|

市場調査レポート

商品コード

1740932

血管造影装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Angiography Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 血管造影装置の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月15日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

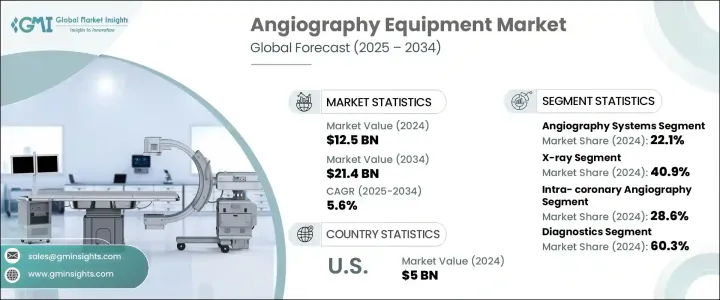

世界の血管造影装置市場は、2024年には125億米ドルと評価され、心血管疾患の負担の増加や、頻繁な診断と介入治療を必要とする世界人口の高齢化の進展に牽引され、CAGR 5.6%で成長し、2034年には214億米ドルに達すると推定されています。

高血圧、糖尿病、肥満のような慢性疾患の蔓延は、血管画像診断を必要とする患者数を著しく増加させています。世界の医療情勢が早期発見と低侵襲治療にシフトするにつれ、先進的な血管造影装置に対する需要は急増すると予想されます。病院や診断センターは、臨床結果を向上させ、処置時間を短縮し、患者の放射線被曝を最小限に抑えるために、最先端の技術を急速に導入しています。

3Dイメージング、フラットパネル検出器、AI強化イメージング・ソフトウェアなどの技術的ブレークスルーは、血管障害の診断・治療方法に革命をもたらしています。ヘルスケア投資の拡大、有利な償還シナリオ、心臓の予防医療に対する意識の高まりは、世界中の血管造影装置メーカーに新たな機会をもたらしています。新興国ではヘルスケアのインフラが大幅に改善され、高度な診断ツールへのアクセスが拡大しています。政府や民間団体が非感染性疾患への取り組みを強化する中、血管造影システムのような高精度画像ソリューションの採用は今後10年間で力強い成長が見込まれています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 125億米ドル |

| 予測金額 | 214億米ドル |

| CAGR | 5.6% |

全製品タイプの中で、血管造影システムは2024年に22.1%のシェアを占めました。これらのシステムは、診断とインターベンションの両方において、詳細な血管撮影のための好ましい選択肢であり続けています。リアルタイムで正確かつダイナミックな画像診断が可能なため、複雑な心臓血管、神経血管、腫瘍の症例管理には欠かせないです。技術革新への継続的な投資により、放射線量の低減や画像の鮮明度の向上などの改善がもたらされ、病院がより安全で効率的な患者転帰を実現できるようになりました。使いやすさの向上とユーザー・インターフェース・デザインの進歩が、さまざまな医療現場での採用をさらに後押ししています。

手技別では、冠動脈内血管造影の2024年のシェアは28.6%でした。心血管疾患が増加傾向を維持する中、冠動脈内血管造影は緊急介入と選択的処置の両方に不可欠であり続けています。分画血流予備量(FFR)や光干渉断層計(OCT)のような技術革新は、純粋な解剖学的評価から機能的評価へと焦点を移し、インターベンション中の意思決定を向上させています。冠動脈疾患は世界の健康上の負担を増大させており、冠動脈内血管造影の役割は、特にハイブリッド手術室や高度なカテラボに統合されることにより、拡大するものと思われます。

米国の血管造影装置市場は、臨床需要の高まりと強力なヘルスケアシステムに後押しされ、2024年には50億米ドルに達します。肥満、高血圧、高齢化率の増加が、早期診断と予防的スクリーニングを推進する国家的イニシアチブを後押ししています。保険適用範囲の拡大と統合ヘルスケアネットワークの台頭により、血管造影評価は外来センターや地方でも利用しやすくなっています。さらに、デジタルプラットフォームの採用により、ルーチンの心血管系評価への血管造影のシームレスな統合が可能になり、スピードと精度が向上しました。

世界の血管造影装置市場で事業を展開している主要企業には、Medtronic、Canon Medical System、GEヘルスケア、Cordis、Philips、Merit Medical、東芝メディカルシステム、Angiodynamics、Siemens Healthineers、Microport Scientific、Cardinal Health、B. Braun、Abbott、Boston Scientific、島津製作所などがあります。大手企業は、AIを統合した低放射線システムを発売するための研究開発に多額の投資を行い、世界なパートナーシップを拡大して市場へのリーチを強化する一方、臨床ニーズや規制が地域化された新興市場向けに製品を調整しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 心血管疾患の有病率の増加

