セルフストレージソフトウェア市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Self-Storage Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740955

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

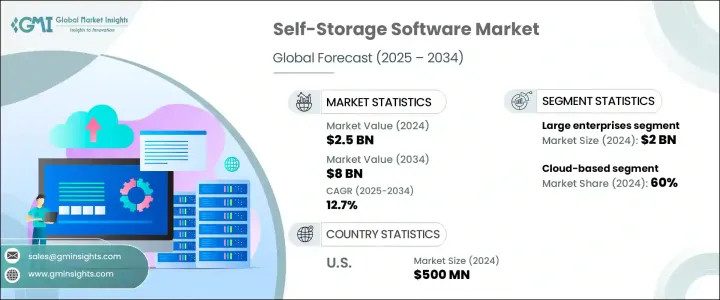

世界のセルフストレージソフトウェア市場は、2024年に25億米ドルと評価され、不動産セクター全体のデジタルソリューションに対する需要の急増、急速な都市部への移住、住宅および商業環境の両方における効率的なスペース管理に対するニーズの高まりによって、CAGR 12.7%で成長し、2034年には80億米ドルに達すると推定されています。

不動産のダイナミクスが進化を続ける中、セルフストレージ事業者は、業務の合理化、テナント体験の向上、施設のセキュリティ強化のために、デジタル・プラットフォームへの関心を高めています。利便性、自動化、データ主導の意思決定が重視されるようになり、最先端のソフトウェアシステムの導入が進んでいます。オペレーターは、従来のインフラに制約されることなく、リアルタイムのモニタリングを可能にし、稼働管理を改善し、業務効率を高める、拡張性のあるクラウドベースのツールを求めています。

ハイテク化が進む今日、セルフストレージソフトウェアは施設運営の近代化において重要な役割を果たしています。非接触型レンタル、自動課金、オンライン決済、リアルタイムの稼働状況追跡などの機能を備えたこれらのソリューションは、オペレーターが競争市場で優位に立つことを支援します。顧客関係管理(CRM)ツール、デジタル入退室管理システム、高度な分析を統合することで、企業はさらに可視性を高め、全体的なユーザー体験を向上させることができます。デジタル・セキュリティの重要性が増すにつれ、プラットフォームには暗号化、モバイル・アラート、詳細なアクセス・ログが組み込まれ、透明性を高め、テナントの信頼を築くことができるようになりました。予測分析、安全な契約管理のためのブロックチェーン、没入型バーチャルツアーのための拡張現実(AR)などの新技術の統合は、企業がデータと顧客の両方に接する方法を再構築し、最終的に敏捷性と収益性の向上を促進します。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 25億米ドル |

| 予測金額 | 80億米ドル |

| CAGR | 12.7% |

クラウドベースのセルフストレージソフトウェアが市場を独占し、2024年の世界収益の60%近くを占める。このセグメントの人気は、その柔軟性、手頃な価格、複数の拠点にまたがる業務をシームレスにサポートする能力に起因しています。クラウドプラットフォームは拡張や管理が容易なため、拠点を拡大するセルフストレージ事業者にとって理想的なものとなっています。これらのシステムでは、人工知能(AI)主導のツール、予測保守スケジュール、動的な価格設定モデルなど、オンプレミスのインフラでは導入が困難な機能の実装が可能です。企業は、一元化されたアクセス、リアルタイムの更新、最小限のITオーバーヘッドから恩恵を受け、パフォーマンスと意思決定能力を大幅に向上させることができます。

サブスクリプション・ベースのモデルは、セルフストレージソフトウェア業界全体で好まれる価格体系として台頭してきました。これらのモデルは、特に先行投資による経済的負担を避けたい中小規模の事業者にとって、比類のない手頃な価格と統合の柔軟性を提供します。定期的な支払い構造を通じて、事業者は最新のソフトウェア機能、リアルタイムのアップデート、技術サポート、堅牢なサイバーセキュリティ強化への継続的なアクセスを得ることができます。このセットアップにより、運用の一貫性が確保されるとともに、事業者は変化する業界標準に準拠し続けることができます。また、サブスクリプション・モデルにより、プロバイダーはより頻繁な製品改良を提供することができ、変化の速いデジタル・エコシステムにおいてビジネスを俊敏に保つことができます。

