|

市場調査レポート

商品コード

1740916

自動車用ディスクカップリングの市場機会、成長促進要因、産業動向分析、2025~2034年予測Automotive Disc Couplings Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用ディスクカップリングの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月21日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

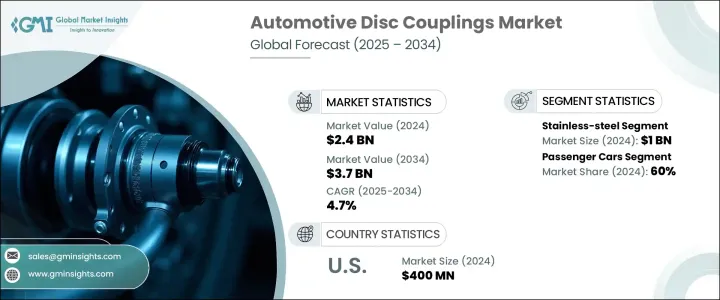

自動車用ディスクカップリングの世界市場規模は、2024年に24億米ドルとなり、CAGR 4.7%で成長し、2034年には37億米ドルに達すると予測されています。

これは、洗練されたインタラクティブな車両内装に対する需要の増加と、自動車分野へのスマート技術の統合の高まりによるものです。自動車メーカーが電動化と自動化への移行を続ける中、ディスク・カップリングは、機能性と美観の両方を優先する高性能システムをサポートする上で不可欠なものとなっています。特に電気自動車(EV)や自律走行プラットフォームでは、シームレスな統合とユーザー中心の体験が主流となっています。

自動車業界は急速に進化しており、次世代モビリティと車内テクノロジーのスマート化が急務となっています。ドライバーの嗜好がより直感的で没入感のある運転体験へとシフトする中、ディスク・カップリングは、従来のスイッチや制御装置を超えた革新的なシステムの開発を可能にしています。消費者は、タッチレスポンス、多機能サーフェス、統合ハプティクス、スマートインターフェースを提供する自動車を求めています。ディスク・カップリングは、ハードウェアとソフトウェアのギャップを埋め、安全性、応答性、快適性を向上させます。自動車メーカーは、過酷な条件、振動、高荷重に耐える信頼性、軽量性、高強度部品を要求する高度なドライブトレインおよび制御技術をますます採用するようになっています。このような需要が高まる中、ディスク・カップリングは、よりスムーズな動作とエネルギー効率の向上を保証するため、電動ドライブトレイン、インフォテインメント・モジュール、室内制御システムに統合されつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 24億米ドル |

| 予測金額 | 37億米ドル |

| CAGR | 4.7% |

テクノロジーは自動車用ディスクカップリングの機能を再定義し続けています。最新の開発動向は、インテリジェントな車両システムの増加傾向に沿った、組み込みセンサーと3Dタッチサーフェスを特徴としています。このような技術革新は、特にEVや自律走行車に関連するものであり、車内技術はハンズフリー、音声制御、応答性の高いユーザーインターフェイスを実現するために進化しています。自動車メーカーが従来の制御の複雑さを軽減し、ドライバーとのインタラクションの強化に取り組む中、ディスク・カップリングは、クリーンでインタラクティブなダッシュボードと集中制御ハブへのシフトを可能にします。ハプティック・フィードバック、ダイナミック・アンビエント・ライティング、アダプティブ・インフォテインメント・システムなどの機能は、精密な機械-電子接続に依存しており、ディスク・カップリングは不可欠なものとなっています。

素材別では、市場にはステンレススチール、アルミニウム、プラスチックのディスク・カップリングが含まれます。中でもステンレス鋼は、2024年の評価額が約10億米ドルで市場をリードしています。この優位性は、その優れた強度、耐熱性、高耐久性、高性能車や電気自動車に使用される重要な特性によるものです。ステンレス・スチール・カップリングは、激しい振動や過酷な条件にも効率的に対応できるため、長期的な信頼性と性能の一貫性が譲れない用途に最適です。自動車メーカーが持続可能で高出力のドライブトレインを重視する中、ステンレス鋼は、性能と寿命のために設計するエンジニアにとって、依然として最適な素材です。

