モノのインターネット収益化の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Internet of Things (IoT) Monetization Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

-

通信/IT

通信/IT

-

IoT

,

ビッグデータ

IoT

,

ビッグデータ

-

データ収益化

,

IoTプラットフォーム

データ収益化

,

IoTプラットフォーム

- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740950

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

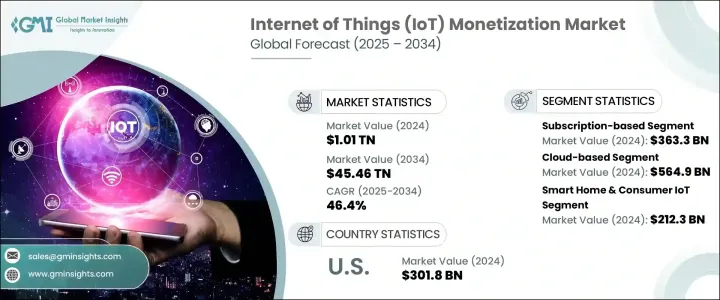

世界のIoT収益化市場は、2024年に1兆100億米ドルと評価され、CAGR46.4%で成長し、2034年までには45兆4,600億米ドルに達すると推定されています。

スマートホームやウェアラブルから産業オートメーションやコネクテッドカーまで、IoTデバイスが日常生活に深く浸透し続ける中、データとコネクティビティを収益化する範囲は指数関数的なペースで拡大しています。住宅、都市、企業の各領域にまたがるデジタルエコシステムの台頭は、収益創出に関する組織の考え方を一変させつつあります。もはや1回限りのハードウェア販売に限定されず、定期的な収入源、付加価値サービス、成果ベースの価格設定モデルに急速に焦点が移っています。

開発企業は、IoTによって生成されたデータを活用して、よりスマートな意思決定や、ニーズに合わせたユーザー体験を促進し、リアルタイムの利用状況に対応するダイナミックな価格体系を開発しています。人工知能とエッジコンピューティングが普及するにつれ、企業はリアクティブなサービスモデルを超えて、予測的・処方的な収益化戦略へと移行しつつあります。企業は、拡張性の高いIoTアプリケーションを作成するために、堅牢なクラウドインフラ、AI主導の分析、ローコードプラットフォームに投資しています。一方、サービスのバンドルやクロスプラットフォーム統合を促進するデジタルマーケットプレースの出現により、新たな収益チャネルが開かれ、顧客エンゲージメントが深まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 1兆100億米ドル |

| 予測金額 | 45兆4,600億米ドル |

| CAGR | 46.4% |

しかし、IoT収益化の展望が技術革新で活気づく一方で、複雑な国際貿易力学をナビゲートしています。米国の貿易政策の初期段階では、半導体やセンサーなどの必須部品に関税が課され、世界のサプライチェーンが混乱しました。こうした混乱がIoTハードウェアの生産コストを押し上げ、企業は顧客にコストを転嫁するか、損失を吸収するかという窮地に追い込まれました。どちらの選択肢も収益性に影響を及ぼし、特に中小ベンダーの間では導入率が鈍化しました。これに対し、一部の大手ベンダーは輸入関税を回避するために現地生産を選択しました。このシフトは、将来の貿易変動にさらされるリスクを軽減するのに役立ちますが、RandD支出の増加や投資回収までの期間の長期化といった短期的なハードルを伴う。競争力を維持するために、アセットライトビジネスモデルに傾倒する企業が増えています。これらのモデルは、ソフトウェア、プラットフォーム、サービスに重点を置き、物理的なハードウェアに大きく依存することなくIoTエコシステムを収益化することを可能にします。

2024年の市場評価額は3,633億米ドルで、サブスクリプションベースモデルが首位に立ちました。リアルタイム診断、遠隔監視、予知保全などの機能を満載したカスタマイズ可能な段階的サービスプランを提供することで、企業は1回限りのデバイス販売を長期的な収益源に変えています。このモデルにより、企業は利用状況に応じて規模を拡大できるようになり、柔軟な価格設定が可能になると同時に、顧客ロイヤルティも高めることができます。予測分析は、このような価格設定モデルを最適化する上で重要な役割を果たし、企業が実際のパフォーマンスや消費動向に合わせて料金を設定できるよう支援します。プロアクティブサポートと一貫した価値を提供できるため、ブランドロイヤルティが強化され、経常収益が促進されます。

クラウドベースのセグメントは2024年に5,649億米ドルを生み出し、その俊敏性とコスト効率の高さによってIoT収益化市場を独占しています。クラウドインフラにより、企業は高価なオンプレミスインフラに投資することなく、コネクテッドサービスを世界に展開することができます。リアルタイムのデータ収集、遠隔地からの資産管理、ソフトウェアの自動更新など、最新のIoTアプリケーションに不可欠なすべての機能が容易になります。AIを活用したソリューションを採用する企業は、クラウドプラットフォームを利用してスマートな課金システムを導入し、利用ベースの価格設定を可能にし、個々のユーザー向けにサービスをカスタマイズしています。これらの機能は、オーバーヘッドを削減しながら顧客満足度を向上させ、企業に迅速なピボットと中断のないスケーリング能力を与えています。

