|

市場調査レポート

商品コード

1740940

セラコート市場の市場機会、成長促進要因、産業動向分析と2025~2034年予測Cerakote (Ceramic-Based Coating) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| セラコート市場の市場機会、成長促進要因、産業動向分析と2025~2034年予測 |

|

出版日: 2025年04月30日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

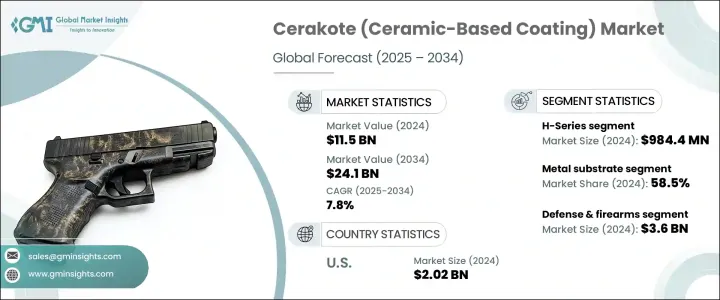

セラコート(セラミックベースコーティング)の世界市場は、2024年に115億米ドルと評価され、CAGR 7.8%で成長し、2034年には241億米ドルに達すると推定されています。

同市場は、技術基準を満たすだけでなく、さまざまな産業でカスタマイズされた機能を提供するコーティングに対する需要の増加により、力強い成長を遂げています。この急成長の主な要因は、耐久性、耐食性、美観を備えた高性能コーティングのニーズが高まっていることです。製造工程がより専門的になるにつれ、業界特有の要件や環境耐性に適合するセラミックベースのコーティングの採用が増加しています。機能性と洗練された外観を併せ持つセラコートは、様々な最終用途分野で好まれています。中でもエレクトロニクスは、消費者層の拡大と、耐熱性、耐摩耗性、高級感のある仕上がりを提供する耐久性コーティングに対する需要の高まりにより、顕著な牽引力となっています。これらの品質により、セラコートは厳しい条件にさらされる基材をコーティングするためのトップクラスのソリューションとして位置づけられています。

Hシリーズは製品セグメントをリードし、2024年には9億8,440万米ドルと評価されました。このシリーズは2025年から2034年にかけてCAGR 8.4%を記録すると予想されています。耐薬品性、耐腐食性、耐摩耗性を併せ持つこのシリーズは、商業的に最も成功した製品ラインです。その効果は、性能と外観の両方が重要な数多くの産業用途で信頼できることが証明されています。この市場には、C-Series、Elite Series、Glacier Series、Clear Coatsといった他の製品ラインもあり、それぞれがさまざまな用途のニーズに合わせて特定の性能基準を満たすように開発されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 115億米ドル |

| 予測金額 | 241億米ドル |

| CAGR | 7.8% |

セラコートコーティングは基材適合性に基づいて分類され、金属、ポリマー・プラスティック、複合材料、木材が主な材料カテゴリーとなっています。金属は2024年の世界市場シェアの58.5%を占め、この分野を支配しています。この優位性は、環境暴露、耐摩耗性、長寿命が不可欠な産業で金属部品が広く使用されていることに起因します。セラコートは、鉄と非鉄の両方の金属に優れた密着性を発揮するため、高負荷のかかる環境でもその魅力を発揮します。セラコートの分子結合能力は、製造業や頑丈な用途で使用される金属の補強に重要な役割を果たしています。

ポリマーやプラスチックは、一般的にCシリーズで塗装され、常温で硬化し、基材の構造的完全性を維持します。これとは対照的に、木質基材はコーティングの耐湿性と耐傷性の恩恵を受け、特に表面デザインが重要な美観重視の用途に適しています。これらのコーティングは単に保護するだけでなく、素材の耐久性を犠牲にすることなく、創造的なカスタマイズを可能にします。

最終用途産業別では、防衛・銃器分野が最大の貢献者に浮上し、2024年の市場規模は36億米ドル、2034年までの予想CAGRは6.7%でした。この分野は市場全体の31%を占め、過酷な条件下でも信頼性の高い性能を発揮するコーティングへの需要が高まっていることが背景にあります。セラコートの熱安定性と耐摩耗性は、性能と表面の完全性が重要な戦術的装備や兵器に特に適しています。

