|

市場調査レポート

商品コード

1740948

航空機油圧システムの市場機会、成長促進要因、産業動向分析、2025~2034年予測Aircraft Hydraulic Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 航空機油圧システムの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月25日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

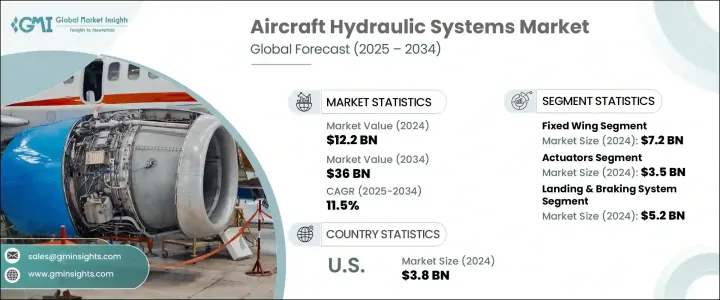

航空機油圧システムの世界市場は、2024年には122億米ドルと評価され、CAGR 11.5%で成長し、2034年には360億米ドルに達すると推定されています。

この成長の主な原動力は、世界の航空需要の増加と、商用、軍事用、無人航空機プラットフォームにおける油圧システムの統合の高まりです。航空会社が航空機をアップグレードし、政府が防衛能力を強化するにつれて、油圧システムは運用効率、信頼性、安全性を確保するために不可欠になっています。世界の航空旅客輸送量の継続的な増加は、航空宇宙企業に、より洗練された航空機に投資するよう圧力をかけており、その結果、高度な油圧アクチュエーション・システムに対するニーズが高まっています。これらのシステムは、操縦、飛行制御、ブレーキ、着陸装置の操作など、航空機のさまざまな機能に不可欠です。

関税の導入を含む近年の地政学的な貿易摩擦は、特に海外から調達する航空宇宙部品のサプライチェーンに大きな混乱をもたらしました。こうした変化により、メーカーやサプライヤーは、多様な調達戦略、現地生産、コスト変動や遅れを緩和するための調達モデルの再評価を通じて適応を余儀なくされました。その結果、地域密着型で弾力性のあるサプライチェーンへのシフトが、市場情勢を形成する重要な傾向となりつつあります。技術面では、超小型油圧システムや電気油圧システムの利用が増加しているため、市場は力強い勢いを見せています。これらの技術革新は、ドローン、自律型航空機、都市型エアモビリティビークルなどの新たなアプリケーションにおいて、コンパクトでエネルギー効率の高いソリューションに対するニーズの高まりに対応しています。さらに、防衛投資により、ステルス性、武器ハンドリング、強化された制御メカニズムなどの高度な航空機機能をサポートする高性能油圧システムの需要が引き続き高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 122億米ドル |

| 予測金額 | 360億米ドル |

| CAGR | 11.5% |

プラットフォーム別に見ると、市場は回転翼、固定翼、無人航空機(UAV)に区分されます。固定翼のカテゴリーは2024年に72億米ドルの評価額で市場をリードしました。この分野の成長には、新世代の民間航空機や防衛航空機の調達の増加、および既存の航空機の継続的なアップグレードが寄与しています。航空交通量の増加と軍事予算の拡大は、飛行制御、ブレーキ、ギア展開などの作業に複雑な油圧サブシステムを必要とする技術的に高度なジェット機の採用を促しています。

部品別に見ると、市場はリザーバ、ポンプ、アキュムレータ、アクチュエータ、油圧ヒューズ、バルブ、その他に分けられます。アクチュエータは、2024年に売上高35億米ドルのトップセグメントに浮上しました。飛行制御システムにおける精度と信頼性へのニーズの高まりが、小型で燃料効率が高く、高性能な出力が可能な次世代アクチュエータへの需要に拍車をかけています。最近の航空機は軽量化と制御応答性の向上に重点を置いているため、メーカーは進化する要件を満たすために電動油圧アクチュエータ技術への投資を増やしています。