米国は、2024年のIoT収益化市場を3,018億米ドルでリードしました。同国は、広範な5G接続、成熟したクラウドインフラ、支援的な政策枠組みから恩恵を受けています。カリフォルニア州消費者プライバシー法(CCPA)のような法律は、匿名化され集約されたデータストリームを収益化するための扉を開く一方で、データ使用に関する明確な基準を設定しています。自動車やヘルスケアなどの産業が勢いを増しています。自動車分野では、コネクテッドカーがナビゲーションサービス、メンテナンスアラート、メディア購読などの機能を通じて収益を生み出しています。ヘルスケアでは、リモートモニタリングデバイスが、単にサービスを提供するだけでなく、患者の健康状態の改善に基づいてプロバイダーに報酬を支払う成果ベースのモデルをサポートしています。

この高成長市場で足場を固めるため、企業はクラウドの拡大を倍加し、より迅速な統合のためのローコード開発ツールを強化し、バンドルサービスの提供を可能にする異業種間パートナーシップを確立しています。各社はまた、安全で匿名化されたデータ交換に注力し、主要部門により良いサービスを提供するために、業界別ソリューションを構築しています。Microsoft、IBM、Amazon Web Services、Siemens、Googleなどの市場リーダーは、AI、クラウド、IoT機能を組み合わせた包括的なプラットフォームを提供し、業界全体で測定可能な価値を生み出すことで、こうした取り組みの先頭に立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- トランプ関税がモノのインターネット(IoT)収益化市場に与える影響

- サービス提供におけるコストインフレ

- 関税によるハードウェアコストの上昇

- ケーススタディ-AWS IoT Coreのハードウェア依存サービスの価格調整

- サプライチェーンに起因するサービス中断

- デバイスの導入遅延がサブスクリプションの展開に影響

- 負荷の高いハードウェアへの依存を軽減するためにハイブリッド(クラウド/エッジ)モデルに移行する

- セクター固有のサービスへの影響

- 産業用IoT(IIoT)サービス

- 消費者向けIoTサービス

- サービス提供におけるコストインフレ

- 業界への影響要因

- 成長促進要因

- 接続デバイスの急増

- AIと分析の進歩

- 5Gネットワークの拡張

- サブスクリプションと成果ベースのモデルへの移行

- 業界の潜在的リスク・課題

- データプライバシー規制による収益化の可能性の制限

- サービスの拡張性を妨げる相互運用性の問題

- 成長促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:ビジネスモデル別、2021年~2034年

- 主要動向

- サブスクリプションベース

- 従量課金制

- 成果に基づく

- 広告・スポンサーシップ

- データの収益化

- ライセンシング・フランチャイズ

第6章 市場推計・予測:展開タイプ別、2021年~2034年

- 主要動向

- クラウドベース

- オンプレミス

- ハイブリッド

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- スマートホーム・消費者向けIoT

- 産業用IoT

- スマートシティ

- ヘルスケアIoT

- 農業IoT

- 小売テクノロジー

- コネクテッドカー・テレマティクス

- エネルギー・ユーティリティ管理

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Microsoft

- Amazon Web Services、Inc.

- Google LLC

- IBM

- Siemens

- Cisco Systems、Inc.

- PTC

- Oracle Corporation

- SAP SE

- Telefonaktiebolaget LM Ericsson

- Verizon

- AT&T

- Bosch Global Software Technologies GmbH

- General Electric Company

- Huawei Technologies Co.、Ltd.

- Qualcomm Technologies、Inc.

- Intel Corporation

- Salesforce、Inc.

- Semtech

目次

The Global IoT Monetization Market was valued at USD 1.01 trillion in 2024 and is estimated to grow at a CAGR of 46.4% to reach USD 45.46 trillion by 2034. As IoT devices continue to embed themselves deeply into daily life-from smart homes and wearables to industrial automation and connected vehicles-the scope for monetizing data and connectivity is growing at an exponential pace. The rise of digital ecosystems across residential, urban, and enterprise domains is transforming how organizations think about revenue generation. No longer limited to one-time hardware sales, the focus has rapidly shifted to recurring income streams, value-added services, and outcome-based pricing models.

Businesses are harnessing IoT-generated data to fuel smarter decision-making, tailored user experiences, and develop dynamic pricing structures that respond to real-time usage. As artificial intelligence and edge computing gain traction, companies are moving beyond reactive service models toward predictive and prescriptive monetization strategies. Enterprises are investing in robust cloud infrastructure, AI-driven analytics, and low-code platforms to create scalable IoT applications. Meanwhile, the emergence of digital marketplaces that facilitate service bundling and cross-platform integration is unlocking new revenue channels and deepening customer engagement.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.01 Trillion |

| Forecast Value | $45.46 Trillion |

| CAGR | 46.4% |

But while the IoT monetization landscape is thriving with innovation, it's also navigating complex international trade dynamics. Tariffs on essential components such as semiconductors and sensors during earlier U.S. trade policy phases disrupted global supply chains. These disruptions pushed up production costs for IoT hardware, putting companies in a tight spot-either pass those costs to customers or absorb losses. Both options impacted profitability and slowed the rate of adoption, especially among small and mid-sized vendors. In response, some major players opted to localize production to sidestep import duties. While this shift helps reduce exposure to future trade volatility, it comes with short-term hurdles like increased RandD spending and longer timelines for return on investment. To remain competitive, a growing number of firms are leaning into asset-light business models. These models focus more on software, platforms, and services, allowing companies to monetize IoT ecosystems without depending heavily on physical hardware.

