自動車用ドアシルの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Automotive Door Sills Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740958

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

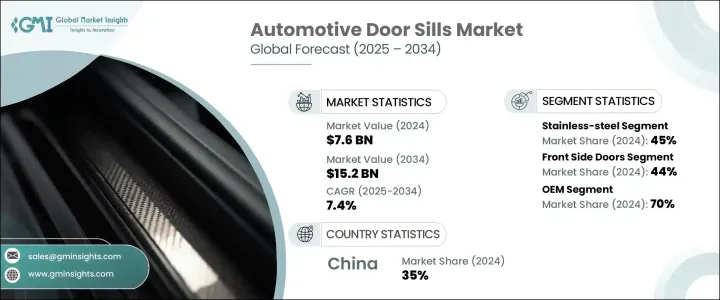

自動車用ドアシルの世界市場規模は、2024年に76億米ドルとなり、CAGR 7.4%で成長し、2034年には152億米ドルに達すると予測されています。

この拡大を後押ししている主な要因は、車両エントリーシステムへの注目の高まりと、世界の自動車生産台数の一貫した増加です。自動車がよりスマートな技術とより洗練された美観で進化するにつれて、ドアシルはもはや単なる保護トリムとしてではなく、デザインと機能性の両方を高める多機能部品と見なされるようになっています。自動車メーカーは、ユーザーエクスペリエンス、耐久性、ビジュアルアピールを向上させるために、照明システム、近接検知、高強度材料などの先進機能を統合しています。軽量設計は電気自動車やハイブリッド車において特に重要であり、余分な重量を増やすことなく強度を提供する材料への需要を促進しています。カーボンファイバー、アルミニウム、耐衝撃性ポリマーは、性能とスタイリングの両方の基準を満たす最新のシルの作成に不可欠となっています。これらの素材は、複雑なデザイン、構造性能の向上、環境条件への耐性の向上を可能にし、これらすべてがエネルギー効率と長期使用という広範な目標をサポートします。

自動車用ドアシルはまた、インタラクティブな要素をミックスにもたらすセンサーベースの技術革新によっても変化しています。メーカー各社は、人の接近に反応し、周囲の照明と連動し、さらにはタッチやジェスチャー操作を可能にするスマートシルを模索しています。こうした機能により、ドアシルは現代自動車のインテリジェント・アーキテクチャの一部として位置づけられ、自動車の幅広いインフォテインメント・システムやエントリー・システムとシームレスに統合されます。テクノロジーが自動車のインテリアと融合し続ける中、こうした強化されたドアシルは、高品質でカスタマイズされたドライビング体験を提供するために不可欠なものとなりつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 76億米ドル |

| 予測金額 | 152億米ドル |

| CAGR | 7.4% |

2024年には、ステンレス鋼が市場の約45%を占め最大のシェアを占め、2034年までのCAGRは7%を超えると予測されます。この優位性は、ステンレス鋼の比類なき耐久性、コスト効率、耐衝撃性によるものです。ステンレス鋼は、特にSUVやフリートカーのような交通量の多い車両で、繰り返される乗り降りにも耐えられます。また、その耐腐食性により、過酷な天候や路面状況下でも、外観や構造的に無傷であることが保証されます。電気自動車やハイブリッド車の場合、ステンレス鋼は、車体の完全性を維持するのに必要な構造強度を提供すると同時に、イルミネーションロゴ、ダイナミック照明、スマートアクセスモジュールなどの最新機能にも対応します。

用途別では、フロント・サイドドア部門が2024年に44%のシェアを占めて市場を牽引し、2025~2034年のCAGRは7%を超えると予想されます。フロントドアのドアシルは、ドライバーと同乗者の両方から最も高いインタラクションを受け、保護と装飾のアップグレードの主な焦点となっています。自動車メーカー各社は、この部分を活用してブランディング要素やユーザー中心の機能を導入しています。第一印象を持続させ、車両全体のデザイン性を強調するために、照明付きシルやロゴ入りトリムがここに組み込まれることが多いです。

車両タイプ別に分類すると、セダン、ハッチバック、コンパクトSUVの世界の生産台数の多さから、乗用車セグメントが引き続き優位を占めています。バイヤーが視覚的に魅力的で機能的なインテリアのアップグレードに傾倒しているため、メーカーはこれらの車両に、保護と高級感を兼ね備えたステンレス鋼や照明付きシルプレートを装備しています。電気自動車や自律走行モデルへのシフトが進む中、ドアシルコンポーネントも統合電子システムに対応するよう進化しており、単なる外観上の役割にとどまらない重要性を増しています。