自動車用ディスクカップリング市場は、最終用途に基づいて乗用車と商用車に分類されます。乗用車は2024年の世界市場の60%を占めています。この牙城は、消費者向け車両における電気技術と自律走行技術の採用が増加していることに起因しています。OEMは、スマート・インターフェース、軽量ドライブトレイン・コンポーネント、シームレスなインテリア・コントロールによって運転体験を最適化することに重点を置いています。コンパクトなEVからハイエンドの自律走行車に至るまで、ディスクカップリングは、インフォテインメントからパワートランスミッションに至るまで、あらゆる要素がスムーズかつ安全に作動することを保証します。

地域別では、北米自動車用ディスクカップリング市場は2024年に4億米ドルを創出しました。米国の自動車産業は、最先端のドライブトレイン技術の導入でリードし続けています。国内自動車メーカーは電動化に多額の投資を行っており、性能とドライバーの快適性を高めるために先進的なディスク・カップリングを組み込んでいます。米国全土でEVの導入が勢いを増す中、電動ドライブトレインの熱負荷や振動に対応できる高品質カップリングのニーズが大幅に高まっています。この地域では、自動車の電動化目標をサポートする軽量で効率的なコンポーネントの開発を目指した研究活動も活発化しています。

世界の自動車用ディスクカップリング市場の主要企業には、Flender、Dodge、Regal Rexnord、RENK-MAAG、Voith、John Crane、ESCO、Timken、REICH、Rathi Transpowerなどがあります。これらの企業は、戦略的提携、継続的な製品革新、研究開発の重視を通じて競争力を高めています。これらの企業は、次世代の自動車プラットフォームとの互換性を向上させるために、軽量で耐腐食性のある材料やモジュラーカップリングの設計に投資しています。また、これらの企業の多くは、エネルギー効率や性能重視のソリューションに対する消費者の期待やOEMの要求の進化に沿ったスマート機能を統合することで、製品機能を進化させています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料供給者

- 部品供給業者

- 製造業者

- テクノロジープロバイダー

- 流通チャネル分析

- 最終用途

- 利益率分析

- サプライヤーの情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 特許分析

- 規制情勢

- コスト内訳分析

- 主なニュースと取り組み

- 影響要因

- 促進要因

- 電気自動車と自動運転車への移行

- 材料とセンシング技術の進歩

- 電気自動車と自動運転車への移行

- カスタマイズとブランド差別化のためのOEMイニシアチブ

- 業界の潜在的リスク&課題

- 開発および統合コストが高め

- レガシーシステムとの互換性の問題

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- フレキシブルカップリング

- 剛性カップリング

- ディスクカップリング

第6章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- ドライブトレインシステム

- 伝送システム

- パワートレインシステム

第8章 市場推計・予測:材料別2021-2034

- 主要動向

- ステンレス鋼

- アルミニウム

- プラスチック

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Altra

- ASA Electronics

- Challenge

- Coupling

- CURRAX

- Dodge

- ESCO

- Flender

- John Crane

- Korea Coupling

- Lovejoy

- R+W Coupling

- Rathi Transpower

- Regal Rexnord

- REICH

- RENK-MAAG

- Renold

- Timken

- Tsubakimoto

- Voith

The Global Automotive Disc Couplings Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 3.7 billion by 2034, fueled by the increasing demand for sophisticated, interactive vehicle interiors and the rising integration of smart technologies into the automotive sector. As vehicle manufacturers continue transitioning toward electrification and automation, disc couplings have become vital in supporting high-performance systems that prioritize both functionality and aesthetics. These components play a crucial role in linking mechanical and electronic subsystems, especially in electric vehicles (EVs) and autonomous platforms, where seamless integration and user-centric experiences are now the norm.

The automotive industry is evolving rapidly, with a sharp focus on next-gen mobility and smarter in-cabin technologies. As driver preferences shift toward more intuitive and immersive driving experiences, disc couplings are enabling the development of innovative systems that go beyond traditional switches and controls. Consumers are looking for vehicles that offer touch-responsive, multifunctional surfaces, integrated haptics, and smart interfaces-and disc couplings help bridge the gap between hardware and software, enhancing safety, responsiveness, and comfort. Automakers are increasingly embracing advanced drivetrain and control technologies that demand reliable, lightweight, and high-strength components capable of withstanding harsh conditions, vibrations, and high loads. With this demand on the rise, disc couplings are being integrated into electric drivetrains, infotainment modules, and interior control systems to ensure smoother operation and improved energy efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $3.7 Billion |

| CAGR | 4.7% |

Technology continues to redefine the functionality of automotive disc couplings. The latest developments feature embedded sensors and 3D touch surfaces that align with the growing trend of intelligent vehicle systems. These innovations are particularly relevant in EVs and autonomous vehicles, where in-cabin technology is evolving to deliver hands-free, voice-controlled, and responsive user interfaces. As automakers work to reduce the complexity of traditional controls and enhance driver interaction, disc couplings enable the shift toward clean, interactive dashboards and centralized control hubs. Features like haptic feedback, dynamic ambient lighting, and adaptive infotainment systems rely on precise mechanical-electronic connectivity-making disc couplings indispensable.