The subscription-based model took the lead in 2024 with a market valuation of USD 363.3 billion. By offering customizable, tiered service plans packed with features like real-time diagnostics, remote monitoring, and predictive maintenance, companies are turning one-time device sales into long-term revenue generators. This model gives businesses the ability to scale according to usage, allowing for flexible pricing while also boosting customer loyalty. Predictive analytics plays a key role in optimizing these pricing models, helping companies align charges with actual performance and consumption trends. The ability to deliver proactive support and consistent value strengthens brand loyalty and drives recurring revenue, making this model one of the most preferred across verticals.

The cloud-based segment generated USD 564.9 billion in 2024, dominating the IoT monetization market thanks to its agility and cost-efficiency. Cloud infrastructure enables businesses to roll out connected services globally without investing in expensive on-premises infrastructure. It facilitates real-time data collection, remote asset control, and automatic software updates-all essential for modern IoT applications. Enterprises adopting AI-powered solutions are using cloud platforms to implement smart billing systems, enable usage-based pricing, and customize services for individual users. These capabilities enhance customer satisfaction while reducing overhead, giving companies the ability to pivot quickly and scale without disruption.

The United States led the IoT monetization market with a value of USD 301.8 billion in 2024. The country benefits from widespread 5G connectivity, mature cloud infrastructure, and supportive policy frameworks. Laws like the California Consumer Privacy Act (CCPA) are setting clear standards for data usage while opening doors for monetizing anonymized and aggregated data streams. Industries such as automotive and healthcare are driving momentum. In the automotive space, connected vehicles are creating revenue through features like navigation services, maintenance alerts, and media subscriptions. In healthcare, remote monitoring devices support outcome-based models where providers are paid based on patient health improvements, not just services rendered.

To gain a stronger foothold in this high-growth market, companies are doubling down on cloud expansion, enhancing low-code development tools for faster integration, and establishing cross-industry partnerships that enable bundled service offerings. Firms are also focusing on secure, anonymized data exchanges and building vertical-specific solutions to better serve key sectors. Market leaders like Microsoft, IBM, Amazon Web Services, Siemens, and Google are spearheading these efforts by offering comprehensive platforms that combine AI, cloud, and IoT capabilities to create measurable value across industries.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Impact of trump tariffs on Internet of Things (IoT) monetization market

- 3.2.1 Cost inflation in service delivery

- 3.2.1.1 Tariff-driven hardware cost increases

- 3.2.1.2 Case study - AWS IoT core’s adjusted pricing for hardware-dependent services

- 3.2.2 Supply chain-driven service disruptions

- 3.2.2.1 Delays in device deployments impacting subscription rollouts

- 3.2.2.2 Shift to hybrid (cloud/edge) models to mitigate dependency on taxed hardware

- 3.2.3 Sector-specific service impacts

- 3.2.3.1 Industrial IoT (IIoT) services

- 3.2.3.2 Consumer IoT services

- 3.2.1 Cost inflation in service delivery

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Proliferation of connected devices

- 3.3.1.2 Advancements in AI and analytics

- 3.3.1.3 5G network expansion

- 3.3.1.4 Shift to subscription and outcome-based models

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Data privacy regulations limit monetization potential

- 3.3.2.2 Interoperability issues hinder service scalability

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Business Model, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Subscription-based

- 5.3 Pay-per-use

- 5.4 Outcome-based

- 5.5 Advertising & sponsorship

- 5.6 Data monetization

- 5.7 Licensing & franchising

Chapter 6 Market Estimates & Forecast, By Deployment Type, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Cloud-based

- 6.3 On-premises

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Smart home & consumer IoT

- 7.3 Industrial IoT

- 7.4 Smart cities

- 7.5 Healthcare IoT

- 7.6 Agriculture IoT

- 7.7 Retail technology

- 7.8 Connected vehicles & telematics

- 7.9 Energy & utility management

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Microsoft

- 9.2 Amazon Web Services, Inc.

- 9.3 Google LLC

- 9.4 IBM

- 9.5 Siemens

- 9.6 Cisco Systems, Inc.

- 9.7 PTC

- 9.8 Oracle Corporation

- 9.9 SAP SE

- 9.10 Telefonaktiebolaget LM Ericsson

- 9.11 Verizon

- 9.12 AT&T

- 9.13 Bosch Global Software Technologies GmbH

- 9.14 General Electric Company

- 9.15 Huawei Technologies Co., Ltd.

- 9.16 Qualcomm Technologies, Inc.

- 9.17 Intel Corporation

- 9.18 Salesforce, Inc.

- 9.19 Semtech

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日