|

|

市場調査レポート

商品コード

1740933

航空宇宙用鍛造材料の市場機会、成長促進要因、産業動向分析、2025~2034年予測Aerospace Forging Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 航空宇宙用鍛造材料の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月25日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

航空宇宙用鍛造材料の世界市場は、2024年には128億米ドルとなり、CAGR 5.8%で成長し、2034年には222億米ドルに達すると予測されています。

この成長は主に、材料性能と耐久性に対する業界の注目度の高まりによるものです。航空宇宙部品は、高圧、高熱、大きな機械的応力といった過酷な条件下で使用されるため、卓越した耐疲労性、機械的強度、長寿命を示す材料が要求されます。その結果、重要な航空宇宙機能における信頼性と構造的完全性により、鍛造材料が広く採用されるようになっています。鋳造部品や機械加工部品とは異なり、鍛造部品は欠陥が発生しにくく、冶金学的特性も向上しているため、航空宇宙分野におけるリスクの高い用途に最適です。

航空機産業が燃費向上と二酸化炭素排出量削減のため、より軽量で効率的な航空機に傾倒しているため、需要も増加しています。航空機の軽量化は燃料消費の低減に直接貢献し、世界の持続可能性の目標に合致します。このシフトは、航空宇宙鍛造における先端金属合金の採用を増加させ、特に高い強度対重量比で知られる合金の採用を増加させています。チタンやアルミニウムのような金属は、強度や性能を損なうことなく軽量化ソリューションを提供する能力のおかげで、主要な選択肢になりつつあります。これらの動向は、航空製造における材料の革新と効率化への幅広いシフトを浮き彫りにしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 128億米ドル |

| 予測金額 | 222億米ドル |

| CAGR | 5.8% |

2024年、航空宇宙用鍛造材料市場は材料別にアルミニウム合金、チタン合金、スチール合金、マグネシウム合金、ニッケル基合金、その他に区分されました。チタン合金は、強度、耐食性、軽量性などの優れた特性を兼ね備えているため、市場の33.2%を占め、最大のシェアを占めています。過酷な環境にも耐えられることから、特に航空宇宙構造物やエンジンシステムに適しています。アルミニウム合金は、特に機体構造において、そのコスト効率と成形のしやすさから広く支持されています。鋼合金はより重いが、強度と耐疲労性が重要な高負荷領域では依然として不可欠です。

鍛造技術に基づき、2024年の市場は閉塞型鍛造、ロール鍛造、開放型鍛造、精密鍛造、その他に分類されました。閉塞型鍛造は、その精度、寸法安定性、複雑な航空宇宙部品の製造における効率性により、45.4%の市場シェアでセグメントをリードしました。この方法は、一貫した再現性で高強度部品を生産する能力で特に評価されています。開放型鍛造は、特に高い機械的完全性が要求される大型の重荷重部品を生産するための重要なセグメントとして続いた。ロール鍛造は、その制御されたグレインフローにより、一般的に長くて平らな部品の製造に使用されます。精密鍛造は、原材料の無駄を省き、機械加工の必要性を最小限に抑えることができるため、メーカーの間で支持を集め続けています。

用途別では、2024年の市場はエンジン部品、機体部品、トランスミッションとローター部品、着陸装置部品、制御面、その他に区分されました。機体部品は、機体フレーム、スパー、隔壁などの構造部品に鍛造材料が広く使用されていることが要因で、32.5%と最大のシェアを占めています。エンジン部品も、高応力、高温耐性の部品に対する需要を考えると、かなりの部分を占めています。鍛造部品は、過酷な使用条件下での耐久性と性能を確保するために不可欠です。反復的な衝撃と応力に耐えなければならない着陸装置部品は、長期的な信頼性を確保するために、一般的に鋼とチタンの鍛造に依存しています。

米国は世界の航空宇宙用鍛造材料市場で注目すべきシェアを獲得し、2024年には17.8%を占めました。これは23億米ドルに相当し、2034年には41億米ドルに増加すると予測されています。米国の航空宇宙部門は、民間航空と航空機製造を含み、同国経済において重要な役割を果たしています。60万人以上の専門家を擁し、国のGDPに大きく貢献しているこの産業は、継続的な技術革新と国際競争力を支えています。

競合情勢を形成している主要企業には、アルコニック・コーポレーション、プレシジョン・キャストパーツ・コーポレーション、アレゲニー・テクノロジーズ・インコーポレイテッド(ATI)、バラット・フォージ・リミテッド、神戸製鋼所、VSMPO-AVISMAコーポレーション、新日本製鐵などがあります。これらのプレーヤーは、技術的進歩、世界展開、戦略的パートナーシップなど多様な戦略を採用し、市場での地位を維持・強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 世界の航空機生産の増加