In terms of material segmentation, the market includes stainless steel, aluminum, and plastic disc couplings. Among these, stainless steel led the market with a valuation of around USD 1 billion in 2024. This dominance stems from its superior strength, resistance to heat, and high durability-key attributes for use in high-performance and electric vehicles. Stainless steel couplings can efficiently handle intense vibrations and extreme conditions, making them ideal for applications where long-term reliability and performance consistency are non-negotiable. As automakers emphasize sustainable and high-output drivetrains, stainless steel remains the go-to material for engineers designing for performance and longevity.

Based on end use, the automotive disc couplings market is categorized into passenger cars and commercial vehicles. Passenger cars accounted for 60% of the global market in 2024. This stronghold is attributed to the increasing adoption of electric and autonomous technologies in consumer vehicles. OEMs are placing greater focus on optimizing the driving experience with smart interfaces, lightweight drivetrain components, and seamless interior controls-all of which demand the integration of robust disc coupling systems. From compact EVs to high-end autonomous cars, disc couplings ensure that every element, from infotainment to power transmission, operates smoothly and safely.

Regionally, the North America Automotive Disc Couplings Market generated USD 400 million in 2024. The U.S. automotive industry continues to lead with the implementation of cutting-edge drivetrain technologies. Domestic automakers are investing heavily in electrification and are incorporating advanced disc couplings to boost performance and driver comfort. With EV adoption gaining momentum across the U.S., the need for high-quality couplings that can handle thermal loads and vibration in electric drivetrains is growing substantially. This region is also witnessing increased research activity aimed at developing lightweight, efficient components to support vehicle electrification targets.

Key players in the global automotive disc couplings market include Flender, Dodge, Regal Rexnord, RENK-MAAG, Voith, John Crane, ESCO, Timken, REICH, and Rathi Transpower. These companies are sharpening their competitive edge through strategic alliances, continuous product innovation, and a strong emphasis on research and development. They are investing in lightweight, corrosion-resistant materials and modular coupling designs to improve compatibility with next-gen automotive platforms. Many of these players are also advancing product capabilities by integrating smart features that align with evolving consumer expectations and OEM requirements for energy efficiency and performance-driven solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.3.2 Pricing and product strategies

- 3.2.1 Impact on trade

- 3.3 Technology & innovation landscape

- 3.4 Patent analysis

- 3.5 Regulatory landscape

- 3.6 Cost breakdown analysis

- 3.7 Key news & initiatives

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Shift toward electric and autonomous vehicles

- 3.8.1.2 Advancements in material and sensing technology

- 3.8.1.3 Shift toward electric and autonomous vehicles

- 3.8.1.4 OEM initiatives for customization and brand differentiation

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High development and integration costs

- 3.8.2.2 Compatibility issues with legacy systems

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Flexible couplings

- 5.3 Rigid couplings

- 5.4 Disc couplings

Chapter 6 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial Vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Medium Commercial Vehicles (MCV)

- 6.3.3 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Drivetrain system

- 7.3 Transmission system

- 7.4 Powertrain system

Chapter 8 Market Estimates & Forecast, By Material 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Stainless steel

- 8.3 Aluminum

- 8.4 Plastic

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Altra

- 10.2 ASA Electronics

- 10.3 Challenge

- 10.4 Coupling

- 10.5 CURRAX

- 10.6 Dodge

- 10.7 ESCO

- 10.8 Flender

- 10.9 John Crane

- 10.10 Korea Coupling

- 10.11 Lovejoy

- 10.12 R+W Coupling

- 10.13 Rathi Transpower

- 10.14 Regal Rexnord

- 10.15 REICH

- 10.16 RENK-MAAG

- 10.17 Renold

- 10.18 Timken

- 10.19 Tsubakimoto

- 10.20 Voith