自動車用燃料計の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Automotive Fuel Gauge Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740922

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

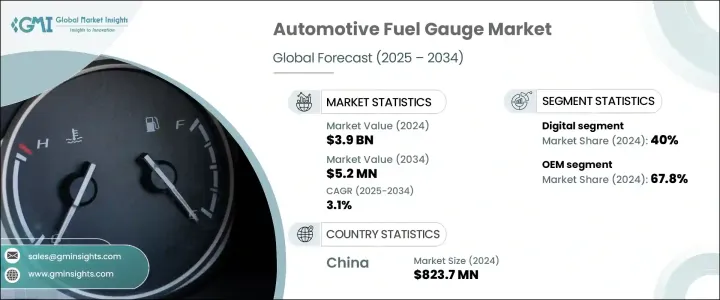

世界の自動車用燃料計市場は、2024年には39億米ドルと評価され、テレマティクスと統合された高度な燃料計システムへの需要を伴う車両とフリートのデジタル化によって、CAGR 3.1%で成長し、2034年には52億米ドルに達すると予測されています。

フリート管理者は、コストの最適化、メンテナンスのスケジュール、ドライバーの行動監視のために、リアルタイムの燃料データに継続的にアクセスする必要があります。テレマティクスを介してリンクされたこれらのスマートゲージは、燃料レベルの即時更新を提供し、燃料の盗難や漏れなどの問題を特定し、給油の必要性のアラートを送信することができます。この統合により、予知保全がサポートされ、運行停止時間が短縮されるため、物流、公共交通機関、共有モビリティ・サービスにおいて、このシステムは極めて重要なものとなります。

センサー設計の技術的進歩により、自動車用燃料計の性能は大幅に向上しました。静電容量式、超音波式、抵抗式を含む最新のセンサーは、さまざまな運転条件下で、より優れた精度、より速い応答時間、より高い耐久性を提供します。これらのセンサーは、バイオ燃料やエタノール混合燃料を含む、さまざまなタンクサイズや燃料タイプに適応します。精度が向上したことで、誤測定が減り、個人用車両とフリート車両の両方の運用に不可欠な信頼性の高い燃料データが保証されます。さらに、センサーの小型化により、コンパクトな車両設計への統合が改善され、全体的な機能性が向上しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 39億米ドル |

| 予測金額 | 52億米ドル |

| CAGR | 3.1% |

自動車用燃料計市場は、アナログ、ハイブリッドディスプレイ、ヘッドアップディスプレイ、デジタルオプションなど技術別に区分されます。2024年の市場シェアはデジタルセグメントが40%で首位に立ち、2034年までCAGR 3.7%で成長する見込みです。この成長の原動力となっているのは、自動車の電動化の進展、スマート・ダッシュボードへの統合需要、燃料やエネルギー使用量の正確でリアルタイムな監視を好む消費者です。デジタル燃料計は、電気自動車やハイブリッド車を含む最新の自動車にとって不可欠であり、バッテリーの航続距離、充電状態、エネルギーの流れに関する詳細な情報を提供します。

販売チャネルでは、OEM分野が2024年に67.8%のシェアを占め、2025年から2034年にかけてCAGR 2.8%で成長すると予想されています。OEM分野は、新しく製造される自動車の標準部品として燃料計が組み込まれているため、依然として支配的です。これらの計器はデジタル計器クラスタや車両診断システムに組み込まれており、最新のエンジン管理技術や排出ガス技術との互換性を確保しています。主要計器メーカーは自動車メーカーと直接協力し、特定の車両アーキテクチャやダッシュボードレイアウトに適合するカスタムソリューションを設計しています。

中国自動車用燃料計市場は2024年に54%のシェアを占め、8億2,370万米ドルを創出しました。中国は垂直統合されたサプライチェーンの恩恵を受けており、現地メーカーはOEMの需要を効率的かつコスト効率よく満たすことができます。この地域における自動車生産台数の増加は、中国の電気自動車(EV)やスマート自動車技術への多額の投資と相まって、燃料計のような高度な自動車部品の需要増加にさらに貢献しています。

