|

市場調査レポート

商品コード

1740983

酸化チタンリチウムの市場機会、成長促進要因、産業動向分析、2025~2034年予測Lithium Titanium Oxide Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 酸化チタンリチウムの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月16日

発行: Global Market Insights Inc.

ページ情報: 英文 263 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

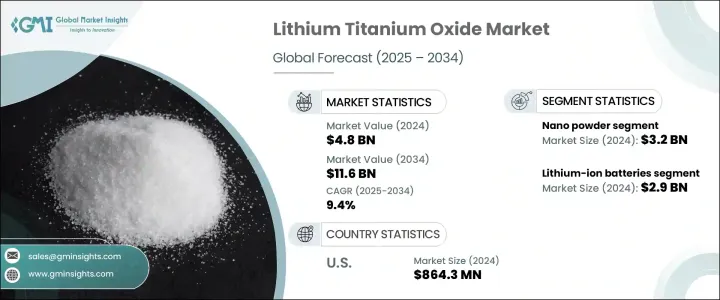

世界の酸化チタンリチウム市場は、2024年に48億米ドルと評価され、エネルギー貯蔵システム(ESS)と電気自動車(EV)の需要急増に後押しされ、CAGR 9.4%で成長し、2034年には116億米ドルに達すると推定されています。

世界の産業がクリーンエネルギーと効率的なストレージソリューションに軸足を移しているため、同市場は力強い勢いを見せています。LTO電池は、超高速充電機能、長サイクル寿命、優れた熱安定性が評価され、民生用電子機器、グリッドストレージ、自動車用途でその性能がますます支持されるようになっています。

再生可能エネルギーの導入が加速する中、安定的かつ効率的なグリッドストレージシステムの必要性はかつてないほど高まっており、LTOバッテリーは世界のエネルギーインフラを近代化する上で重要なコンポーネントとなっています。各国政府がより厳しいカーボンニュートラル目標を実施し、産業界が脱炭素化に注力する中、高性能で持続可能な電池技術への需要は、LTOメーカーに大きなビジネスチャンスをもたらしています。安全性、長寿命、短時間での充電が重視されるようになり、航空宇宙、防衛、大型輸送などの分野でLTOの魅力がさらに高まっています。市場プレーヤーは、LTOバッテリーの商業用途の拡大を活用するため、急速に生産規模を拡大し、研究に投資し、戦略的提携を結んでいます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 48億米ドル |

| 予測金額 | 116億米ドル |

| CAGR | 9.4% |

さらに、特に電気自動車の急速な生産拡大により、自動車分野がLTO市場を牽引する大きな役割を果たしています。LTOバッテリーは、急速充電機能、優れた熱安定性、ライフサイクルの延長により、電気自動車用途において信頼性の高い代替品として見なされており、厳しい条件下で安定した性能を要求される高性能電気自動車や商用電気自動車に非常に適しています。世界の自動車メーカーが脱炭素化と持続可能なイノベーションへの取り組みを強化する中、LTOバッテリーはフリート、バス、都市モビリティ・プラットフォームの実用的なソリューションとして台頭してきています。数千回の充放電サイクルに耐え、劣化を最小限に抑えるLTOバッテリーは、長期的な運用コストを削減することで、環境と経済の両方の目標に沿った大きな価値をもたらします。

LTO市場は、グレードとバッテリータイプによって区分されます。2024年はナノパウダーLTOが市場を席巻し、32億米ドルの貢献。ナノ粉末を使用することで、LTO電池の表面積対体積比が改善され、容量、サイクル安定性、充放電速度などの電気化学特性が向上します。導電性の向上と粒度分布の均一化により、ナノ粉末はエネルギー貯蔵システムや電気自動車にとって理想的な材料選択となります。

同市場は電池の種類によっても分類され、リチウムイオン電池が最大のシェアを占めています。2024年には、リチウムイオン電池分野が29億米ドルを占め、59.6%のシェアを占めています。LTO電池は安全性、寿命、急速充電に優れているが、従来のリチウムイオン電池に比べてエネルギー密度が低く、コストが高いため、普及には限界があります。しかし、その明確な利点により需要は増加し続けています。

米国酸化チタンリチウム市場は2024年に8億6,430万米ドルに達し、産業界の高性能エネルギー貯蔵に対する需要の高まりが後押ししています。LTOバッテリーは、その優れた信頼性、安全性、極端な温度下での動作能力により、自動車、航空宇宙、再生可能エネルギー分野に理想的なものとして、強い支持を集めています。

世界の酸化チタンリチウム業界の主要企業には、BTR New Material Group、NEI Corporation、Microvast Holdings、Ossila、SAT Nano Technology Materialなどがあります。これらの企業は、製造プロセスの革新、アプリケーション技術の強化、研究開発投資の拡大、戦略的パートナーシップの締結を継続的に行い、急成長するLTO市場での地位を強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国

- 主要輸入国

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 電気自動車とクリーンエネルギーソリューションの需要の高まり

