|

市場調査レポート

商品コード

1859024

輸送用燃料電池の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Transport Fuel Cell Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 輸送用燃料電池の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年10月03日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

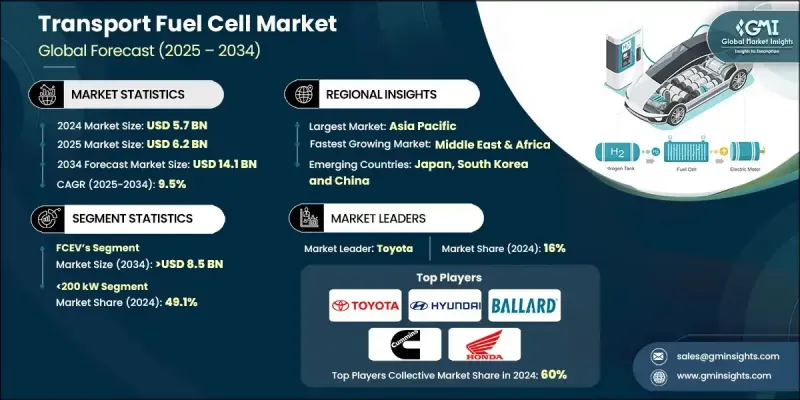

輸送用燃料電池の世界市場規模は、2024年に57億米ドルとなり、CAGR9.5%で成長し、2034年までには141億米ドルに達すると予測されています。

この成長軌道は、世界的な輸送ネットワークにおける脱炭素化とクリーンエネルギー導入の推進が高まっていることに後押しされています。耐久性の向上、コストの最適化、効率の改善など、最新の燃料電池システムの性能指標が強化されたことで、燃料電池はさまざまな輸送用途で好まれるソリューションとなっています。水素インフラが成熟し続け、主要経済国による国家水素目標が展開される中、燃料電池の実現可能性は急速に拡大しています。モビリティセクター全体の排出量削減に焦点を当てた政府の義務付けは、ゼロ・エミッション・ソリューションへの大規模なシフトを促しており、燃料電池は、特に大型、長距離、オフグリッド用途で強力な代替案を提供しています。これらのシステムは、電気モーターに電力を供給するために発電し、燃焼エンジンのような安定した出力性能を発揮しながら、テールパイプ排出を排除します。明確な勢いがあるにもかかわらず、市場は依然として、特に成熟度の低い地域では、先行投資コストの高さ、過酷な条件下での運用信頼性の問題、水素ロジスティクスの未整備と闘っています。しかし、現在進行中の投資と官民パートナーシップは、こうした制約を緩和し、世界的なアクセシビリティの向上に取り組んでいます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 57億米ドル |

| 予測金額 | 141億米ドル |

| CAGR | 9.5% |

鉄道分野は、旅客輸送と貨物輸送の両方で燃料電池の利用が増加していることを背景に、2034年までCAGR9.5%で成長します。燃料電池を動力源とする列車は、電化の遅れている鉄道網で排出ガスを出さない運行を可能にし、インフラコストを最小限に抑え、メンテナンスの軽減と静かなサービスを提供します。この技術は、持続可能な改修が必要な広大な鉄道網を持つ国々で特に魅力的なものとなっています。

容量200kW~1MWの燃料電池は、2024年に34.7%のシェアを占め、2034年までCAGR8.5%で成長すると予測されています。この出力帯域は、中型商用車、貨物用機関車、中型船舶に最適です。エネルギー出力、システムの複雑さ、コストのバランスが取れているため、多くの実輸送用途に最適です。

欧州の輸送用燃料電池市場は、欧州グリーンディール政策や水素インフラへの大規模投資の影響を受け、2034年までに30億米ドルに達すると予想されます。同地域では、鉄道用途への導入が活発で、船舶システムでの利用が拡大しています。ドイツ、ノルウェー、オランダなどの国々は、燃料電池輸送のイノベーションを積極的に形成しており、製品需要全体とインフラ支援を後押ししています。

世界の輸送用燃料電池市場の主要企業には、Toyota Motor Corporation、Ballard Power Systems、Hyundai Motor Company、Honda Motor、BorgWarner Inc.、Doosan Fuel Cell、Intelligent Energy Limited、ZF Friedrichshafen AG、Freudenberg、PowerCell Sweden、ElringKlinger、AISIN Corporation、Symbio、Nuvera Fuel Cells、Oorja Fuel Cells、AFC Energy PLC、Cummins、Wuhan Tiger Fuel Cell、Toshiba Corporation、Nedstack Fuel Cell Technologyなどがあります。輸送用燃料電池業界における地位を強化するため、主要企業は燃料電池システムの効率とライフサイクルを向上させる研究開発に多額の投資を行っています。多くの企業が自動車メーカーや鉄道メーカーと提携し、自社の技術を商用車や車両に組み込もうとしています。世界的な需要に対応し、サプライチェーンの摩擦を減らすために、生産能力を拡大し、地域的な製造ハブを構築している企業もあります。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム

- 規制情勢

- 業界への影響要因

- 成長促進要因

- 業界の潜在的リスク・課題

- 成長可能性分析

- 価格動向分析、2021年~2034年

- 最終用途別

- 地域別

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析:地域別

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

- ラテンアメリカ

- 戦略的ダッシュボード

- 戦略的取り組み

- 企業ベンチマーキング

- イノベーション・テクノロジー情勢

第5章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- PEMFC

- SOFC

- DMFC

- PAFC・AFC

- MCFC

第6章 市場規模・予測:容量別、2021年~2034年

- 主要動向

- 200 kW以下

- 200 kW~1 MW

- 1MW以上

第7章 市場規模・予測:最終用途別、2021年~2034年

- 主要動向

- 海上

- 鉄道

- FCEV

- その他

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オーストリア

- アジア太平洋地域

- 日本

- 韓国

- 中国

- インド

- フィリピン

- ベトナム

- 中東・アフリカ

- 南アフリカ

- アラブ首長国連邦

- サウジアラビア

- ラテンアメリカ

- ブラジル

- ペルー

- メキシコ

第9章 企業プロファイル

- AISIN Corporation

- AFC Energy PLC

- BorgWarner Inc

- Ballard Power Systems

- Cummins

- Doosan Fuel Cell

- ElringKlinger

- Freudenberg

- Hyundai Motor Company

- Honda Motor

- Intelligent Energy Limited

- Nuvera Fuel Cells

- Nedstack Fuel Cell Technology

- PowerCell Sweden

- Oorja Fuel Cells

- Symbio

- Toyota Motor Corporation

- Toshiba Corporation

- Wuhan Tiger Fuel Cell

- ZF Friedrichshafen AG