|

市場調査レポート

商品コード

1740938

商用車用クランクシャフトの市場機会、成長促進要因、産業動向分析、2025~2034年予測Commercial Vehicle Crankshaft Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 商用車用クランクシャフトの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月17日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

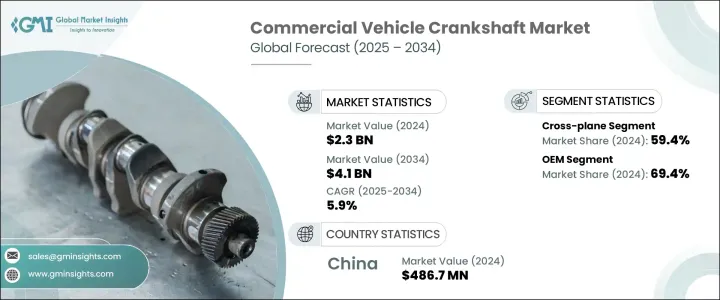

商用車用クランクシャフトの世界市場規模は、2024年に23億米ドルとなり、商用車生産の増加や世界の輸送・物流分野の急速な拡大により、CAGR 5.9%で成長し、2034年には41億米ドルに達すると予測されています。

世界の産業界がゼロエミッション目標に向けた競争を繰り広げる中、より効率的でクリーンな車両技術の必要性がクランクシャフト業界全体に大きな勢いをもたらしています。ハイブリッド、電気、過渡的なパワートレインに対する需要の高まりは、材料要件と期待性能を変化させ、メーカーに軽量で耐久性の高いクランクシャフトソリューションの革新を促しています。フリートオペレータは、従来の内燃システムと電化プラットフォームの橋渡しをする次世代商用車への投資を増やしており、効率性と信頼性の両方を実現する高性能コンポーネントの必要性を高めています。サプライチェーンダイナミクスの進化、排ガス規制の強化、燃費重視の高まりにより、OEMとサプライヤーは従来のクランクシャフト設計を再考する必要に迫られています。各社は現在、よりスマートな予知保全技術、軽量合金、精密製造技術に資源を投入し、世界のフリート基準の高まりに対応しています。特に、物流トラックやバスなどの大型セグメントでは、ビークル・ツー・グリッド(V2G)システムの採用が拡大しており、エンジン性能を最大化しながら持続可能性をサポートする高度なクランクシャフト設計の継続的なニーズがさらに高まっています。

商用車のスマートグリッドシステムへの統合が進んでいることも、クランクシャフトの設計要件に影響を与えています。V2Gネットワークに参加する車両は、この過渡期においても内燃エンジンやハイブリッドエンジンに大きく依存しているため、低排出ガスと燃費向上をサポートするクランクシャフトが極めて重要になります。この動向は、レガシーシステムと将来を見据えたモビリティソリューションの融合を目指す、より広範な自動車シフトに直結しています。バリューチェーン全体において、OEMと部品メーカーは、耐熱性と振動制御に優れた軽量・高強度クランクシャフトの開発を優先しています。同時に、北米、欧州、アジアでは、排出ガス削減をターゲットとした規制上のインセンティブにより、高性能クランクシャフト技術への投資が加速しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 23億米ドル |

| 予測金額 | 41億米ドル |

| CAGR | 5.9% |

2024年には、クロスプレーン・クランクシャフトセグメントが59.4%の市場シェアを占め、その主な理由は振動減衰、トルクの安定性、動的バランスに優れているためです。これらの特徴は、長距離トラックや産業用バスなど、さまざまな地形で極端な負荷条件下で運転される大型車両に不可欠です。また、クロスプレーン・クランクシャフトは、大排気量エンジンやハイブリッドエンジンとの互換性を高め、最適な燃料効率とドライバビリティに不可欠なスムーズなトルク伝達を実現します。

販売チャネルの観点からは、OEMが2024年に69.4%の圧倒的なシェアを占め、2034年までのCAGRは6.8%と予測されています。OEMは、強度、耐疲労性、熱効率を優先した用途別鍛造設計を共同開発するため、クランクシャフトメーカーとの協力関係を強めています。

