水産養殖用飼料押出成形の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Aquaculture Feed Extrusion Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740947

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

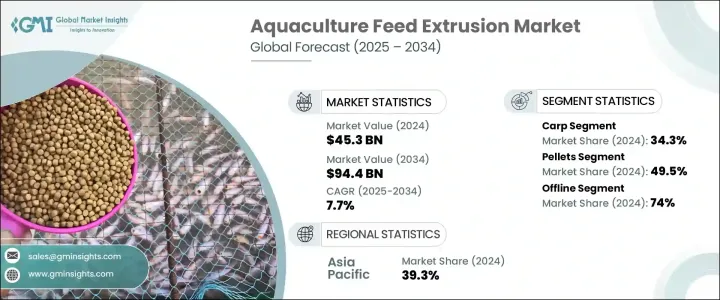

世界の水産養殖用飼料押出成形市場は、2024年に453億米ドルと評価され、CAGR 7.7%で成長し、2034年には944億米ドルに達すると推定されています。

過去10年間、この市場は着実な拡大を目の当たりにしてきたが、その主な要因は高タンパク質魚介類に対する需要の高まりと、集約的な養殖方法への世界のシフトです。伝統的な給餌方法は、栄養価が高く、水に安定した飼料の選択肢を提供する、より高度な押出技術に取って代わられました。これらの技術革新は、飼料の効率と動物の健康を向上させただけでなく、養殖システムが環境に与える影響も最小限に抑えています。正確な配合と的を絞った栄養補給を可能にする飼料押出成形は、多様な水生種の食事ニーズを満たすために不可欠なものとなっています。押出成型飼料は消化率、安定性、転換率の点で利点があり、商業的経営において好ましい選択となっています。改良された設備技術は、世界の飼料生産者にも地域的な飼料生産者にも、規模に応じた飼料のソリューションを作り出す能力を与えることで、この移行をさらに後押ししています。

魚種ごとの飼料需要が引き続き市場力学を形成しています。2024年には、鯉が34.3%と魚種別で最大の市場シェアを占め、飼料生産の費用対効果と応用のしやすさがその原動力となっています。水生種はそれぞれ栄養面や成長面で異なる課題を抱えているため、飼料の配合や押出成形の要件が複雑になっています。肉食性の魚種はタンパク質が豊富なエクストルージョン製剤の恩恵を受ける一方で、メーカーは特にコストに敏感な地域において、手頃な価格を維持する必要に迫られています。栄養価に優れ、水に安定した飼料へのシフトは、魚の健康状態を改善し、水生環境における重要な懸念事項である栄養分の溶出を最小限に抑えるための中心的な課題です。同時に養殖業者は、消費中の監視が容易で、特に大量養殖セットアップにおいて全体的な無駄の削減に貢献する飼料を求めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 453億米ドル |

| 予測金額 | 944億米ドル |

| CAGR | 7.7% |

例えばティラピアの飼料生産では、魚粉への依存を減らすために植物性タンパク質への移行が見られ、より持続可能な飼料原料への移行を後押ししています。ナマズ用飼料は一般的に低タンパクで、沈むペレット状であるが、集約的養殖経営における消化性の高い飼料へのニーズの高まりに対応するため、再評価が進んでいます。飼料要求率がますます厳しくなる中、生産者は品質とコストのバランスを取ることに取り組んでおり、経費を増やすことなく効率を維持することを目指しています。

飼料の種類別に分類すると、2024年の水産養殖用飼料押出成形市場はペレットが49.5%のシェアでリードしています。ペレットはCAGR 7.3%で拡大し続けると予想され、これは飼料供給の一貫性と性能を求める大規模養殖施設からの需要によるものです。浮力、水安定性、高栄養負荷の運搬能力により、幅広い水生種に理想的です。エクストルージョンの開発により、特定の摂餌行動や環境条件を満たす、特殊なフローティングペレットやスローシンキングペレットの開発が可能になりました。しかし、高級ペレット飼料は生産コストが高く、予算が限られている小規模生産者にとってはハードルとなりうる。

顆粒は、その小ささと摂取のしやすさから、水生幼生種に広く使用されています。便利ではあるが、水に対する安定性が十分でないことが多く、廃棄物が多くなり、高密度のシステムでは慎重な管理が必要となります。一般に孵化場で初期段階の魚やエビに使用される粉末飼料は、必須栄養素を供給するが、過剰給餌や水質悪化を避けるために正確な散布が要求されます。

