|

市場調査レポート

商品コード

1740914

再生可能エネルギー変圧器市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Renewable Energy Transformer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 再生可能エネルギー変圧器市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月15日

発行: Global Market Insights Inc.

ページ情報: 英文 123 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

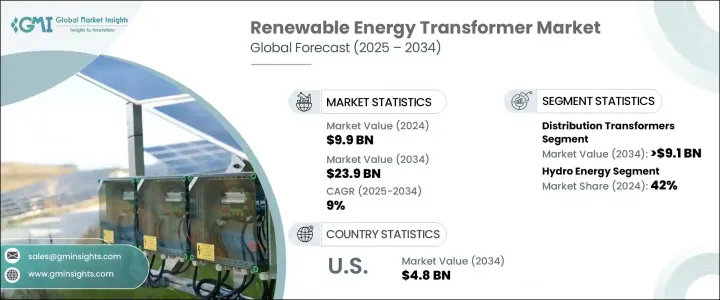

再生可能エネルギー変圧器の世界市場規模は2024年に99億米ドルとなり、CAGR 9%で成長し、2034年には239億米ドルに達すると予測されています。

クリーンエネルギー源への積極的な世界的移行に後押しされ、市場は大きな勢いを見せています。世界中の国々が太陽光、風力、水力発電プロジェクトに多額の投資を行っており、再生可能エネルギー入力の動的な性質を効率的に処理できる変圧器の大規模な需要につながっています。電力会社が老朽化したインフラを近代化し、政府がより厳しい再生可能エネルギー目標を実施する中、送電網の安定性を確保できる技術的に高度な変圧器の必要性はかつてないほど高まっています。

分散型エネルギー資源(DER)とマイクログリッドの台頭は、エネルギー貯蔵技術の進歩と相まって、特殊変圧器の重要性をさらに高めています。各社は、グリッド性能の最適化、エネルギー損失の最小化、予知保全の実現を目指して、変圧器の設計にAI主導の監視システムやIoT対応センサーを組み込む動きを強めています。電気自動車の着実な成長、分散型発電の拡大、スマートシティへの投資は、高性能再生可能エネルギー変圧器の必要性を強化し、世界市場全体に有望な機会を生み出しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 99億米ドル |

| 予測金額 | 239億米ドル |

| CAGR | 9% |

太陽光発電や風力発電へのシフトが進むとともに、よりクリーンなエネルギーの導入が世界的に推進されていることが、この市場の拡大に拍車をかけています。エネルギー貯蔵システムへの投資が増え、送電網が近代化されるにつれて、再生可能エネルギーの流れの変動を効率的に管理できる変圧器へのニーズが高まっています。デジタル監視システムとスマートグリッド技術の開発が変圧器設計の革新を促し、市場拡大にさらに貢献しています。政府による義務付けや電力会社による再生可能エネルギー利用目標は、引き続き需要を押し上げる大きな役割を果たしています。

見通しは明るいもの、複雑な規制環境、継続的なサプライチェーンの混乱、原材料価格の変動といった課題は依然として重大な懸念事項です。業界は、進化するエネルギー・環境基準に適合する先進的でカスタマイズ可能な変圧器設計に注力することで対応しています。トランプ政権下で施行された輸入鉄鋼、アルミニウム、電気部品への関税を含む貿易政策は、製造コストに大きな影響を与え、メーカーに戦略の調整を促しています。多くの企業は、経費管理を改善しリスクを最小化するため、台湾、メキシコ、ベトナムなど費用対効果の高い地域に生産施設を移転または拡張しています。

製品タイプ別では、配電用変圧器が市場を独占しており、2034年までに91億米ドルを生み出すと予測されています。これらの変圧器は、太陽光や風力などの再生可能エネルギーを既存の送電網に統合する上で重要な役割を果たしています。IoTセンサーやリアルタイム性能監視などの技術革新により、信頼性と運用効率が向上しています。また、大規模な再生可能エネルギー設備から都市中心部への大容量送電に不可欠な電力変圧器も、絶縁技術や冷却技術の進歩に支えられて力強い成長を遂げています。