アジア太平洋地域では、中国が2024年に市場の支配者に浮上し、約7億米ドルを生み出し、地域シェアの約35%を占めています。世界最大の自動車生産国としての地位と、電気自動車に対する国内需要の高まりが、このリーダーシップに大きく貢献しています。同国の強固な製造エコシステムは、先進ドアシルシステムの効率的な生産と輸出を可能にしています。

この市場は、ユーザー重視の人間工学、高性能素材、アンビエント・インテグレーションといった自動車業界の動向によって形成されつつあります。機械的ストレス、天候への暴露、電子部品の安定性といった課題に対処するため、メーカーは現在、高い耐衝撃性を持つ熱可塑性プラスチック、紫外線に安定した仕上げ、防水LEDシステムを採用しています。これらのアップグレードは、特にプレミアム車セグメントにおいて、極端な気候や常時使用下でのシルの耐久性を向上させます。

高度な製造技術により、特にライトやセンサーを内蔵したモデルの装着精度が向上しています。クイックアセンブリー接着剤とクリップロックシステムの使用により、振動によるダメージを最小限に抑え、よりクリーンな取り付けを実現しています。一方、EMIシールド配線と最適化されたケーブル配線は、照明付きシルの信号干渉を回避するのに役立ちます。AIと3Dビジュアライゼーションによるインテリジェント設計プラットフォームは、現在、シルモジュールの迅速なプロトタイピングとカスタマイズを可能にしています。これらのツールは、ブランディングの目標、ユーザーインターフェースの期待、車両の美観に正確に合わせることを可能にし、ドアシルを次世代車両のキャビンの重要なインタラクションポイントにします。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 製造業者

- 原材料サプライヤー

- 自動車OEM

- 流通チャネル

- 最終用途

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(顧客へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 価格動向分析

- 製品

- 地域

- コスト内訳分析

- 影響要因

- 促進要因

- 車両のカスタマイズに対する需要の高まり

- 内部保護に対する意識の高まり

- 電気自動車と高級車の販売増加

- 世界の自動車生産の増加

- 業界の潜在的リスク&課題

- 高度な設計による高製造コスト

- 過酷な環境での耐久性の懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:材料別、2021-2034

- 主要動向

- ステンレス鋼

- アルミニウム

- ゴム

- プラスチック

- 炭素繊維

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- フロントサイドドア

- 後部ドア

- テールゲート

第7章 市場推計・予測:車両別、2021-2034

- 主要動向

- 乗用車

- 商用車

- 小型商用車

- 中型商用車

- 大型商用車

第8章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- AC Schnitzer

- BMW

- Bosch

- Galio

- Gestamp

- Gronbach

- Hangzhou Green Offroad Auto Parts

- Honda Access

- Innotec

- Key Safety Systems(KSS)

- Mahle

- Mopar(FCA)

- Normic Industries

- Prius Auto Industries

- Rugged Ridge

- Shenzhen ATR Industry

- Shenzhen Yanming Plate Process

- SKS Kontakttechnik

- STEProtect(Sliplo)

- Zealio Electronics

目次

The Global Automotive Door Sills Market was valued at USD 7.6 billion in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 15.2 billion by 2034. A key factor fueling this expansion is the heightened focus on vehicle entry systems and the consistent rise in global automobile production. As vehicles evolve with smarter technologies and more refined aesthetics, door sills are no longer viewed as simple protective trims but as multifunctional components that enhance both design and functionality. Automakers are integrating advanced features like lighting systems, proximity detection, and high-strength materials to improve user experience, durability, and visual appeal. Lightweight designs are especially important in electric and hybrid vehicles, driving the demand for materials that provide strength without adding extra weight. Carbon fiber, aluminum, and impact-resistant polymers are becoming essential in creating modern sills that meet both performance and styling standards. These materials allow for intricate designs, improved structural performance, and better resistance to environmental conditions, all of which support the broader goals of energy efficiency and long-term use.

Automotive door sills are also being transformed through sensor-based innovations that bring interactive elements into the mix. Manufacturers are exploring smart sills that can respond to human proximity, coordinate with ambient lighting, and even enable touch or gesture controls. These features position the door sill as part of the intelligent architecture of modern vehicles, seamlessly integrating with the car's broader infotainment and entry systems. As technology continues to merge with automotive interiors, these enhanced sills are becoming crucial for delivering a high-quality, customized driving experience.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.6 billion |

| Forecast Value | $15.2 Billion |

| CAGR | 7.4% |

In 2024, stainless steel held the largest share of the market, accounting for approximately 45%, and is projected to grow at a CAGR exceeding 7% through 2034. This dominance is due to stainless steel's unmatched durability, cost-effectiveness, and impact resistance. It holds up well under repeated entry and exit, especially in high-traffic vehicles like SUVs and fleet cars. Its corrosion resistance also ensures that it remains visually and structurally intact even under harsh weather or road conditions. For electric and hybrid models, stainless steel offers the structural strength needed to support vehicle body integrity while accommodating modern features like illuminated logos, dynamic lighting, or smart access modules.