セラコート市場の塗布方法は、主にスプレー塗装、熱硬化、風乾に分類されます。スプレーコーティングは、均一で薄い層を効率的に形成できるため、引き続きリードしています。熱硬化は主に、最高の耐久性と耐薬品性が要求される状況で適用され、風乾はプラスチック、複合材料、木材など、熱に弱い基材に適しています。

2024年には、米国が20億2,000万米ドルの評価額で世界市場で大きなシェアを占めています。国内市場は、2025年から2034年にかけてCAGR 7.8%で成長すると予測されています。自動車、軍事、消費財などの高性能産業からの需要の増加が成長を後押しし続けています。カスタマイズされた美的仕上げと部品ライフサイクルの延長が市場拡大の主な要因です。耐久性コーティングと業界標準に関する規制意識も、セラミックベースのソリューションの採用増加につながっています。

大手メーカーは技術革新、戦略的提携、世界な販売網の拡大に多額の投資を行っており、競合環境は激化しています。一流企業は、生産技術の最適化、製品品質の一貫性の維持、OEMおよびアフターマーケットチャネルでのプレゼンス強化に注力しています。主要企業はまた、ブランドの信頼と顧客ロイヤルティを構築するために、認証、社内試験能力、技術サービスを優先しています。高性能で見た目も美しいコーティングへの需要が高まる中、メーカーは先進的な研究開発とプロセス開発を通じて期待に応えようと競い合っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国

- 主要輸入国

注:上記の貿易統計は主要国についてのみ提供されます

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 銃器および防衛分野における高性能コーティングの需要が高まっています

- 自動車のカスタマイズとアフターマーケットサービスの増加

- 軽量で高熱の部品として航空宇宙分野での使用が増加しています

- 産業機器における高温コーティングの需要急増

- 業界の潜在的リスク&課題

- 従来のコーティングに比べて、塗布と硬化のコストが高くなります

- ブランドの在庫が限られています

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- Hシリーズ

- Cシリーズ

- エリートシリーズ

- 氷河シリーズ

- クリアコート

第6章 市場推計・予測:基材適合性別、2021-2034

- 主要動向

- 金属

- 鋼鉄

- アルミニウム

- チタン

- ポリマーとプラスチック

- 複合材料

- 木材

第7章 市場推計・予測:用途別業界、2021-2034

- 主要動向

- 防衛と銃器

- 自動車・輸送

- 航空宇宙および航空

- 家電

- 医療機器

- 産業機器

- スポーツ・アウトドア用品

第8章 市場推計・予測:用途別、2021-2034

- 主要動向

- スプレーコーティング

- 熱硬化

- 空気乾燥

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Arrow Finishing

- Cerakote

- KECO Coatings

- KOTEC Ceramic Coatings

- MSP Manufacturing

- Mueller Coatings

- NIC Industries

- Spectrum Coating

- Sun Coating Company

- Tanury Industries

The Global Cerakote (Ceramic-Based Coating) Market was valued at USD 11.5 billion in 2024 and is estimated to grow at a CAGR of 7.8% to reach USD 24.1 billion by 2034. The market is experiencing robust growth due to the increasing demand for coatings that not only fulfill technical standards but also deliver tailored functionality across different industries. This surge is primarily driven by the rising need for high-performance coatings that offer durability, corrosion resistance, and aesthetic appeal. As manufacturing processes become more specialized, there's growing adoption of ceramic-based coatings that align with industry-specific requirements and environmental resilience. Cerakote's ability to combine functionality with visual sophistication makes it a preferred choice across various end-use sectors. Among these, electronics are witnessing notable traction due to the expanding consumer base and the growing demand for durable coatings that offer heat resistance, wear protection, and a premium finish on devices and accessories. These qualities have positioned cerakote as a top-tier solution for coating substrates exposed to demanding conditions.

