ユーティリティ電気絶縁体の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Utility Electric Insulators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740986

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

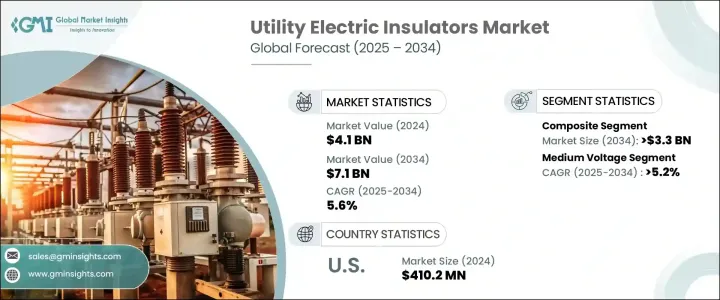

ユーティリティ電気絶縁体の世界市場規模は、2024年に41億米ドルとなり、急速な都市化や市場開拓に伴うエネルギー消費の増加に伴い、信頼性の高い電気インフラへのニーズが高まっていることから、CAGR 5.6%で成長し、2034年には71億米ドルに達すると予測されています。

各国が強靭な電力システムの構築に投資する中、高性能絶縁体の需要は急増すると予想されます。進化するエネルギー事情、特に再生可能エネルギー源へのシフトが加速する中、効率的で中断のない送電網の性能を確保する上で、電気絶縁体の役割がより重視されています。これらの部品は、送配電システムの信頼性と安全性の維持に不可欠です。

さらに、輸送の電化が進み、屋上ソーラーやエネルギー貯蔵のような分散型エネルギーシステムが台頭しているため、碍子はよりダイナミックで複雑なグリッド環境をサポートしなければならなくなっています。新興経済諸国ではインフラが老朽化し、よりスマートで適応性の高い電力ネットワークが求められているため、送電網の近代化に向けた投資が継続的に行われています。その結果、ユーティリティ電気絶縁体市場は、技術革新とインフラ配備の両方で上昇を経験しています。世界各国の政府は、クリーンエネルギーの生産を強化し、送電網の回復力を高め、ますます厳しくなる環境条件下でも動作可能な先進的な電気部品を採用するプログラムを積極的に支持しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 41億米ドル |

| 予測金額 | 71億米ドル |

| CAGR | 5.6% |

政府の政策や規制の枠組みは、ユーティリティ電気絶縁体市場の成長を支え続けています。これらのイニシアティブは、スマートグリッドインフラへの資金提供、再生可能エネルギー源の統合へのインセンティブ、老朽化した送電システムの交換や改修の義務付けなどをしばしば行っています。こうしたアップグレードの一環として、電力会社は優れた機械的強度、耐熱性、耐久性を提供する先進的な絶縁体に注目しています。例えば、ポスト碍子 Gen 2ファミリーのような新製品の発売は、信頼性の向上、極端な気象条件下での性能向上、設置の容易さを実現することで、こうした需要に応える一助となっています。これらの技術革新は、電力システムにおける自動化、デジタル化、持続可能性といったより広範な目標に沿いながら、レガシー・インフラストラクチャの問題に対処する上で極めて重要です。

材料に関しては、複合碍子分野は力強い成長軌道にあり、2034年までに33億米ドルを生み出すと予測されています。軽量設計、環境汚染物質に対する高い耐性、沿岸部、工業地帯、高湿度地域での優れた性能により、最新の電力システムに理想的な選択肢となっています。開発途上地域の都市化と工業化が進むにつれ、過酷な使用条件に耐える絶縁体へのニーズが急激に高まっています。複合がいしには持続可能性という利点もあるため、保守コストの削減と環境フットプリントの削減を目指す電力会社にとって、ますます魅力的なものとなっています。

電圧別では、中電圧分野が2034年までにCAGR 5.2%で成長すると予想されています。この成長は、電力会社の配電網で中電圧碍子が広く使用されていることと、再生可能エネルギー資産を送電網に接続する上で不可欠な役割を担っていることが主な要因です。各国が長距離送電のための大容量送電システムを導入するにつれて、電圧カテゴリーを問わず、信頼性が高く高性能の絶縁体に対する需要は増大し続けると思われます。各メーカーは、製品の熱的、機械的、電気的特性を向上させるため、研究開発に多額の投資を行っています。こうした進歩により、中・高圧碍子は現代の電力インフラにおいて重要な部品として位置づけられています。