水力エネルギー分野の再生可能エネルギー変圧器市場は、2024年に42%のシェアを占め、2034年までにCAGR 8%で成長すると予測されています。水力発電プロジェクトの拡大と、洋上および陸上風力発電設備の増加が市場成長の主な促進要因となっています。太陽光発電システムの変動する出力に対応するよう設計された変圧器の需要も大幅に増加しています。

米国の再生可能エネルギー変圧器市場は、2024年に19億米ドルを生み出しました。太陽光発電と風力発電技術の採用が拡大し、インフラの近代化努力とスマートグリッド統合が相まって、米国市場は持続的な拡大が見込まれています。

世界の再生可能エネルギー変圧器市場で事業を展開している主要企業には、Aditya Energy、ABC Transformers、GE Vernova、ACTOM、Acutran、AEP Group、Celme、Hammond Power Solutions、CG Power、Daelim、Deltron Electricals、Eaton、Elsewedy Electric、HD Hyundai Electric、Hitachi Energy、Hyosung Heavy Industries、MGM Transformers、Mitsubishi Electric、Ormazabal、Prolec Energy、Siemens Energy、Virginia Transformer、WEGなどがあります。これらの企業は、エネルギー効率と持続可能性における製品革新を優先し、高度な監視システムを取り入れ、再生可能エネルギー・インフラに対する需要の高まりに対応するため、新興市場に戦略的に進出しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略的ダッシュボード

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:製品別、2021-2034

- 主要動向

- 配電用変圧器

- 電力変圧器

- インバータデューティトランス

- その他

第6章 市場規模・予測:冷却により、2021-2034

- 主要動向

- ドライタイプ

- オイル浸漬

第7章 市場規模・予測:評価順、2021-2034

- 主要動向

- 10 MVA未満

- 10 MVA以上から100 MVA以下

- 100 MVA以上から600 MVA以下

- 600MVA以上

第8章 市場規模・予測:用途別、2021-2034

- 主要動向

- 水力エネルギー

- 風力発電所

- 太陽光発電

- その他

第9章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- ロシア

- 英国

- イタリア

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- エジプト

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第10章 企業プロファイル

- ABC Transformers

- ACTOM

- Acutran

- Aditya Energy

- AEP Group

- Celme

- CG Power

- Daelim

- Deltron Electricals

- Eaton

- Elsewedy Electric

- GE Vernova

- Hammond Power Solutions

- HD Hyundai Electric

- Hitachi Energy

- Hyosung Heavy Industries

- MGM Transformers

- Mitsubishi Electric

- Ormazabal

- Prolec Energy

- Siemens Energy

- Virginia Transformer

- WEG

The Global Renewable Energy Transformer Market was valued at USD 9.9 billion in 2024 and is estimated to grow at a CAGR of 9% to reach USD 23.9 billion by 2034. Driven by an aggressive global transition toward clean energy sources, the market is witnessing substantial momentum. Countries across the world are investing heavily in solar, wind, and hydroelectric power projects, leading to a massive demand for transformers capable of efficiently handling the dynamic nature of renewable energy inputs. As utility providers modernize aging infrastructure and governments enforce stricter renewable energy targets, the need for technologically advanced transformers that can ensure grid stability has never been higher.

The rise of distributed energy resources (DERs) and microgrids, combined with advancements in energy storage technologies, are further boosting the importance of specialized transformers. Companies are increasingly integrating AI-driven monitoring systems and IoT-enabled sensors into transformer designs, aiming to optimize grid performance, minimize energy loss, and enable predictive maintenance. The steady growth of electric vehicles, expanding decentralized power generation, and investments in smart cities are reinforcing the necessity for high-performance renewable energy transformers, creating promising opportunities across global markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.9 Billion |

| Forecast Value | $23.9 Billion |

| CAGR | 9% |

The increasing shift toward solar and wind power, along with a worldwide push for cleaner energy adoption, is fueling this market expansion. As energy storage systems receive more investments and power grids are modernized, there is a growing need for transformers that can efficiently manage the variability of renewable energy flows. The development of digital monitoring systems and smart grid technologies is driving innovations in transformer designs, further contributing to market growth. Government mandates and renewable energy usage targets set by utility companies continue to play a major role in boosting demand.