The H-Series led the product segment and was valued at USD 984.4 million in 2024. This series is anticipated to witness a CAGR of 8.4% between 2025 and 2034. It remains the most commercially successful product line due to its strong combination of chemical resistance, corrosion protection, and wear durability. Its effectiveness has proven reliable across numerous industrial uses where both performance and appearance matter. The market comprises other product lines as well, such as the C-Series, Elite Series, Glacier Series, and Clear Coats, each developed to meet specific performance benchmarks in line with various application needs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.5 Billion |

| Forecast Value | $24.1 Billion |

| CAGR | 7.8% |

Cerakote coatings are classified based on substrate compatibility, with metals, polymers & plastics, composites, and wood serving as the primary material categories. Metals dominated the segment in 2024, accounting for 58.5% of the global market share. This dominance stems from the widespread use of metallic components in industries where environmental exposure, wear resistance, and longevity are essential. The coating's superior adhesion to both ferrous and non-ferrous metals adds to its attractiveness in high-stress environments. Cerakote's molecular bonding capability plays a significant role in reinforcing metals used in manufacturing and heavy-duty applications.

Polymers and plastics are typically coated with C-Series formulations, which cure at ambient temperatures to maintain the structural integrity of the base materials. In contrast, wood substrates benefit from the coating's moisture resistance and scratch protection, especially in aesthetic-focused uses where surface design matters. These coatings offer more than just protection; they allow for creative customization without sacrificing material durability.

In terms of end-use industries, the defense and firearms sector emerged as the largest contributor, with a market value of USD 3.6 billion in 2024 and an expected CAGR of 6.7% through 2034. This segment represented 31% of the overall market, driven by growing demand for coatings that perform reliably under extreme conditions. The thermal stability and abrasion resistance of cerakote make it particularly suitable for tactical equipment and weaponry, where performance and surface integrity are critical.

Application methods in the cerakote market are primarily segmented into spray coating, heat curing, and air drying. Spray coating continues to lead due to its efficiency in producing even, thin layers, which is critical for applications where visual appeal and smooth finishes are essential. Heat curing is mainly applied in situations that demand peak durability and chemical resistance, whereas air drying is more appropriate for heat-sensitive substrates, including plastics, composites, and wood.

In 2024, the United States held a significant share of the global market, with a valuation of USD 2.02 billion. The domestic market is forecasted to grow at a 7.8% CAGR between 2025 and 2034. Increased demand from high-performance industries such as automotive, military, and consumer goods continues to boost growth. Customized aesthetic finishes and extended component lifecycles are key drivers for market expansion. Regulatory awareness around durable coatings and industry standards has also led to increased adoption of ceramic-based solutions.

The competitive environment is intensifying as leading manufacturers invest heavily in innovation, strategic collaborations, and expansion of global distribution networks. Top-tier companies are focusing on optimizing production techniques, maintaining consistency in product quality, and strengthening their presence across OEM and aftermarket channels. Key players are also prioritizing certifications, in-house testing capabilities, and technical services to build brand trust and customer loyalty. As demand for high-performance and visually appealing coatings grows, manufacturers are racing to meet expectations through advanced R&D and process development.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising demand for high-performance coatings in firearms and defense.

- 3.7.1.2 Increasing automotive customization and aftermarket services.

- 3.7.1.3 Growing use in aerospace for lightweight, high-heat components.

- 3.7.1.4 Surge in demand for high-temperature coatings in industrial equipment

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High application and curing costs compared to traditional coatings.

- 3.7.2.2 Limited brand availability.

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 H-series

- 5.3 C-series

- 5.4 Elite series

- 5.5 Glacier series

- 5.6 Clear coats

Chapter 6 Market Estimates & Forecast, By Substrate Compatibility, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Metals

- 6.2.1 Steel

- 6.2.2 Aluminum

- 6.2.3 Titanium

- 6.3 Polymers & plastics

- 6.4 Composites

- 6.5 Wood

Chapter 7 Market Estimates & Forecast, By Application Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Defense & firearms

- 7.3 Automotive & transportation

- 7.4 Aerospace & aviation

- 7.5 Consumer electronics

- 7.6 Medical devices

- 7.7 Industrial equipment

- 7.8 Sporting & outdoor goods

Chapter 8 Market Estimates & Forecast, By Application Method, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Spray coating

- 8.3 Heat curing

- 8.4 Air drying

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Arrow Finishing

- 10.2 Cerakote

- 10.3 KECO Coatings

- 10.4 KOTEC Ceramic Coatings

- 10.5 MSP Manufacturing

- 10.6 Mueller Coatings

- 10.7 NIC Industries

- 10.8 Spectrum Coating

- 10.9 Sun Coating Company

- 10.10 Tanury Industries