米国のユーティリティ電気絶縁体市場は2024年に4億1,020万米ドルを生み出し、再生可能エネルギー容量の拡大、産業用電力ニーズの高まり、送電網の近代化を目指した取り組みがその原動力となっています。老朽化した電気システムのアップグレードと、エネルギー効率を高めリアルタイム監視を可能にするスマートグリッド技術の統合が、市場の上昇の勢いの中心となっています。都市部の老朽化した電柱の碍子(がいし)交換などのプロジェクトは、電力供給網の強化に対する国のコミットメントを例証しています。

世界のユーティリティ電気絶縁体市場の主要企業には、シーメンス・エナジー、CYGインシュレーター、GIPRO、LAPPインシュレーター、PHIインダストリアル、ABB、BHEL、Seves、日立エナジー、ゼネラル・エレクトリック、Elsewedy Electric、Newell Porcelain、PFISTERER、Izoelektro、Hubbell、Gamma Insulators、TE Connectivity、INAEL Electrical Systems、Insulation Technology Groupなどがあります。競争力を得るため、これらの企業は、次世代絶縁体技術への投資、製造拠点の拡大、世界な規模拡大のための戦略的提携など、いくつかの重要な戦略を推進しています。電力網のデジタル変革に伴い、メーカー各社は予知保全とシステムの信頼性を向上させるため、IoT対応のモニタリング・ソリューションも取り入れています。さらに、M&Aは、進化する電力会社の要件を満たすため、製品提供の幅を広げ、技術力を強化するための一般的な戦略であり続けています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:材料別、2021-2034

- 主要動向

- 陶磁器

- ガラス

- 複合

第6章 市場規模・予測:電圧別、2021-2034

- 主要動向

- 高

- 中

- 低

第7章 市場規模・予測:評価順、2021-2034

- 主要動向

- 11 kV未満

- 11 kV以上22 kV以下

- 22 kV以上33 kV以下

- 33 kV以上72.5 kV以下

- 72.5 kV以上145 kV以下

- 145 kV以上220 kV以下

- 220 kV以上400 kV以下

- 400 kV以上800 kV以下

- 800 kV以上1,200 kV以下

- 1,200 kV以上

第8章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第9章 企業プロファイル

- ABB

- BHEL

- CYG Insulator

- Elsewedy Electric

- Gamma Insulators

- General Electric

- GIPRO

- Hitachi Energy

- Hubbell

- INAEL Electrical Systems

- Insulation Technology Group

- Izoelektro

- LAPP Insulators

- Newell Porcelain

- PFISTERER

- PHI Industrial

- Seves

- Siemens Energy

- TE Connectivity

目次

The Global Utility Electric Insulators Market was valued at USD 4.1 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 7.1 billion by 2034, driven by the increasing need for dependable electrical infrastructure amid the rising energy consumption associated with rapid urbanization and industrial development. As nations invest in building resilient power systems, the demand for high-performance insulators is expected to surge. The evolving energy landscape, particularly the accelerating shift toward renewable energy sources, has placed greater emphasis on the role of electric insulators in ensuring efficient and uninterrupted grid performance. These components are essential in maintaining the reliability and safety of electricity transmission and distribution systems.

Moreover, with the ongoing electrification of transportation and the rise of distributed energy systems like rooftop solar and energy storage, insulators must now support more dynamic and complex grid environments. Aging infrastructure across developed economies, coupled with the need for smarter and more adaptable power networks, is fueling sustained investment in grid modernization initiatives. As a result, the utility electric insulators market is experiencing an upswing in both technological innovation and infrastructure deployment. Governments worldwide are actively endorsing programs to bolster clean energy production, enhance grid resilience, and adopt advanced electrical components capable of operating in increasingly demanding environmental conditions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.1 Billion |

| Forecast Value | $7.1 Billion |

| CAGR | 5.6% |

Government policies and regulatory frameworks continue to support the growth of the utility electric insulators market. These initiatives often provide funding for smart grid infrastructure, incentives for the integration of renewable energy sources, and mandates for the replacement or refurbishment of aging power transmission systems. As part of these upgrades, utilities are turning to advanced insulators that offer superior mechanical strength, thermal resistance, and durability. For example, new product launches such as the Gen 2 family of post insulators are helping meet these demands by delivering enhanced reliability, better performance in extreme weather conditions, and ease of installation. These innovations are critical in addressing legacy infrastructure issues while aligning with broader goals around automation, digitization, and sustainability in power systems.