米国のセルフストレージソフトウェア市場は2024年に5億米ドルに達し、約12.9%のCAGRで成長すると予測されています。セルフストレージ部門が確立され、デジタル利便性に対する消費者の期待が高まっている米国では、クラウドベースの管理プラットフォームへのシフトが顕著になっています。主要ソフトウェア・プロバイダによる戦略的投資と、デジタル・インフラをアップグレードしデータ・セキュリティを強化する政府の取り組みが、ソフトウェア採用をさらに加速させています。全米の企業は、スペース利用の最適化、サービス提供の改善、規制遵守の確保において、スケーラブルなAI対応ソリューションの価値を認識しています。

世界のセルフストレージソフトウェア市場における主要企業には、OpenTech Alliance、storEDGE、QuikStor、Yardi Systems、Cascade Self-Storage、Space Managementなどがあります。これらの企業は、ユーザーエクスペリエンスを向上させ、バックエンドプロセスを合理化する先進的なクラウドネイティブソリューションでポートフォリオを拡大することに注力しています。AI、IoT、ブロックチェーン技術を活用することで、よりスマートで安全、かつ効率性の高いプラットフォームを提供しています。また、多くの企業が戦略的パートナーシップ、買収、共同事業を展開し、市場での存在感を高め、リーチを広げ、セルフストレージソフトウェア領域でのイノベーションを推進しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料供給者

- 部品供給業者

- 製造業者

- テクノロジープロバイダー

- 流通チャネル分析

- 最終用途

- 利益率分析

- サプライヤーの情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 特許分析

- 規制情勢

- コスト内訳分析

- 主なニュースと取り組み

- 影響要因

- 促進要因

- 施設管理のデジタル変革

- 都市化の進行と空間の制約

- 非接触型およびリモートアクセスの需要

- スマートテクノロジーとの統合

- 業界の潜在的リスク&課題

- 初期導入コストが高め

- データプライバシーとサイバーセキュリティのリスク

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:展開別、2021-2034

- 主要動向

- クラウドベース

- オンプレミス

第6章 市場推計・予測:組織規模別、2021-2034

- 主要動向

- 大企業

- 中規模企業(SME)

- 中小企業

第7章 市場推計・予測:ビジネスモデル別、2021-2034

- 主要動向

- サブスクリプションベース

- 永久ライセンスベース

第8章 市場推計・予測:用途別、2021-2034

- 主要動向

- 住宅用

- 商業用

- 産業

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Apex

- Beloit

- Cascade

- Easy Storage

- iStorage

- MyStorage

- OpenTech Alliance

- QuikStor

- Rentec Direct

- Secure Self Storage

- Self Storage Manager

- Shedul

- SiteLink

- Space Management

- Storage Commander

- Storage Pro Software

- storEDGE

- STORIS

- StorTrack

- Yardi Systems

目次

The Global Self-Storage Software Market was valued at USD 2.5 billion in 2024 and is estimated to grow at a CAGR of 12.7% to reach USD 8 billion by 2034, driven by the surging demand for digital solutions across the real estate sector, rapid urban migration, and the rising need for efficient space management in both residential and commercial environments. As real estate dynamics continue to evolve, self-storage businesses are increasingly turning to digital platforms to streamline operations, elevate tenant experiences, and strengthen facility security. The growing emphasis on convenience, automation, and data-driven decision-making is driving the adoption of cutting-edge software systems. Operators are seeking scalable, cloud-based tools that enable real-time monitoring, improve occupancy management, and enhance operational efficiency without the limitations of traditional infrastructure.