用途別では、飛行制御システム、推力反転システム、着陸・制動システム、その他の機能が市場に含まれます。着陸・制動システム分野は2024年に52億米ドルで最も貢献しました。これらのシステムは、特に航空機が頻繁に離着陸を行う地域では、航空機の安全運航に不可欠です。需要はさらに、横滑り防止機能、圧力管理の改善、内蔵冗長性などの機能を備えたより高度な油圧コンポーネントを必要とする、より厳格な安全規制によって支えられています。

地域別では、米国が航空機油圧システム市場で最大のシェアを占めており、2024年には38億米ドルを占める。米国市場の優位性は、防衛プログラムへの投資の増加、民間航空のアップグレード、航空宇宙技術全般にわたる研究開発努力に起因しています。同国はまた、一貫して油圧システム技術を進歩させている大手航空宇宙メーカーやサプライヤーの存在からも恩恵を受けています。これらの企業は、軽量構造、電気油圧統合、MEA(More Electric Aircraft)構想に沿ったシステムに重点を置いています。

市場競争は依然として激しく、既存の多国籍企業と革新的な新興企業の両方がシェアを争っています。大手企業は、スマート油圧技術、統合診断、電気およびハイブリッド・プラットフォーム向けに設計されたソリューションに積極的に注力しています。FAA、EASA、AS9100などの世界な安全基準を満たしながら、燃料効率と環境性能を向上させた油圧システムの開発へのシフトが顕著です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 主要部品の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 世界の航空旅客数の増加

- 航空機群の拡大と近代化

- 商用、軍事、UAVプラットフォームでの使用増加

- より高いパワーウェイトレシオと荷重ハンドリング

- 油圧システムの技術的進歩

- 業界の潜在的リスク&課題

- 電気および代替システムとの競合

- 高い保守・運用コスト

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:プラットフォーム別、2021 –2034

- 主要動向

- 固定翼

- 回転翼

- 無人航空機

第6章 市場推計・予測:コンポーネント別、2021 –2034

- 主要動向

- リザーバー

- ポンプ

- アキュムレータ

- アクチュエータ

- 油圧ヒューズ

- バルブ

- その他

第7章 市場推計・予測:用途別、2021 –2034

- 主要動向

- 飛行制御システム

- 推力反転システム

- 着陸およびブレーキシステム

- その他

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- AeroControlex

- Circor Aerospace

- Collins Aerospace

- Crane Aerospace and Electronics

- Eaton

- Gar Kenyon

- Liebherr Aerospace

- Moog

- Parker Hannifin

- PTI Technologies

- Safran

- Senior

- Triumph Group

- Woodward

The Global Aircraft Hydraulic Systems Market was valued at USD 12.2 billion in 2024 and is estimated to grow at a CAGR of 11.5% to reach USD 36 billion by 2034. This growth is largely driven by the increasing global demand for air travel and the rising integration of hydraulic systems across commercial, military, and unmanned aerial vehicle platforms. As airlines upgrade fleets and governments ramp up defense capabilities, hydraulic systems have become critical for ensuring operational efficiency, reliability, and safety. The continued rise in global air passenger traffic is putting pressure on aerospace companies to invest in more sophisticated aircraft, which in turn is driving the need for advanced hydraulic actuation systems. These systems are essential for various aircraft functions, including maneuvering, flight control, braking, and landing gear operation.

Geopolitical trade tensions in recent years, including the introduction of tariffs, have caused significant disruption in the supply chain, particularly for aerospace components sourced from overseas. These changes forced manufacturers and suppliers to adapt through diversified sourcing strategies, local production, and reevaluation of procurement models to mitigate cost fluctuations and delays. As a result, the shift toward localized and resilient supply chains is becoming a crucial trend shaping the market landscape. On the technology front, the market is experiencing strong momentum due to the rising use of micro and electro-hydraulic systems. These innovations cater to the growing need for compact and energy-efficient solutions in emerging applications such as drones, autonomous aircraft, and urban air mobility vehicles. Moreover, defense investments continue to boost the demand for high-performance hydraulic systems that support advanced aircraft functionalities like stealth, weapons handling, and enhanced control mechanisms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.2 Billion |