市場の流通経路はオンラインとオフラインに分かれます。2024年には、オフライン販売が市場を独占し、総売上の74%を占める。このチャネルは主要養殖地域における存在感が強いため、CAGR 8.9%の堅調な成長が見込まれます。オフライン・チャネルは、柔軟な支払い条件、カスタマイズされた栄養計画、在庫供給の準備など、個別化されたサポートにより人気があります。これらの要素は、養殖インフラが確立されている地域では特に重要です。

地域別では、アジア太平洋が2024年の売上高シェア39.3%で世界市場をリードしています。この地域は、高い養殖生産高と、飼料の近代化と持続可能性を目指した政府の有利な取り組みから利益を得ています。中国、インド、東南アジアなどの市場は、水産物消費の増加と飼料効率向上の努力により、引き続き地域の優位性を牽引しています。対照的に、北米のような地域は、持続可能な水産養殖の実践に対する意識の高まりと地元産の水産物への注目によって、緩やかではあるが着実な成長を示しています。

市場をリードする企業には、ADM、Cargill、Biomar、Purina Animal Nutrition LLC、Skretting、DSM、Aller Aqua Groupなどがあります。これらの企業は、技術革新、タンパク質源の多様化、環境に配慮した飼料製品の開拓を通じて、市場の状況を形成しています。これらの企業の努力は、世界規模の事業と地域ごとの飼料のカスタマイズの両方をサポートし、全体的な水産養殖用飼料押出成形エコシステムを強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 貿易統計(HSコード)

- 主要輸出国、2021-2024

- 主要輸入国、2021-2024

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 供給側の影響(原材料)

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 持続可能な代替原料への移行

- 飼料押出における技術の進歩

- 高性能機能性飼料の需要の高まり

- 業界の潜在的リスク&課題

- 不安定な価格

- 原材料の入手が限られている

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:種別、2021 –2034

- 主要動向

- 鯉

- 海産エビ

- ティラピア

- ナマズ

- 海水魚

第6章 市場推計・予測:飼料種別、2021 –2034

- 主要動向

- ペレット

- 顆粒

- 粉

- その他

第7章 市場推計・予測:流通チャネル別、2021 –2034

- 主要動向

- オンライン

- オフライン

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Cargill

- ADM

- Biomar

- Skretting

- Purina Animal Nutrition llc.

- Marubeni Nisshin Feed co.,ltd.

- Fish Feed Extruder

- DSM

- Aller Aqua Group

- Heritage Nutrient Limited

目次

The Global Aquaculture Feed Extrusion Market was valued at USD 45.3 billion in 2024 and is estimated to grow at a CAGR of 7.7% to reach USD 94.4 billion by 2034. Over the last decade, this market has witnessed steady expansion, largely fueled by the rising demand for high-protein seafood and the global shift toward intensive aquaculture practices. Traditional feeding methods have given way to more advanced extrusion techniques that provide nutrient-dense, water-stable feed options. These innovations have not only improved feed efficiency and animal health but have also minimized the environmental impact of aquaculture systems. Feed extrusion, which allows for precise formulation and targeted nutrition, has become critical to meeting the dietary needs of diverse aquatic species. Extruded feeds offer advantages in terms of digestibility, stability, and conversion rates, making them the preferred choice across commercial operations. Enhanced equipment technology has further supported this transition by giving both global and regional feed producers the ability to create tailored feed solutions at scale.

Species-specific feed demand continues to shape market dynamics. In 2024, carp held the largest market share by species at 34.3%, driven by the cost-effectiveness of feed production and ease of application. Each aquatic species poses different nutritional and growth challenges, contributing to the complexity of feed formulation and extrusion requirements. While carnivorous species benefit from protein-rich extruded formulations, manufacturers are also being pushed to maintain affordability-particularly in cost-sensitive regions. The shift toward nutritionally superior, water-stable feeds is central to improving fish health and minimizing nutrient leaching, which remains a key concern in aquatic environments. At the same time, farmers seek feeds that are easy to monitor during consumption and contribute to reducing overall wastage, especially in high-volume farming setups.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $45.3 Billion |

| Forecast Value | $94.4 Billion |

| CAGR | 7.7% |

Tilapia feed production, for instance, has seen a transition toward plant-based proteins to reduce reliance on fishmeal, supporting the move toward more sustainable feed ingredients. Catfish feeds, typically lower in protein and presented in sinking pellet forms, are being re-evaluated to meet the rising need for highly digestible feed in intensive farming operations. As feed conversion ratios come under greater scrutiny, producers are working to strike a balance between quality and cost, aiming to maintain efficiency without driving up expenses.