中国商用車用クランクシャフト市場シェアは54.2%で世界をリードし、2024年には4億8,670万米ドルを創出します。中国の優位性は、大規模な商用車生産規模と垂直統合されたサプライチェーンに起因します。重慶、済南、広州といった都市は、政府のイニシアティブ、熟練労働者プール、強力なOEMパートナーシップに支えられ、主要製造拠点として台頭してきました。自動鍛造ライン、ロボット加工、厳格な品質管理への投資が、中国の主導的地位を強化しています。

世界市場の主要企業には、Bharat Forge、thyssenkrupp、MAHLE、Rheinmetall、Kellogg Crankshaft Company、Crower Cams &Equipment、NSI Crankshaft、ZF Friedrichshafen、Nippon Steel、Tianrun Industrial Technologyなどがあります。業界大手は、高強度・低重量材料の研究開発を優先し、CNC自動化を強化し、OEMとの連携を深め、デジタル統合を進めてメンテナンスを追跡し、排出ガス性能を最適化することで、進化する商用モビリティの状況に対応しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 製造業者

- 原材料サプライヤー

- 自動車OEM

- 流通チャネル

- 最終用途

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(顧客へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 価格分析

- 推進

- 地域

- 影響要因

- 促進要因

- 商用車の需要増加

- 運輸・物流部門の拡大

- 軽量・高強度素材の採用

- 商用車用クランクシャフトにおける継続的な技術進歩

- 業界の潜在的リスク&課題

- 製造コストが高め

- サプライチェーンの混乱

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:クランクシャフト別、2021-2034

- 主要動向

- 平面

- 交差面

- モジュラー

第6章 市場推計・予測:材料別、2021-2034

- 主要動向

- 鍛造鋼

- 鋳鉄/鋼

- 機械加工されたビレット

第7章 市場推計・予測:推進力別、2021-2034

- 主要動向

- ディーゼル

- 天然ガス

第8章 市場推計・予測:車両別、2021-2034

- 主要動向

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第9章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Aichi Steel

- Atlas Industries

- Bharat Forge

- Bharat gears

- Bryan Tools &Engineering

- China Zhongwang Holdings

- CIE Automotive

- Crower Cams &Equipment Company

- Indian Crankshaft Manufacturing Company(ICM)

- Kellogg Crankshaft Company

- MAHLE

- Metalurgica Riosulense S/A

- Molnar Technologies

- Nippon Steel

- NSI Crankshaft

- Rheinmetall

- Teksid

- thyssenkrupp

- Tianrun Crankshaft

- ZF Friedrichshafen

The Global Commercial Vehicle Crankshaft Market was valued at USD 2.3 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 4.1 billion by 2034, driven by rising commercial vehicle production and the rapid expansion of global transportation and logistics sectors. As industries worldwide race toward zero-emission targets, the need for more efficient, cleaner vehicle technologies is creating significant momentum across the crankshaft industry. The growing demand for hybrid, electric, and transitional powertrains is reshaping material requirements and performance expectations, pushing manufacturers to innovate lighter, more durable crankshaft solutions. Fleet operators are increasingly investing in next-generation commercial vehicles that bridge traditional internal combustion systems with electrified platforms, boosting the need for high-performance components that deliver both efficiency and reliability. Evolving supply chain dynamics, stricter emissions regulations, and a heightened focus on fuel economy are compelling OEMs and suppliers to reimagine traditional crankshaft designs. Companies are now channeling resources into smarter predictive maintenance technologies, lightweight alloys, and precision manufacturing techniques to meet the rising standards of global fleets. The growing adoption of vehicle-to-grid (V2G) systems, particularly in heavy-duty segments like logistics trucks and buses, further highlights the ongoing need for advanced crankshaft designs that support sustainability while maximizing engine performance.