| Forecast Value | $36 Billion |

| CAGR | 11.5% |

In terms of platform, the market is segmented into rotary wing, fixed wing, and unmanned aerial vehicles (UAVs). The fixed wing category led the market in 2024 with a valuation of USD 7.2 billion. The growth of this segment is fueled by an increase in procurement of new-generation commercial and defense aircraft as well as ongoing upgrades to existing fleets. Rising air traffic and expanded military budgets are encouraging the adoption of technologically advanced jets that require complex hydraulic subsystems for tasks such as flight control, braking, and gear deployment.

By component, the market is divided into reservoirs, pumps, accumulators, actuators, hydraulic fuses, valves, and others. Actuators emerged as the top-performing segment in 2024, generating USD 3.5 billion in revenue. The heightened need for accuracy and reliability in flight control systems is spurring demand for next-generation actuators that are compact, fuel-efficient, and capable of high-performance output. As modern aircraft focus on weight reduction and improved control responsiveness, manufacturers are increasingly investing in electro-hydraulic actuator technologies to meet evolving requirements.

On the basis of application, the market includes flight control systems, thrust reversal systems, landing and braking systems, and other functions. The landing and braking systems segment was the highest contributor in 2024, valued at USD 5.2 billion. These systems are essential for the safe operation of aircraft, especially in regions where aircraft perform frequent takeoffs and landings. Demand is further supported by stricter safety regulations, which require more advanced hydraulic components with features like anti-skid capabilities, improved pressure management, and built-in redundancies.

Regionally, the United States held the largest share of the aircraft hydraulic systems market, accounting for USD 3.8 billion in 2024. The dominance of the US market can be attributed to rising investments in defense programs, commercial aviation upgrades, and R&D efforts across aerospace technologies. The country also benefits from the presence of major aerospace manufacturers and suppliers who are consistently advancing hydraulic system technologies. These companies are placing emphasis on lightweight construction, electro-hydraulic integrations, and systems that align with More Electric Aircraft (MEA) initiatives.

Market competition remains intense, with both established multinational companies and innovative startups competing for share. Leading players are actively focusing on smart hydraulic technologies, integrated diagnostics, and solutions designed for electric and hybrid platforms. There is a noticeable shift toward developing hydraulic systems that offer enhanced fuel efficiency and environmental performance while meeting global safety standards such as FAA, EASA, and AS9100.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising global air passenger traffic

- 3.3.1.2 Expansion and modernization of aircraft fleets

- 3.3.1.3 Increased use in commercial, military, and UAV platforms

- 3.3.1.4 Higher power-to-weight ratios and load handling

- 3.3.1.5 Technological advancements in hydraulic systems

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Competition from electric and alternative systems

- 3.3.2.2 High maintenance and operational costs

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Platform, 2021 – 2034 (USD Million & Million Units)

- 5.1 Key trends

- 5.2 Fixed wing

- 5.3 Rotary wing

- 5.4 Unmanned aerial vehicles

Chapter 6 Market Estimates and Forecast, By Component, 2021 – 2034 (USD Million & Million Units)

- 6.1 Key trends

- 6.2 Reservoir

- 6.3 Pumps

- 6.4 Accumulators

- 6.5 Actuators

- 6.6 Hydraulic fuse

- 6.7 Valves

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million & Million Units)

- 7.1 Key trends

- 7.2 Flight control system

- 7.3 Thrust reversal system

- 7.4 Landing & braking system

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Million Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AeroControlex

- 9.2 Circor Aerospace

- 9.3 Collins Aerospace

- 9.4 Crane Aerospace and Electronics

- 9.5 Eaton

- 9.6 Gar Kenyon

- 9.7 Liebherr Aerospace

- 9.8 Moog

- 9.9 Parker Hannifin

- 9.10 PTI Technologies

- 9.11 Safran

- 9.12 Senior

- 9.13 Triumph Group

- 9.14 Woodward