From an application perspective, the front side doors segment led the market with a 44% share in 2024 and is expected to expand at a CAGR of over 7% between 2025 and 2034. Front door sills see the highest interaction from both drivers and passengers, making them the primary focus for protective and decorative upgrades. Auto manufacturers leverage this section to introduce branding elements and user-centric features, as it forms a major visual and tactile contact point when entering the vehicle. Illuminated sills and logo-enhanced trims are frequently integrated here to leave a lasting first impression and emphasize the vehicle's overall design quality.

When classified by vehicle type, the passenger cars segment continues to dominate due to the high global production volumes of sedans, hatchbacks, and compact SUVs. As buyers lean toward visually appealing and functional interior upgrades, manufacturers are equipping these vehicles with stainless steel and lighted sill plates that combine protection with a touch of luxury. With the increasing shift toward electric and autonomous models, door sill components are also evolving to be compatible with integrated electronic systems, reinforcing their importance beyond just cosmetic roles.

In the Asia-Pacific region, China emerged as the dominant market player in 2024, generating approximately USD 700 million and holding around 35% of the regional share. Its position as the world's largest vehicle producer and growing domestic appetite for electric vehicles contribute significantly to this leadership. The country's robust manufacturing ecosystem enables efficient production and export of advanced door sill systems.

The market is being shaped by automotive industry trends such as user-focused ergonomics, high-performance materials, and ambient integration. To address challenges like mechanical stress, weather exposure, and electronic component stability, manufacturers now employ thermoplastics with high impact resistance, UV-stable finishes, and waterproof LED systems. These upgrades enhance the sills' durability in extreme climates and under constant use, especially in premium vehicle segments.

Advanced manufacturing techniques are improving fitment accuracy, particularly for models featuring integrated lights and sensors. The use of quick-assembly adhesives and clip-lock systems minimizes vibration damage and ensures cleaner installations. Meanwhile, EMI-shielded wiring and optimized cable routing helps avoid signal interference in illuminated sills. Intelligent design platforms powered by AI and 3D visualization are now enabling rapid prototyping and customization of sill modules. These tools allow for precise alignment with branding goals, user interface expectations, and vehicle aesthetics, making door sills a key point of interaction in next-generation vehicle cabins.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturers

- 3.2.2 Raw material suppliers

- 3.2.3 Automotive OEM

- 3.2.4 Distribution channel

- 3.2.5 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Pricing trend analysis

- 3.9.1 Product

- 3.9.2 Region

- 3.10 Cost breakdown analysis

- 3.11 Impact on forces

- 3.11.1 Growth drivers

- 3.11.1.1 Rising demand for vehicle customization

- 3.11.1.2 Growing awareness of interior protection

- 3.11.1.3 Growth in electric and luxury vehicle sales

- 3.11.1.4 Increasing automotive production globally

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High manufacturing costs of advanced designs

- 3.11.2.2 Durability concerns in harsh environments

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Stainless steel

- 5.3 Aluminum

- 5.4 Rubber

- 5.5 Plastic

- 5.6 Carbon fiber

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Front side doors

- 6.3 Back side door

- 6.4 Tailgate

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles

- 7.3.2 Medium commercial vehicles

- 7.3.3 Heavy commercial vehicles

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 AC Schnitzer

- 10.2 BMW

- 10.3 Bosch

- 10.4 Galio

- 10.5 Gestamp

- 10.6 Gronbach

- 10.7 Hangzhou Green Offroad Auto Parts

- 10.8 Honda Access

- 10.9 Innotec

- 10.10 Key Safety Systems (KSS)

- 10.11 Mahle

- 10.12 Mopar (FCA)

- 10.13 Normic Industries

- 10.14 Prius Auto Industries

- 10.15 Rugged Ridge

- 10.16 Shenzhen ATR Industry

- 10.17 Shenzhen Yanming Plate Process

- 10.18 SKS Kontakttechnik

- 10.19 STEProtect (Sliplo)

- 10.20 Zealio Electronics

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日