- 軽量・高強度材料の需要増加

- 商業航空と航空旅客交通の増加

- 軍艦の近代化

- 新興市場における格安航空会社の拡大

- 鍛造工程における技術的進歩

- 業界の潜在的リスク&課題

- 鍛造施設の資本コストと運用コストが高め

- 原材料価格の変動(チタン、ニッケルなど)

- 厳格な航空宇宙品質および認証基準

- 促進要因

- トランプ政権の関税の影響- 構造化された概要

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:材質別、2021-2034

- 主要動向

- チタン合金

- アルミニウム合金

- 鋼合金

- ニッケル基合金

- マグネシウム合金

- その他

第6章 市場推計・予測:鍛造技術別、2021-2034

- 主要動向

- 型鍛造

- 自由鍛造

- ロール鍛造

- 精密鍛造

- その他

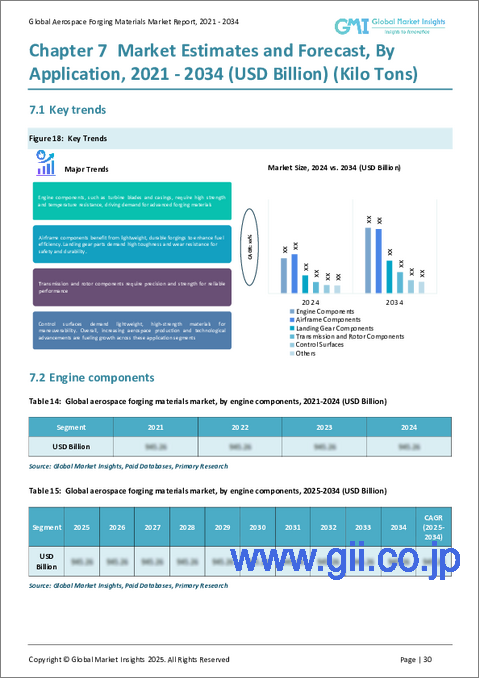

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- エンジン部品

- 機体部品

- 着陸装置の部品

- トランスミッションとローター部品

- 操縦翼面

- その他

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Alcoa

- Allegheny Technologies Incorporated(ATI)

- Arconic Corporation

- Barry A. Dorfman &Co.

- Bergsen Metals

- Bharat Forge Limited

- Forgital Group

- KOBE STEEL、LTD.

- Nippon Steel Corporation

- Plymouth Tube Company

- Precision Castparts Corp.

- Reliance Steel &Aluminum Co.

- Rickard Specialty Metals Supply &Engineering

- VSMPO-AVISMA Corporation

- Weldaloy Specialty Forgings Company

The Global Aerospace Forging Materials Market was valued at USD 12.8 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 22.2 billion by 2034. This growth is primarily influenced by the industry's increasing focus on material performance and durability. Aerospace components operate under extreme conditions such as high pressure, intense heat, and significant mechanical stress, demanding materials that exhibit exceptional fatigue resistance, mechanical strength, and longevity. As a result, forged materials are gaining widespread adoption due to their reliability and structural integrity in critical aerospace functions. Unlike cast or machined parts, forged components are less prone to defects and deliver enhanced metallurgical properties, making them ideal for high-risk applications across the aerospace sector.

Demand is also rising as the industry leans toward lighter, more efficient aircraft to improve fuel economy and reduce carbon emissions. Reducing aircraft weight directly contributes to lower fuel consumption and aligns with global sustainability objectives. This shift has increased the adoption of advanced metal alloys in aerospace forging, particularly those known for their high strength-to-weight ratios. Metals like titanium and aluminum are becoming the go-to options, thanks to their ability to deliver lightweight solutions without compromising strength or performance. These trends highlight the broader shift toward material innovation and efficiency in aviation manufacturing.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.8 Billion |

| Forecast Value | $22.2 Billion |

| CAGR | 5.8% |

In 2024, the aerospace forging materials market was segmented by material into aluminum alloys, titanium alloys, steel alloys, magnesium alloys, nickel-based alloys, and others. Titanium alloys held the largest share, accounting for 33.2% of the market, owing to their excellent combination of strength, corrosion resistance, and lightweight characteristics. Their ability to endure extreme environments makes them especially suitable for aerospace structures and engine systems. Aluminum alloys are widely favored for their cost-efficiency and ease of formability, especially in airframe structures. Although heavier, steel alloys remain essential in high-load areas where strength and fatigue resistance are critical.