自動車用燃料計業界の主要企業は、Aptiv、BorgWarner、Bosch、Continental、Densoなどです。自動車用燃料計市場の企業は、市場での地位を強化するため、自動車メーカーとの戦略的提携に重点を置き、独自の燃料計ソリューションを開発しています。特にセンサーの設計やテレマティクスの統合など、技術的な進歩に多額の投資を行い、精度を高め、リアルタイムのモニタリング機能を提供しています。さらに、各社はアジア太平洋のような新興市場でのプレゼンス拡大に注力し、現地生産能力を活用してコストを削減し、高度な燃料管理システムの需要増に対応しています。自動車の電動化とコネクテッド・テクノロジーの利用拡大に注力することで、これらの企業は急速に進化する自動車市場をリードする地位を確立しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 製造業者

- 原材料サプライヤー

- OEM

- 流通チャネル

- 最終用途

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(顧客へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- コスト内訳分析

- 価格分析

- 地域別

- 推進力別

- 規制情勢

- 影響要因

- 促進要因

- 車両の電動化の進展

- 排出ガス規制と燃費規制の強化

- センサー技術の進歩

- フリートとテレマティクスの統合の成長

- 業界の潜在的リスク&課題

- センサーの校正と精度の問題

- 統合の複雑さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:技術別、2021-2034

- 主要動向

- アナログ

- デジタル

- 液晶

- 有機EL

- ハイブリッドディスプレイ

- ヘッドアップディスプレイ

第6章 市場推計・予測:センサー別、2021-2034

- 主要動向

- 抵抗型

- 静電容量式

- 超音波

- その他

第7章 市場推計・予測:推進力別、2021-2034

- 主要動向

- ICE

- 電気自動車

- バッテリー電気自動車(BEV)

- プラグインハイブリッド電気自動車(PHEV)

- ハイブリッド電気自動車(HEV)

第8章 市場推計・予測:車両別、2021-2034

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第9章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Aptiv

- Auto Meter Products

- AUTOGAUGE

- Continental

- DENSO

- DunkTeam

- Equus Products

- Faria Beede Instruments

- Gee Kay Equipments

- GlowShift Gauges

- Iontra

- KUS USA

- Marshall Instruments

- Minda

- Pricol

- Robert Bosch

- Sierra Instruments

- Stoneridge

- Wonfly

- Yazaki

目次

The Global Automotive Fuel Gauge Market was valued at USD 3.9 billion in 2024 and is estimated to grow at a CAGR of 3.1% to reach USD 5.2 billion by 2034, driven by the vehicles and fleet digitalization, with the demand for advanced fuel gauge systems integrated with telematics. Fleet managers need continuous access to real-time fuel data to optimize costs, schedule maintenance, and monitor driver behavior. These smart gauges, linked through telematics, can provide instant fuel level updates, identify issues such as fuel theft or leaks, and send alerts for refueling needs. This integration supports predictive maintenance and reduces operational downtime, making the systems crucial in logistics, public transportation, and shared mobility services.

Technological advancements in sensor design have greatly improved the performance of automotive fuel gauges. Modern sensors, including capacitive, ultrasonic, and resistive types, offer better accuracy, faster response times, and greater durability under various operating conditions. These sensors adapt to different tank sizes and fuel types, including biofuels and ethanol blends. This increased precision reduces false readings and ensures reliable fuel data, which is critical for both personal and fleet vehicle operations. Additionally, sensor miniaturization has improved integration in compact vehicle designs, enhancing overall functionality.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.9 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 3.1% |

The automotive fuel gauge market is segmented by technology, including analog, hybrid display, head-up display, and digital options. In 2024, the digital segment took the lead with a 40% market share, expected to grow at a 3.7% CAGR through 2034. This growth is fueled by the increasing electrification of vehicles, the demand for smart dashboard integration, and consumers' preference for accurate and real-time monitoring of fuel or energy usage. Digital fuel gauges are essential for modern vehicles, including electric and hybrid models, providing detailed information on battery range, charge status, and energy flow.