When categorized by feed type, pellets led the aquaculture feed extrusion market in 2024 with a 49.5% share. Pellets are expected to continue expanding at a CAGR of 7.3%, driven by demand from large-scale aquaculture facilities seeking consistency and performance in feed delivery. Their buoyancy, water stability, and ability to carry high nutrient loads make them ideal for a broad range of aquatic species. Ongoing advances in extrusion allow for the development of specialized floating and slow-sinking pellet types that meet specific feeding behaviors and environmental conditions. However, premium pellet feeds come with high production costs, which can be a hurdle for small-scale producers with limited budgets.

Granules remain widely used for juvenile aquatic species due to their small size and ease of intake. Although they are convenient, they often lack sufficient water stability, leading to higher waste and requiring careful management in high-density systems. Powdered feed, generally used in hatcheries for early-stage fish and shrimp, delivers essential nutrients but demands precise application to avoid overfeeding and deterioration in water quality.

The market's distribution channels are divided into online and offline modes. In 2024, offline sales dominated the market, accounting for 74% of total revenue. This channel is expected to grow at a robust CAGR of 8.9% due to its strong presence in key aquaculture regions. Offline channels are popular due to the personalized support they provide, including flexible payment terms, customized nutritional planning, and ready inventory supply. These factors are especially important in regions with well-established aquaculture infrastructure.

Regionally, Asia Pacific led the global market with a 39.3% revenue share in 2024. The region benefits from high aquaculture output and favorable government initiatives aimed at feed modernization and sustainability. Markets such as China, India, and Southeast Asia continue to drive regional dominance, with increasing seafood consumption and efforts to enhance feed efficiency. In contrast, regions like North America show moderate but steady growth, driven by growing awareness of sustainable aquaculture practices and a focus on locally sourced seafood.

Leading market players include ADM, Cargill, Biomar, Purina Animal Nutrition LLC, Skretting, DSM, and Aller Aqua Group. These companies shape the market landscape through innovation, diversification of protein sources, and development of environmentally conscious feed products. Their efforts support both global scale operations and localized feed customization, strengthening the overall aquaculture feed extrusion ecosystem.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Impact on trade

- 3.1.8 Trade volume disruptions

- 3.2 Retaliatory measures

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries, 2021-2024 (Kilo Tons)

- 3.3.2 Major importing countries, 2021-2024 (Kilo Tons)

- 3.4 Impact on the industry

- 3.4.1 Supply-Side impact (raw materials)

- 3.4.1.1 Price volatility in key materials

- 3.4.1.2 Supply chain restructuring

- 3.4.1.3 Production cost implications

- 3.4.1 Supply-Side impact (raw materials)

- 3.5 Demand-side impact (selling price)

- 3.5.1 Price transmission to end markets

- 3.5.2 Market share dynamics

- 3.5.3 Consumer response patterns

- 3.6 Key companies impacted

- 3.7 Strategic industry responses

- 3.7.1 Supply chain reconfiguration

- 3.7.2 Pricing and product strategies

- 3.7.3 Policy engagement

- 3.8 Outlook and Future considerations

- 3.9 Supplier landscape

- 3.10 Profit margin analysis

- 3.11 Key news & initiatives

- 3.12 Regulatory landscape

- 3.13 Impact forces

- 3.13.1 Growth drivers

- 3.13.1.1 Shift toward sustainable and alternative ingredients

- 3.13.1.2 Technological advancements in feed extrusion

- 3.13.1.3 Rising demand for high-performance functional feeds

- 3.13.2 Industry pitfalls & challenges

- 3.13.2.1 Volatile pricing

- 3.13.2.2 Limited availability of raw materials

- 3.13.1 Growth drivers

- 3.14 Growth potential analysis

- 3.15 Porter's analysis

- 3.16 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Species, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Carp

- 5.3 Marine shrimps

- 5.4 Tilapias

- 5.5 Catfishes

- 5.6 Marine fishes

Chapter 6 Market Estimates and Forecast, By Feed Type, 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Pellets

- 6.3 Granules

- 6.4 Powder

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Online

- 7.3 Offline

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Cargill

- 9.2 ADM

- 9.3 Biomar

- 9.4 Skretting

- 9.5 Purina Animal Nutrition llc.

- 9.6 Marubeni Nisshin Feed co.,ltd.

- 9.7 Fish Feed Extruder

- 9.8 DSM

- 9.9 Aller Aqua Group

- 9.10 Heritage Nutrient Limited

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日