Based on forging techniques, the market in 2024 was classified into closed die forging, roll forging, open die forging, precision forging, and others. Closed die forging led the segment with a 45.4% market share due to its precision, dimensional stability, and efficiency in producing complex aerospace components. This method is especially valued for its ability to produce high-strength parts with consistent repeatability. Open die forging followed as a significant segment, especially for producing large, heavy-duty components that require high mechanical integrity. Roll forging, with its controlled grain flow, is typically used for manufacturing long, flat parts. Precision forging continues to gain traction among manufacturers for its ability to reduce raw material waste and minimize machining requirements.

In terms of applications, the market was segmented in 2024 into engine components, airframe components, transmission and rotor components, landing gear components, control surfaces, and others. Airframe components accounted for the largest share at 32.5%, driven by the widespread use of forged materials in structural parts such as fuselage frames, spars, and bulkheads. Engine components also represent a significant portion, given the demand for high-stress, high-temperature-resistant parts. Forged components are vital in ensuring durability and performance under harsh operating conditions. Landing gear components, which must endure repetitive impact and stress, typically rely on steel and titanium forging to ensure long-term reliability.

The United States captured a notable share of the global aerospace forging materials market, holding 17.8% in 2024. This equated to USD 2.3 billion and is projected to rise to USD 4.1 billion by 2034. The U.S. aerospace sector plays a vital role in the country's economy, encompassing commercial aviation and aircraft manufacturing. With a workforce of over 600,000 professionals and substantial contributions to the national GDP, the industry supports continuous innovation and global competitiveness.

Leading companies shaping the competitive landscape include Arconic Corporation, Precision Castparts Corp., Allegheny Technologies Incorporated (ATI), Bharat Forge Limited, KOBE STEEL, LTD., VSMPO-AVISMA Corporation, and Nippon Steel Corporation. These players employ diverse strategies, including technological advancements, global expansions, and strategic partnerships, to maintain and strengthen their market positions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing global aircraft production

- 3.6.1.2 Rising demand for lightweight, high-strength materials

- 3.6.1.3 Growth in commercial aviation and air passenger traffic

- 3.6.1.4 Modernization of military fleets

- 3.6.1.5 Expansion of low-cost carriers in emerging markets

- 3.6.1.6 Technological advancements in forging processes

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High capital and operational cost of forging facilities

- 3.6.2.2 Volatility in raw material prices (e.g., titanium, nickel)

- 3.6.2.3 Stringent aerospace quality and certification standards

- 3.6.1 Growth drivers

- 3.7 Impact of trump administration tariffs – structured overview

- 3.7.1 Impact on trade

- 3.7.1.1 Trade volume disruptions

- 3.7.1.2 Retaliatory measures

- 3.7.2 Impact on the industry

- 3.7.2.1 Supply-side impact (raw materials)

- 3.7.2.1.1 Price volatility in key materials

- 3.7.2.1.2 Supply chain restructuring

- 3.7.2.1.3 Production cost implications

- 3.7.2.2 Demand-side impact (selling price)

- 3.7.2.2.1 Price transmission to end markets

- 3.7.2.2.2 Market share dynamics

- 3.7.2.2.3 Consumer response patterns

- 3.7.2.1 Supply-side impact (raw materials)

- 3.7.3 Key companies impacted

- 3.7.4 Strategic industry responses

- 3.7.4.1 Supply chain reconfiguration

- 3.7.4.2 Pricing and product strategies

- 3.7.4.3 Policy engagement

- 3.7.4.4 Outlook and future considerations

- 3.7.1 Impact on trade

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Material Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Titanium alloys

- 5.3 Aluminum alloys

- 5.4 Steel alloys

- 5.5 Nickel-based alloys

- 5.6 Magnesium alloys

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Forging Technique, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Closed die forging

- 6.3 Open die forging

- 6.4 Roll forging

- 6.5 Precision forging

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Engine components

- 7.3 Airframe components

- 7.4 Landing gear components

- 7.5 Transmission and rotor components

- 7.6 Control surfaces

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alcoa

- 9.2 Allegheny Technologies Incorporated (ATI)

- 9.3 Arconic Corporation

- 9.4 Barry A. Dorfman & Co.

- 9.5 Bergsen Metals

- 9.6 Bharat Forge Limited

- 9.7 Forgital Group

- 9.8 KOBE STEEL, LTD.

- 9.9 Nippon Steel Corporation

- 9.10 Plymouth Tube Company

- 9.11 Precision Castparts Corp.

- 9.12 Reliance Steel & Aluminum Co.

- 9.13 Rickard Specialty Metals Supply & Engineering

- 9.14 VSMPO-AVISMA Corporation

- 9.15 Weldaloy Specialty Forgings Company