|

市場調査レポート

商品コード

1740931

サイドローダー式ごみ収集車市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Side Loader Refuse Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| サイドローダー式ごみ収集車市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月30日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

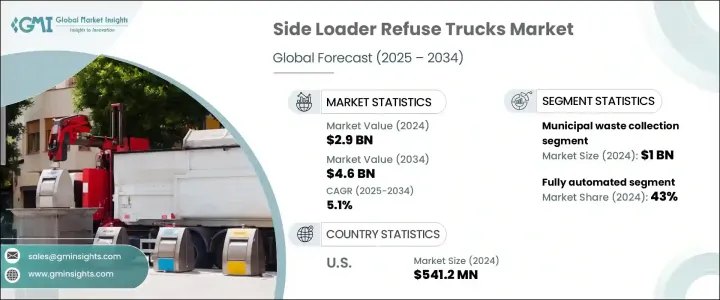

世界のサイドローダー式ごみ収集車市場は、2024年には29億米ドルとなり、CAGR 5.1%で成長し、2034年には46億米ドルに達すると推定されています。

世界中の都市が拡大を続ける中、効率的でスペースに配慮した廃棄物収集車の需要が急増しています。都市開発によって人口密度が高まり、固形廃棄物の量が増えるのは当然のことで、狭いスペースでの廃棄物収集に対応できるシステムが急務となっています。サイドローダー式ごみ収集車は、狭い道路や交通量の多い道路でも小回りが利くため、都市部での最適なソリューションとなっています。また、標準化されたゴミ箱との互換性もあるため、収集プロセスの合理化を目指す自治体にとっても好ましい選択肢となっています。都市の中心部は、よりクリーンで効率的な廃棄物管理を実践する方向に向かっており、これがサイドローダー・トラックの採用を大幅に加速させています。

政府の規制もまた、これらの車両の採用拡大において重要な役割を果たしています。より厳しい環境・安全基準が、地方自治体や民間企業に最新の低排出技術への投資を促しています。電気システムやハイブリッドシステムを動力源とするサイドローダーは、都市が大気質の改善と二酸化炭素排出量の削減を目指していることから、人気を集めています。これらの車両は、環境目標の達成に役立つだけでなく、燃料消費量の削減やメンテナンス時間の短縮によって運転性能も向上させる。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 29億米ドル |

| 予測金額 | 46億米ドル |

| CAGR | 5.1% |

用途別に見ると、市場は産業廃棄物、一般廃棄物、商業廃棄物、建設・解体廃棄物に分けられます。2024年の市場規模は約10億米ドルで、市場シェアの45%以上を占める都市廃棄物回収が優勢です。急速な都市化に伴い、都市部で発生する廃棄物は増加の一途をたどっており、この増加は自治体の収集サービスに対する需要の高まりに反映されています。廃棄物量が増加するにつれて、自治体は衛生システムに対する圧力の高まりに対処するためにサイドローダー・トラックに目を向けています。

これらのトラックの自動設計は、人件費の削減を目指す地方自治体にとって特に価値があることが証明されています。自動化されたアームとビン・リフティング機構を備えたサイドローダーは、必要な運転者の数を減らし、コスト効率と効率を高めています。これらのトラックは、最小限の人的介入で一貫した中断のない廃棄物収集を可能にし、より良い労働力管理と生産性向上をもたらします。都市政府は、廃棄物管理システムの有効性を改善するため、しばしば公的資金や助成金によって支援されながら、このような技術を採用しつつあります。

積み込み機構に関しては、市場は完全自動化システム、半自動化システム、手動システムに区分されます。全自動サイドローダー・トラックは2024年に市場をリードし、全シェアの約43%を占めています。これらのトラックは、ビンの持ち上げ、積み込み、空っぽにすることを含むすべての中核機能を、たった一人の運転者で実行することができます。この自動化は労働力の削減に役立つだけでなく、収集プロセスをスピードアップし、ダウンタイムを最小化し、精度を高めます。技術の進歩に伴い、こうした完全自動化システムは信頼性が高まり、大都市環境では不可欠なものとなっています。

燃料タイプもまた重要なセグメンテーションであり、ディーゼル、電気、CNG、ハイブリッド、その他の燃料タイプが混在しています。ディーゼルエンジン搭載トラックは2024年の市場をリードしました。代替燃料の人気が高まっているにもかかわらず、ディーゼルは多くの自治体や民間事業者にとって最も実用的で費用対効果の高い選択肢であり続けています。ディーゼル・トラックは、耐久性があり、メンテナンスが容易で、給油インフラが確立していることで知られています。長距離路線や大型運転では、ディーゼルは電気やCNGを動力とする代替品と比較して、比類のない信頼性と低い初期費用を提供し続けています。