In terms of materials, the composite insulators segment is on a strong growth trajectory and is projected to generate USD 3.3 billion by 2034. Their lightweight design, high resistance to environmental pollutants, and superior performance in coastal, industrial, and high-humidity areas make them an ideal choice for modern power systems. As developing regions continue to urbanize and industrialize, the need for insulators that can withstand harsh operating conditions is rising sharply. Composite insulators also offer added sustainability benefits, making them increasingly attractive for utilities seeking to lower maintenance costs and reduce the environmental footprint of their operations.

By voltage, the medium-voltage segment is expected to grow at a CAGR of 5.2% by 2034. This growth is largely driven by the widespread use of medium-voltage insulators in utility distribution networks and their essential role in connecting renewable energy assets to the grid. As countries implement high-capacity transmission systems for long-distance electricity delivery, the demand for reliable, high-performance insulators across voltage categories will continue to grow. Manufacturers are investing heavily in research and development to enhance the thermal, mechanical, and electrical properties of their products. These advancements are positioning medium and high-voltage insulators as critical components in modern power infrastructure.

In the United States, the utility electric insulators market generated USD 410.2 million in 2024, fueled by the expansion of renewable energy capacity, rising industrial electricity needs, and initiatives aimed at grid modernization. Upgrading outdated electrical systems and integrating smart grid technologies to enhance energy efficiency and enable real-time monitoring are central to the market's upward momentum. Projects such as the replacement of aging power pole insulators across urban areas exemplify the country's commitment to strengthening its power delivery networks.

Leading players in the global utility electric insulators market include Siemens Energy, CYG Insulator, GIPRO, LAPP Insulators, PHI Industrial, ABB, BHEL, Seves, Hitachi Energy, General Electric, Elsewedy Electric, Newell Porcelain, PFISTERER, Izoelektro, Hubbell, Gamma Insulators, TE Connectivity, INAEL Electrical Systems, and Insulation Technology Group. To gain a competitive edge, these companies are pursuing several key strategies, including investing in next-generation insulator technologies, expanding manufacturing footprints, and forming strategic alliances to scale globally. In line with the digital transformation of power grids, manufacturers are also incorporating IoT-enabled monitoring solutions to improve predictive maintenance and system reliability. Additionally, mergers and acquisitions remain a popular strategy for broadening product offerings and enhancing technical capabilities to meet evolving utility requirements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Material, 2021 - 2034, (USD Million)

- 5.1 Key trends

- 5.2 Ceramic/Porcelain

- 5.3 Glass

- 5.4 Composite

Chapter 6 Market Size and Forecast, By Voltage, 2021 - 2034, (USD Million)

- 6.1 Key trends

- 6.2 High

- 6.3 Medium

- 6.4 Low

Chapter 7 Market Size and Forecast, By Rating, 2021 - 2034, (USD Million)

- 7.1 Key trends

- 7.2 ≤ 11 kV

- 7.3 > 11 kV to ≤ 22 kV

- 7.4 > 22 kV to ≤ 33 kV

- 7.5 > 33 kV to ≤ 72.5 kV

- 7.6 > 72.5 kV to ≤ 145 kV

- 7.7 > 145 kV to ≤ 220 kV

- 7.8 > 220 kV to ≤ 400 kV

- 7.9 > 400 kV to ≤ 800 kV

- 7.10 > 800 kV to ≤ 1,200 kV

- 7.11 > 1,200 kV

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034, (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 BHEL

- 9.3 CYG Insulator

- 9.4 Elsewedy Electric

- 9.5 Gamma Insulators

- 9.6 General Electric

- 9.7 GIPRO

- 9.8 Hitachi Energy

- 9.9 Hubbell

- 9.10 INAEL Electrical Systems

- 9.11 Insulation Technology Group

- 9.12 Izoelektro

- 9.13 LAPP Insulators

- 9.14 Newell Porcelain

- 9.15 PFISTERER

- 9.16 PHI Industrial

- 9.17 Seves

- 9.18 Siemens Energy

- 9.19 TE Connectivity

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日