- 高齢化人口の増加

- 画像技術の技術的進歩

- 心臓疾患の早期発見に向けた公衆衛生の取り組みの拡大

- 業界の潜在的リスク&課題

- 機器の調達とメンテナンスにかかる高コスト

- 放射線被曝に関連するリスク

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 技術的情勢

- 将来の市場動向

- ギャップ分析

- 特許分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021 –2034

- 主要動向

- 血管造影システム

- カテーテル

- ガイドワイヤー

- 風船

- 造影剤

- 血管閉鎖デバイス

- 血管造影アクセサリー

第6章 市場推計・予測:技術別、2021 –2034

- 主要動向

- X線

- 画像増強装置

- フラットパネル検出器

- MRA

- CT

第7章 市場推計・予測:手順別、2021 –2034

- 主要動向

- 冠動脈造影検査

- 血管内血管造影

- 神経血管造影検査

- 腫瘍血管造影

- その他の血管造影検査

第8章 市場推計・予測:用途別、2021 –2034

- 主要動向

- 診断

- 治療薬

第9章 市場推計・予測:最終用途別、2021 –2034

- 主要動向

- 病院と診療所

- 診断・画像診断センター

- その他の用途

第10章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Abbott

- Angiodynamics

- B. BRAUN

- Boston Scientific

- Canon Medical System

- Cardinal Health

- Cordis

- GE Healthcare

- Koninklijke Philips

- Medtronic

- Merit Medical

- Microport Scientific

- Shimadzu

- Siemens Healthineers

- Toshiba Medical System

The Global Angiography Equipment Market was valued at USD 12.5 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 21.4 billion by 2034, driven by the rising burden of cardiovascular diseases and an increasingly aging global population that demands frequent diagnostic and interventional care. The escalating prevalence of chronic conditions like hypertension, diabetes, and obesity is significantly increasing the number of patients who require vascular imaging procedures. As the global healthcare landscape shifts toward early detection and minimally invasive treatments, the demand for advanced angiography equipment is expected to soar. Hospitals and diagnostic centers are rapidly adopting cutting-edge technologies to enhance clinical outcomes, reduce procedure time, and minimize patient exposure to radiation.

Technological breakthroughs such as 3D imaging, flat-panel detectors, and AI-enhanced imaging software are revolutionizing the way vascular disorders are diagnosed and treated. Growing healthcare investments, favorable reimbursement scenarios, and rising awareness about preventative cardiac care are creating new opportunities for angiography equipment manufacturers worldwide. Emerging economies are witnessing major improvements in healthcare infrastructure, fueling broader access to advanced diagnostic tools. As governments and private organizations ramp up efforts to tackle non-communicable diseases, the adoption of high-precision imaging solutions like angiography systems is expected to experience robust growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.5 Billion |

| Forecast Value | $21.4 Billion |

| CAGR | 5.6% |

Among all product types, the angiography systems segment accounted for a 22.1% share in 2024. These systems continue to be the preferred choice for detailed vessel imaging in both diagnostic and interventional procedures. Their ability to deliver real-time, accurate, and dynamic imaging has made them crucial in managing complex cardiovascular, neurovascular, and oncological cases. Continuous investments in innovation have led to improvements such as reduced radiation doses and enhanced imaging clarity, helping hospitals deliver safer, more efficient patient outcomes. Enhanced ease of use and advancements in user interface design are further driving their adoption across various care settings.

Based on the procedure, the intra-coronary angiography segment generated a 28.6% share in 2024. As cardiovascular diseases maintain a rising trend, intra-coronary angiography remains vital for both emergency interventions and elective procedures. Innovations like fractional flow reserve (FFR) and optical coherence tomography (OCT) have shifted the focus from purely anatomical assessments to functional evaluations, improving decision-making during interventions. With coronary artery disease presenting a growing global health burden, the role of intra-coronary angiography is set to expand, especially with its integration into hybrid ORs and advanced cath labs.

The U.S. Angiography Equipment Market reached USD 5 billion in 2024, fueled by rising clinical demand and a strong healthcare system. The growing rates of obesity, hypertension, and an aging population have driven national initiatives promoting early diagnostics and preventative screenings. Expanded insurance coverage and the rise of integrated healthcare networks have made angiographic evaluations more accessible across outpatient centers and rural areas. Additionally, the adoption of digital platforms has enabled seamless integration of angiography into routine cardiovascular assessments, boosting speed and accuracy.

Leading companies operating in the Global Angiography Equipment Market include Medtronic, Canon Medical System, GE Healthcare, Cordis, Philips, Merit Medical, Toshiba Medical System, Angiodynamics, Siemens Healthineers, Microport Scientific, Cardinal Health, B. Braun, Abbott, Boston Scientific, and Shimadzu Corporation. Major players are heavily investing in R&D to launch AI-integrated, low-radiation systems and expanding global partnerships to strengthen market reach while tailoring products for emerging markets with localized clinical needs and regulations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of cardiovascular diseases

- 3.2.1.2 Rise in aging population

- 3.2.1.3 Technological advancements in imaging techniques

- 3.2.1.4 Growing public health initiatives for early detection of cardiac diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated to equipment procurement and maintenance

- 3.2.2.2 Risk related to radiation exposure

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Patent analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Angiography systems

- 5.3 Catheters

- 5.4 Guidewire

- 5.5 Balloons

- 5.6 Contrast media

- 5.7 Vascular closure devices

- 5.8 Angiography accessories

Chapter 6 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 X-ray

- 6.2.1 Image intensifiers

- 6.2.2 Flat-panel detectors

- 6.3 MRA

- 6.4 CT

Chapter 7 Market Estimates and Forecast, By Procedure, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Coronary angiography

- 7.3 Endovascular angiography

- 7.4 Neuroangiography

- 7.5 Onco-angiography

- 7.6 Other angiography procedures

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Diagnostics

- 8.3 Therapeutics

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals and clinics

- 9.3 Diagnostic and imaging centers

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Abbott

- 11.2 Angiodynamics

- 11.3 B. BRAUN

- 11.4 Boston Scientific

- 11.5 Canon Medical System

- 11.6 Cardinal Health

- 11.7 Cordis

- 11.8 GE Healthcare

- 11.9 Koninklijke Philips

- 11.10 Medtronic

- 11.11 Merit Medical

- 11.12 Microport Scientific

- 11.13 Shimadzu

- 11.14 Siemens Healthineers

- 11.15 Toshiba Medical System