Increased integration of commercial fleets into smart grid systems is also influencing crankshaft design requirements. Vehicles participating in V2G networks still depend heavily on internal combustion or hybrid engines during this transitional phase, making it crucial for crankshafts to support lower emissions and enhanced fuel efficiency. This trend ties directly into the broader automotive shift toward blending legacy systems with future-forward mobility solutions. Across the value chain, OEMs and component manufacturers are prioritizing the development of lightweight, high-strength crankshafts with better heat resistance and vibration control. At the same time, regulatory incentives across North America, Europe, and Asia targeting emissions reduction are accelerating investments in high-performance crankshaft technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $4.1 Billion |

| CAGR | 5.9% |

In 2024, the cross-plane crankshaft segment dominated with a 59.4% market share, largely because of its superior vibration damping, torque consistency, and dynamic balance. These features are vital for long-haul trucks, industrial buses, and other heavy-duty vehicles that operate under extreme load conditions across diverse terrains. Cross-plane crankshafts also enhance compatibility with large displacement and hybrid engines, ensuring smooth torque delivery critical for optimal fuel efficiency and drivability.

From a sales channel standpoint, OEMs accounted for a commanding 69.4% share in 2024 and are projected to grow at a CAGR of 6.8% through 2034. OEMs are increasingly collaborating with crankshaft manufacturers to co-develop application-specific forged designs that prioritize strength, fatigue resistance, and thermal efficiency.

China Commercial Vehicle Crankshaft Market led globally with a 54.2% share, generating USD 486.7 million in 2024. The country's dominance stems from its massive commercial vehicle production scale and vertically integrated supply chain. Cities like Chongqing, Jinan, and Guangzhou have emerged as key manufacturing hubs, supported by government initiatives, skilled labor pools, and strong OEM partnerships. Investments in automated forging lines, robotic machining, and stringent quality control are reinforcing China's leadership position.

Key players in the global market include Bharat Forge, thyssenkrupp, MAHLE, Rheinmetall, Kellogg Crankshaft Company, Crower Cams & Equipment, NSI Crankshaft, ZF Friedrichshafen, Nippon Steel, and Tianrun Industrial Technology. Industry leaders are prioritizing R&D for high-strength, low-weight materials, enhancing CNC automation, forging deeper OEM collaborations, and advancing digital integration to track maintenance and optimize emissions performance, keeping pace with the evolving landscape of commercial mobility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturers

- 3.2.2 Raw material suppliers

- 3.2.3 Automotive OEM

- 3.2.4 Distribution channel

- 3.2.5 End-use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Pricing analysis

- 3.9.1 Propulsion

- 3.9.2 Region

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising demand for commercial vehicles

- 3.10.1.2 Expansion of transportation and logistics sector

- 3.10.1.3 Adoption of lightweight and high-strength materials

- 3.10.1.4 Ongoing technological advancements in commercial vehicle crankshaft

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High manufacturing cost

- 3.10.2.2 Supply chain disruption

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Crankshaft, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Flat plane

- 5.3 Cross plane

- 5.4 Modular

Chapter 6 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Forged steel

- 6.3 Cast iron/steel

- 6.4 Machined billet

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Diesel

- 7.3 Natural gas

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Light Commercial Vehicles (LCV)

- 8.3 Medium Commercial Vehicles (MCV)

- 8.4 Heavy Commercial Vehicles (HCV)

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Aichi Steel

- 11.2 Atlas Industries

- 11.3 Bharat Forge

- 11.4 Bharat gears

- 11.5 Bryan Tools & Engineering

- 11.6 China Zhongwang Holdings

- 11.7 CIE Automotive

- 11.8 Crower Cams & Equipment Company

- 11.9 Indian Crankshaft Manufacturing Company (ICM)

- 11.10 Kellogg Crankshaft Company

- 11.11 MAHLE

- 11.12 Metalurgica Riosulense S/A

- 11.13 Molnar Technologies

- 11.14 Nippon Steel

- 11.15 NSI Crankshaft

- 11.16 Rheinmetall

- 11.17 Teksid

- 11.18 thyssenkrupp

- 11.19 Tianrun Crankshaft

- 11.20 ZF Friedrichshafen