Despite the positive outlook, challenges such as complex regulatory environments, ongoing supply chain disruptions, and fluctuating raw material prices remain critical concerns. The industry is responding by focusing on advanced, customizable transformer designs that meet evolving energy and environmental standards. Trade policies, including tariffs on imported steel, aluminum, and electrical components enacted during the Trump administration, have significantly impacted production costs, pushing manufacturers to adjust strategies. Many companies are relocating or expanding production facilities to cost-effective regions like Taiwan, Mexico, and Vietnam to better manage expenses and minimize risks.

In terms of product types, distribution transformers dominate the market and are projected to generate USD 9.1 billion by 2034. These transformers play a vital role in integrating renewable energy sources like solar and wind into the existing grid. Innovations such as IoT sensors and real-time performance monitoring are enhancing their reliability and operational efficiency. Power transformers, which are critical for transmitting high-capacity electricity from large-scale renewable installations to urban centers, are also seeing robust growth, supported by advancements in insulation and cooling technologies.

The renewable energy transformers market from the hydro energy segment accounted for a 42% share in 2024 and is anticipated to grow at a CAGR of 8% by 2034. Expanding hydropower projects, along with increasing offshore and onshore wind installations, are key drivers for market growth. The demand for transformers designed to handle the fluctuating outputs of solar photovoltaic systems is also rising significantly.

The U.S. Renewable Energy Transformer Market generated USD 1.9 billion in 2024. With a growing adoption of solar and wind technologies, coupled with infrastructure modernization efforts and smart grid integration, the U.S. market is poised for sustained expansion.

Key companies operating in the Global Renewable Energy Transformer Market include Aditya Energy, ABC Transformers, GE Vernova, ACTOM, Acutran, AEP Group, Celme, Hammond Power Solutions, CG Power, Daelim, Deltron Electricals, Eaton, Elsewedy Electric, HD Hyundai Electric, Hitachi Energy, Hyosung Heavy Industries, MGM Transformers, Mitsubishi Electric, Ormazabal, Prolec Energy, Siemens Energy, Virginia Transformer, and WEG. These companies are prioritizing product innovation in energy efficiency and sustainability, incorporating advanced monitoring systems, and strategically expanding into emerging markets to meet the rising demand for renewable energy infrastructure.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's Analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL Analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Product, 2021 - 2034 (USD Million, ‘000 Units)

- 5.1 Key trends

- 5.2 Distribution transformer

- 5.3 Power transformer

- 5.4 Inverter duty transformer

- 5.5 Others

Chapter 6 Market Size and Forecast, By Cooling, 2021 - 2034 (USD Million, ‘000 Units)

- 6.1 Key trends

- 6.2 Dry type

- 6.3 Oil immersed

Chapter 7 Market Size and Forecast, By Rating, 2021 - 2034 (USD Million, ‘000 Units)

- 7.1 Key trends

- 7.2 ≤ 10 MVA

- 7.3 > 10 MVA to ≤ 100 MVA

- 7.4 > 100 MVA to ≤ 600 MVA

- 7.5 > 600 MVA

Chapter 8 Market Size and Forecast, By Application, 2021 - 2034 (USD Million, ‘000 Units)

- 8.1 Key trends

- 8.2 Hydro energy

- 8.3 Wind farm

- 8.4 Solar PV

- 8.5 Others

Chapter 9 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, ‘000 Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 Russia

- 9.3.4 UK

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 South Korea

- 9.4.4 India

- 9.4.5 Australia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Qatar

- 9.5.4 Egypt

- 9.5.5 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

Chapter 10 Company Profiles

- 10.1 ABC Transformers

- 10.2 ACTOM

- 10.3 Acutran

- 10.4 Aditya Energy

- 10.5 AEP Group

- 10.6 Celme

- 10.7 CG Power

- 10.8 Daelim

- 10.9 Deltron Electricals

- 10.10 Eaton

- 10.11 Elsewedy Electric

- 10.12 GE Vernova

- 10.13 Hammond Power Solutions

- 10.14 HD Hyundai Electric

- 10.15 Hitachi Energy

- 10.16 Hyosung Heavy Industries

- 10.17 MGM Transformers

- 10.18 Mitsubishi Electric

- 10.19 Ormazabal

- 10.20 Prolec Energy

- 10.21 Siemens Energy

- 10.22 Virginia Transformer

- 10.23 WEG