 3.3.1.4 Increasing data center infrastructure

- 3.3.1.5 Rising internet of things (IoT) adoption

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Rising material costs

- 3.3.2.2 Supply chain disruptions leading to revenue loss

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Power cable assemblies

- 5.3 Data cable assemblies

- 5.4 Signal cable assemblies

- 5.5 Ribbon cable assemblies

- 5.6 Custom cable assemblies

- 5.7 Coaxial cable assemblies

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Industry Vertical, 2021 – 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Automotive

- 6.3 Telecommunications

- 6.4 Consumer electronics

- 6.5 Aerospace & defense

- 6.6 Healthcare

- 6.7 Energy & utilities

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Amphenol Corporation

- 8.2 Aptiv

- 8.3 BizLink Holding Inc

- 8.4 Carrio Cabling Corp.

- 8.5 Copartner Tech Corp.

- 8.6 Corning Inc.

- 8.7 Dongguan Luxshare Technology Co., Ltd.

- 8.8 Fischer Connectors Holding SA

- 8.9 Minnesota Wire & Cable Co.

- 8.10 Nexans SA

- 8.11 Prysmian Spa

- 8.12 RF Industries Ltd.

- 8.13 Samtec Inc.

- 8.14 Smiths Group Plc

- 8.15 TE Connectivity

- 8.16 W. L. Gore & Associates Inc.