In today's tech-forward landscape, self-storage software plays a critical role in modernizing facility operations. With features like contactless rentals, automated billing, online payments, and real-time availability tracking, these solutions help operators stay ahead in a competitive market. Integrating customer relationship management (CRM) tools, digital access control systems and advanced analytics further allows businesses to boost visibility and improve the overall user experience. As digital security becomes more important, platforms now incorporate encryption, mobile alerts, and detailed access logs to enhance transparency and build tenant trust. The integration of emerging technologies such as predictive analytics, blockchain for secure contract management, and augmented reality (AR) for immersive virtual tours is reshaping how businesses interact with both data and customers, ultimately driving greater agility and profitability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.5 Billion |

| Forecast Value | $8 Billion |

| CAGR | 12.7% |

Cloud-based self-storage software dominates the market and accounted for nearly 60% of the global revenue in 2024. This segment's popularity stems from its flexibility, affordability, and ability to seamlessly support operations across multiple locations. Cloud platforms are easier to scale and manage, making them ideal for self-storage operators expanding their footprint. These systems allow for the implementation of artificial intelligence (AI)-driven tools, predictive maintenance schedules, and dynamic pricing models-features that are often difficult to deploy with on-premises infrastructure. Businesses benefit from centralized access, real-time updates, and minimal IT overhead, which significantly enhances performance and decision-making capabilities.

Subscription-based models have emerged as the preferred pricing structure across the self-storage software industry. These models offer unmatched affordability and integration flexibility, especially for small and mid-sized operators looking to avoid the financial burden of upfront capital investments. Through a recurring payment structure, businesses gain continuous access to the latest software features, real-time updates, technical support, and robust cybersecurity enhancements. This setup ensures operational consistency while helping operators remain compliant with changing industry standards. The subscription model also enables providers to offer more frequent product improvements, keeping businesses agile in a fast-moving digital ecosystem.

The U.S. Self-Storage Software Market reached USD 500 million in 2024 and is projected to grow at a CAGR of around 12.9%. With a well-established self-storage sector and rising consumer expectations for digital convenience, the U.S. is witnessing a significant shift toward cloud-based management platforms. Strategic investments by key software providers and government initiatives to upgrade digital infrastructure and enhance data security are further accelerating software adoption. Businesses across the country are recognizing the value of scalable, AI-enabled solutions in optimizing space utilization, improving service delivery, and ensuring regulatory compliance.

Leading players in the global self-storage software market include OpenTech Alliance, storEDGE, QuikStor, Yardi Systems, Cascade Self-Storage, and Space Management. These companies are focused on expanding their portfolios with advanced, cloud-native solutions that elevate user experience and streamline back-end processes. By leveraging AI, IoT, and blockchain technologies, they are offering smarter, more secure, and highly efficient platforms. Many are also engaging in strategic partnerships, acquisitions, and collaborative ventures to strengthen their market presence, broaden their reach, and drive innovation in the self-storage software space.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Trade impact

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.3.2 Pricing and product strategies

- 3.2.1 Trade impact

- 3.3 Technology & innovation landscape

- 3.4 Patent analysis

- 3.5 Regulatory landscape

- 3.6 Cost breakdown analysis

- 3.7 Key news & initiatives

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Digital transformation of facility management

- 3.8.1.2 Rising urbanization & space constraints

- 3.8.1.3 Demand for contactless & remote access

- 3.8.1.4 Integration with smart technologies

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High initial implementation costs

- 3.8.2.2 Data privacy & cybersecurity risks

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Cloud-based

- 5.3 On-premises

Chapter 6 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Large enterprises

- 6.3 Medium-Sized Enterprises (SME)

- 6.4 Small enterprises

Chapter 7 Market Estimates & Forecast, By Business Model, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Subscription-based

- 7.3 Perpetual License-based

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.4 Industrial

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Apex

- 10.2 Beloit

- 10.3 Cascade

- 10.4 Easy Storage

- 10.5 iStorage

- 10.6 MyStorage

- 10.7 OpenTech Alliance

- 10.8 QuikStor

- 10.9 Rentec Direct

- 10.10 Secure Self Storage

- 10.11 Self Storage Manager

- 10.12 Shedul

- 10.13 SiteLink

- 10.14 Space Management

- 10.15 Storage Commander

- 10.16 Storage Pro Software

- 10.17 storEDGE

- 10.18 STORIS

- 10.19 StorTrack

- 10.20 Yardi Systems

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日