エンドユーザーの観点から、市場は自治体サービス、専門廃棄物処理業者、非公開廃棄物管理会社、その他に区分されます。2024年は自治体サービスが主導権を握りました。都市部、特に人口密度の高い地域では、地方自治体が廃棄物収集の大半を扱っています。サイドローダー・トラックは、そのコンパクトな設計と自動化機能により、こうした地域で効率的にサービスを提供しています。政府補助金と予算配分を利用できるため、地方自治体は、環境目標をサポートする最新かつコスト効率の高い廃棄物収集技術に投資するのに有利な立場にあります。

地域別では、北米が2024年には35%以上を占め、大きなシェアを占めています。米国だけの市場規模は約5億4,120万米ドルです。都市人口が多い同国では、州レベルの厳しい規制も相まって、自動化されたクリーンな廃棄物収集技術が必要不可欠となっています。廃棄物収集当局は、全体的な運営コストを削減しながら排出規制を遵守するため、電気モデルやハイブリッドモデルへの投資を増やしています。

この分野の主要メーカーは現在、持続可能性に重点を置き、スマートオートメーション、電気ドライブトレイン、診断機能を備えたモデルを提供することで競争しています。低排出ガス車やゼロ・エミッション車を提供できる企業は、特に北米と欧州のグリーン調達政策を持つ地域で、より多くのビジネスチャンスを見出しています。競争優位性は、性能、燃料効率、安全性、環境コンプライアンスをコスト効率の良いパッケージでバランスさせた車両を提供することにあります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料および部品サプライヤー

- トラックおよび機器メーカー

- テクノロジーおよびテレマティクスプロバイダー

- 最終用途

- 利益率分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 特許分析

- 価格分析

- 地域

- 推進

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 都市化と人口増加

- クリーンで効率的な廃棄物収集のための規制の推進

- 民間廃棄物管理会社の成長

- ゴミ収集車の技術的進歩

- 業界の潜在的リスク&課題

- 初期コストが高め

- 高いメンテナンス費用と修理費用

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:ローディング機構別、2021-2034

- 主要動向

- 完全自動化

- 半自動

- マニュアル

第6章 市場推計・予測:容量別、2021-2034

- 主要動向

- 10,000ポンド未満

- 10,000~20,000ポンド

- 2万~3万ポンド

- 3万ポンド以上

第7章 市場推計・予測:燃料別、2021-2034

- 主要動向

- ディーゼル

- 電気

- CNG

- ハイブリッド

- その他

第8章 市場推計・予測:用途別、2021-2034

- 主要動向

- 自治体の廃棄物収集

- 産業廃棄物収集

- 商業廃棄物収集

- 建設廃棄物および解体廃棄物

第9章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 市政サービス

- 民間の廃棄物管理会社

- 専門廃棄物処理業者

- その他

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Amrep

- Autocar

- Bridgeport Manufacturing

- Bucher Municipal

- BYD

- Curbtender

- Dennis Eagle

- FAUN Zoeller(UK)

- Foton Motor

- Freightliner(Daimler)

- Fujian Longma Environmental Sanitation Equipment

- Heil

- Isuzu

- Labrie Trucks

- Mack Trucks

- McNeilus Truck and Manufacturing

- New Way Refuse Trucks

- NTM

- Pak-Mor

- Peterbilt Motors Company

The Global Side Loader Refuse Trucks Market was valued at USD 2.9 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 4.6 billion by 2034. As cities around the world continue to expand, the demand for efficient and space-conscious waste collection vehicles has surged. Urban development naturally brings with it higher population densities and increased volumes of solid waste, creating an urgent need for systems that can handle waste collection in tight spaces. Side loader refuse trucks have become the go-to solution in urban areas, thanks to their ability to maneuver through narrow roads and busy streets. Their compatibility with standardized waste bins also makes them a preferred option for municipalities aiming to streamline collection processes. Urban centers are moving towards cleaner and more efficient waste management practices, which has significantly accelerated the adoption of side loader trucks.

Government regulations are also playing a critical role in the growing adoption of these vehicles. Stricter environmental and safety standards are pushing local authorities and private firms to invest in modern, low-emission technologies. Side loaders powered by electric and hybrid systems are gaining traction as cities aim to improve air quality and reduce carbon emissions. These vehicles not only help meet environmental goals but also improve operational performance by consuming less fuel and reducing maintenance time.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.9 Billion |

| Forecast Value | $4.6 Billion |

| CAGR | 5.1% |

In terms of application, the market is divided into industrial waste, municipal waste, commercial waste, and construction and demolition waste. Municipal waste collection dominated in 2024, with a market value of around USD 1 billion, representing over 45% of the market share. With rapid urbanization, waste generated in city areas continues to rise, and this increase is reflected in the higher demand for municipal collection services. As waste volumes grow, municipalities are turning to side loader trucks to handle rising pressure on their sanitation systems.