- LTOバッテリーの優れた性能と長いサイクル寿命

- エネルギー貯蔵システムにおけるLTOの採用増加

- 業界の潜在的リスク&課題

- 従来のリチウムイオン電池に比べて生産コストが高め

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品別、2021 –2034

- 主要動向

- ナノパウダー

- ミクロンパウダー

第6章 市場推計・予測:用途別、2021 –2034

- 主要動向

- リチウムイオン電池

- チタン酸リチウム電池

- その他

第7章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第8章 企業プロファイル

- BTR New Material Group

- Microvast Holdings

- NEI Corporation

- Ossila

- SAT Nano Technology Material

- Stanford Advanced Materials

- Tokyo Chemical Industry India

- Xiamen AOT Electronics Technology

- Xiamen TOB New Energy Technology

- Xiamen Tmax Battery Equipments

The Global Lithium Titanium Oxide Market was valued at USD 4.8 billion in 2024 and is estimated to grow at a CAGR of 9.4% to reach USD 11.6 billion by 2034, fueled by surging demand from energy storage systems (ESS) and electric vehicles (EVs). The market is experiencing strong momentum as industries worldwide pivot toward clean energy and efficient storage solutions. LTO batteries, recognized for their ultra-fast charging capabilities, long cycle life, and superior thermal stability, are becoming increasingly favored for their performance in consumer electronics, grid storage, and automotive applications.

As renewable energy adoption accelerates, the need for stable and efficient grid storage systems has never been greater, positioning LTO batteries as a critical component in modernizing global energy infrastructure. With governments implementing stricter carbon neutrality goals and industries focusing on decarbonization, the demand for high-performance, sustainable battery technologies is creating massive opportunities for LTO manufacturers. The growing emphasis on safety, longevity, and quick turnaround charging further boosts the appeal of LTO across sectors like aerospace, defense, and heavy-duty transportation. Market players are rapidly scaling production, investing in research, and forging strategic alliances to leverage the expanding commercial applications of LTO batteries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.8 Billion |

| Forecast Value | $11.6 Billion |

| CAGR | 9.4% |

Moreover, the automotive sector is playing a major role in driving the LTO market forward, especially with the rapid expansion of electric vehicle production. LTO batteries are increasingly seen as a reliable alternative in EV applications due to their fast-charging capabilities, excellent thermal stability, and extended life cycles, making them highly suitable for high-performance and commercial electric vehicles that demand consistent performance under rigorous conditions. As global automakers intensify their focus on decarbonization and sustainable innovation, LTO batteries are emerging as a practical solution for fleets, buses, and urban mobility platforms. Their ability to endure thousands of charge-discharge cycles with minimal degradation adds significant value by reducing long-term operational costs, aligning with both environmental and economic goals.

The LTO market is segmented based on grade and battery type. Nano powder LTO dominated the market in 2024, contributing USD 3.2 billion. The use of nanopowders improves the surface area-to-volume ratio of LTO batteries, enhancing their electrochemical properties such as capacity, cycle stability, and charge/discharge rates. Improved conductivity and uniform particle size distribution make nanopowders an ideal material choice for energy storage systems and electric vehicles.

The market is also categorized by battery type, with lithium-ion batteries holding the largest share. In 2024, the lithium-ion battery segment accounted for USD 2.9 billion, representing a 59.6% share. While LTO batteries excel in safety, longevity, and fast charging, their lower energy density and higher cost compared to conventional lithium-ion batteries limit widespread adoption. However, their demand continues to rise due to their distinct advantages.

The U.S. Lithium Titanium Oxide Market reached USD 864.3 million in 2024, propelled by rising demand for high-performance energy storage across industries. LTO batteries are gaining strong traction due to their outstanding reliability, safety, and ability to operate under extreme temperatures, making them ideal for the automotive, aerospace, and renewable energy sectors.

Key players in the Global Lithium Titanium Oxide Industry include BTR New Material Group, NEI Corporation, Microvast Holdings, Ossila, and SAT Nano Technology Material. These companies are continuously innovating manufacturing processes, enhancing application technologies, expanding R&D investments, and forging strategic partnerships to strengthen their position in the rapidly growing LTO market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Base estimates and calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic Industry Responses

- 3.2.4.1 Supply Chain Reconfiguration

- 3.2.4.2 Pricing and Product Strategies

- 3.2.4.3 Policy Engagement

- 3.2.5 Outlook and Future Considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major Exporting Countries

- 3.3.2 Major Importing Countries

- 3.4 Profit margin analysis

- 3.5 Key news and initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising demand for electric vehicles and clean energy solutions

- 3.7.1.2 Superior performance and long cycle life of LTO batteries

- 3.7.1.3 Increasing adoption of LTO in energy storage systems

- 3.7.2 Industry pitfalls and challenges

- 3.7.2.1 High production costs compared to conventional lithium-ion batteries

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Nano powder

- 5.3 Micron powder

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Lithium-ion batteries

- 6.3 Lithium-titanate battery

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 BTR New Material Group

- 8.2 Microvast Holdings

- 8.3 NEI Corporation

- 8.4 Ossila

- 8.5 SAT Nano Technology Material

- 8.6 Stanford Advanced Materials

- 8.7 Tokyo Chemical Industry India

- 8.8 Xiamen AOT Electronics Technology

- 8.9 Xiamen TOB New Energy Technology

- 8.10 Xiamen Tmax Battery Equipments