In terms of sales channels, the OEM segment held 67.8% share in 2024 and is expected to grow at a CAGR of 2.8% from 2025 to 2034. The OEM sector remains dominant due to the incorporation of fuel gauges as standard components in newly manufactured vehicles. These gauges are integrated into digital instrument clusters and vehicle diagnostic systems, ensuring compatibility with modern engine management and emissions technologies. Key gauge manufacturers collaborate directly with automotive producers to design custom solutions that fit specific vehicle architectures and dashboard layouts.

China Automotive Fuel Gauge Market held 54% share in 2024 and generated USD 823.7 million, driven by passenger and commercial vehicle production, which has bolstered its position in the fuel gauge market. China benefits from a vertically integrated supply chain, enabling local manufacturers to meet OEM demand efficiently and cost-effectively. The growing volume of vehicle production in the region, coupled with China's significant investment in electric vehicles (EVs) and smart automotive technology, has further contributed to the rising demand for advanced automotive components like fuel gauges.

Key players in the automotive fuel gauge industry include Aptiv, BorgWarner, Bosch, Continental, and Denso. To strengthen their market position, companies in the automotive fuel gauge market focus on strategic collaborations with automotive manufacturers to develop tailored fuel gauge solutions. They invest heavily in technological advancements, particularly sensor design and telematics integration, to enhance accuracy and offer real-time monitoring features. Additionally, companies focus on expanding their presence in emerging markets like Asia Pacific, leveraging local manufacturing capabilities to reduce costs and cater to increasing demand for advanced fuel management systems. By focusing on the electrification of vehicles and increasing use of connected technologies, these companies are positioning themselves to lead in a rapidly evolving automotive market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturers

- 3.2.2 Raw material suppliers

- 3.2.3 OEM

- 3.2.4 Distribution channel

- 3.2.5 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Cost breakdown analysis

- 3.9 Price analysis

- 3.9.1 By region

- 3.9.2 By propulsion

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Rise in vehicle electrification

- 3.11.1.2 Stricter emission and fuel efficiency regulations

- 3.11.1.3 Advancement in sensor technologies

- 3.11.1.4 Growth in fleet and telematics integration

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 Sensor calibration and accuracy issues

- 3.11.2.2 Integration complexity

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Analog

- 5.3 Digital

- 5.3.1 LCD

- 5.3.2 OLED

- 5.4 Hybrid display

- 5.5 Head-up display

Chapter 6 Market Estimates & Forecast, By Sensor, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Resistive

- 6.3 Capacitive

- 6.4 Ultrasonic

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric vehicles

- 7.3.1 Battery Electric Vehicles (BEV)

- 7.3.2 Plug-in Hybrid Electric Vehicles (PHEV)

- 7.3.3 Hybrid Electric Vehicles (HEV)

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Passenger vehicles

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUV

- 8.3 Commercial vehicles

- 8.3.1 Light Commercial Vehicles (LCV)

- 8.3.2 Medium Commercial Vehicles (MCV)

- 8.3.3 Heavy Commercial Vehicles (HCV)

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Aptiv

- 11.2 Auto Meter Products

- 11.3 AUTOGAUGE

- 11.4 Continental

- 11.5 DENSO

- 11.6 DunkTeam

- 11.7 Equus Products

- 11.8 Faria Beede Instruments

- 11.9 Gee Kay Equipments

- 11.10 GlowShift Gauges

- 11.11 Iontra

- 11.12 KUS USA

- 11.13 Marshall Instruments

- 11.14 Minda

- 11.15 Pricol

- 11.16 Robert Bosch

- 11.17 Sierra Instruments

- 11.18 Stoneridge

- 11.19 Wonfly

- 11.20 Yazaki

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日