The automated design of these trucks has proven to be especially valuable for city governments looking to reduce labor costs. With automated arms and bin-lifting mechanisms, side loaders require fewer operators, making them more cost-effective and efficient. These trucks allow consistent and uninterrupted waste collection with minimal human intervention, leading to better workforce management and productivity gains. City governments are increasingly adopting such technologies, often supported by public funding or grants, to improve the effectiveness of their waste management systems.

When it comes to loading mechanisms, the market is segmented into fully automated, semi-automated, and manual systems. Fully automated side loader trucks led the market in 2024, holding around 43% of the total share. These trucks are capable of performing all core functions - including lifting, loading, and emptying bins - with just one operator. This automation not only helps reduce the labor force but also speeds up collection processes, minimizes downtime, and increases accuracy. As technology continues to advance, these fully automated systems are becoming more reliable and essential in large urban settings.

Fuel type is another critical segmentation, with diesel, electric, CNG, hybrid, and other fuel types in the mix. Diesel-powered trucks led the market in 2024. Despite the growing popularity of alternative fuels, diesel remains the most practical and cost-effective choice for many municipalities and private operators. Diesel trucks are known for their durability, easier maintenance, and well-established refueling infrastructure. For long-haul routes and heavy-duty operations, diesel continues to offer unmatched reliability and lower upfront costs compared to electric or CNG-powered alternatives.

In terms of end users, the market is segmented into municipal services, specialized waste handlers, private waste management companies, and others. Municipal services took the lead in 2024. Local governments handle the majority of waste collection in urban areas, especially in densely populated neighborhoods. Side loader trucks serve these regions efficiently due to their compact design and automated capabilities. With access to government subsidies and budget allocations, municipalities are better positioned to invest in updated and cost-efficient waste collection technologies that support their environmental goals.

Geographically, North America held a major share of the market, accounting for over 35% in 2024. The U.S. alone reached a market value of approximately USD 541.2 million. The country's high urban population, combined with strict state-level regulations, has made automated and clean waste collection technologies a necessity. Waste collection authorities are increasingly investing in electric and hybrid models to comply with emission mandates while reducing overall operating costs.

Major manufacturers in this space are now focusing heavily on sustainability, competing by offering models with smart automation, electric drivetrains, and diagnostic features. Companies that can provide low or zero-emission vehicles are finding more opportunities in regions with green procurement policies, especially in North America and Europe. The competitive edge lies in offering vehicles that balance performance, fuel efficiency, safety, and environmental compliance in a cost-effective package.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material and component supplier

- 3.2.2 Truck and equipment manufacturer

- 3.2.3 Technology and telematics providers

- 3.2.4 End use

- 3.3 Profit margin analysis

- 3.4 Impact of trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook & future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Price analysis

- 3.7.1 Region

- 3.7.2 Propulsion

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Urbanization and population growth

- 3.10.1.2 Regulatory push for clean and efficient waste collection

- 3.10.1.3 Growth of private waste management companies

- 3.10.1.4 Technological advancements in refuse trucks

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High initial cost

- 3.10.2.2 High maintenance and repair costs

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Loading Mechanism, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Fully automated

- 5.3 Semi-automated

- 5.4 Manual

Chapter 6 Market Estimates & Forecast, By Capacity, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Less than 10,000 lbs

- 6.3 10,000 to 20,000 lbs

- 6.4 20,000 to 30,000 lbs

- 6.5 More than 30,000 lbs

Chapter 7 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Diesel

- 7.3 Electric

- 7.4 CNG

- 7.5 Hybrid

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Municipal waste collection

- 8.3 Industrial waste collection

- 8.4 Commercial waste collection

- 8.5 Construction and demolition waste

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Municipal services

- 9.3 Private waste management companies

- 9.4 Specialized waste handlers

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Amrep

- 11.2 Autocar

- 11.3 Bridgeport Manufacturing

- 11.4 Bucher Municipal

- 11.5 BYD

- 11.6 Curbtender

- 11.7 Dennis Eagle

- 11.8 FAUN Zoeller (UK)

- 11.9 Foton Motor

- 11.10 Freightliner (Daimler)

- 11.11 Fujian Longma Environmental Sanitation Equipment

- 11.12 Heil

- 11.13 Isuzu

- 11.14 Labrie Trucks

- 11.15 Mack Trucks

- 11.16 McNeilus Truck and Manufacturing

- 11.17 New Way Refuse Trucks

- 11.18 NTM

- 11.19 Pak-Mor

- 11.20 Peterbilt Motors Company