航空機用電動モーターの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Aircraft Electric Motors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740907

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

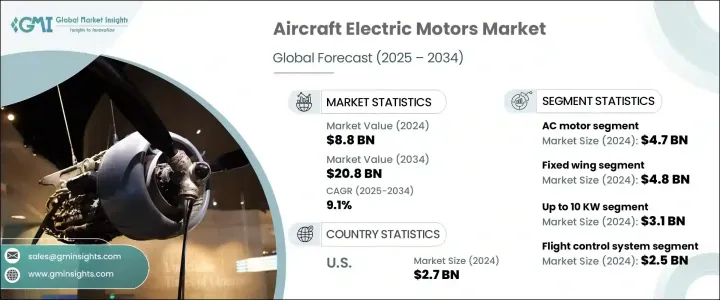

世界の航空機用電動モーター市場は、2024年に88億米ドルと評価され、CAGR 9.1%で成長し、2034年には208億米ドルに達すると推定されています。

この成長の主な要因は、分散型電気推進(DEP)の採用増加とともに、アーバンエアモビリティ(UAM)と電気垂直離着陸(eVTOL)航空機の需要増です。同市場はまた、特に中国の航空宇宙部品や電気部品に対する関税をはじめとする外部要因の影響も受けており、これによって原材料コストが上昇し、世界的なサプライチェーンが混乱しています。これに対応するため、メーカー各社はサプライヤーを多様化し、輸入品への依存度を下げるため、一部の生産活動を再調達しつつあります。航空機に使用される電動モーターは、よりクリーンで持続可能な技術の開発に向けた業界の取り組みにおいて重要な役割を果たすようになってきており、環境問題への関心と規制圧力が強まるにつれて、この動向は加速すると予想されます。

UAMとeVTOL航空機の急速な開発は、航空機用電動モーター市場拡大の主な要因です。これらの航空機は、従来の地上移動に代わる、よりクリーンで効率的な代替手段を提供することで、都市交通に革命を起こそうとしています。UAMとeVTOL技術は、混雑と交通渋滞が毎日の通勤者にとって大きな課題となっている都市部での短距離、高効率飛行のために特別に設計されています。従来の航空機とは異なり、eVTOLは長い滑走路を必要としないため、インフラを設置するスペースが限られる都市環境に最適です。その垂直離着陸能力と環境に優しい電気推進システムが相まって、eVTOLは都市交通の未来形として位置づけられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 88億米ドル |

| 予測金額 | 208億米ドル |

| CAGR | 9.1% |

電動モーター別に、市場は大きく2つのタイプに分けられます:ACモーターとDCモーターです。2024年には、ACモーターが市場を独占し、47億米ドルの大きなシェアを占めました。ACモーターは、効率性、低メンテナンス性、持続的な出力能力により、電気航空機やハイブリッド電気航空機の高い需要に特に適しています。可変周波数ドライブ(VFD)を含むパワーエレクトロニクスの技術的進歩が、特に信頼性の高い長期的性能を必要とする航空用途での人気をさらに高めています。ACモーターは、航空業界がより持続可能で効率的な飛行ソリューションを推進する上で極めて重要です。

2024年に48億米ドルと評価される固定翼機セグメントは、航空機用電動モーター市場の成長に寄与するもう1つの大きな要因です。このセグメントの拡大は、持続可能な航空技術が重視されるようになったことが背景にあります。電動モーターは短距離路線やリージョナルフライトに最適で、排出ガスの低減や運航コストの削減に役立ちます。各国政府や規制当局が環境基準を強化する中、固定翼機のハイブリッド化や完全電動化を推進する動きが強まっています。メーカー各社はこうした技術革新に積極的に投資しており、機体の軽量化と総合性能の向上を図りつつ、モーター効率の向上に注力しています。

米国市場では、航空機用電動モーターの需要も急増しています。2024年、米国の航空機用電動モーター市場は27億米ドルを生み出し、先進ハイブリッド電気研究開発への連邦政府の多額の投資に支えられています。NASAの電動パワートレイン飛行実証プログラムのような政府の支援によるイニシアチブは、民間および軍用航空用途の両方で電動推進システムの技術的ブレークスルーを加速するのに役立ち、この成長において重要な役割を果たしています。これらのイニシアティブはまた、航空機システムへの電動モーターの統合課題を克服し、この技術の普及に向けた実現可能性を確保することにも重点を置いています。

航空機用電動モーター市場の主要企業には、Emrax、Safran Group、H3X Technologies、Liebherr Aerospace、Moog、Maxon、Wright Electric、THINGAP、Electromech Technologiesなどがあります。これらの企業は、電動モーターの効率、耐久性、総合性能を高めるために研究開発に多額の投資を行っています。また、航空機メーカーと戦略的パートナーシップを結び、新しい航空機設計に電気推進システムを統合しようとしています。技術革新に注力し、ハイブリッド電気用途に特化したモーターを開発することで、これらの企業は、持続可能な航空ソリューションに対する需要の高まりの最前線に自らを位置づけています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 主要部品の価格変動

- サプライチェーン再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- アーバンエアモビリティ(UAM)とeVTOL開発の急増

- 短距離便の需要増加

- 分散型電気推進(DEP)の台頭

- ハイブリッド電気航空機の開発

- 電動モーターの技術的進歩

- 業界の潜在的リスク&課題

- バッテリーのエネルギー密度の限界

- 熱管理と安全リスク

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021~2034年

- 主要動向

- ACモーター

- DCモーター

第6章 市場推計・予測:機種別、2021~2034年

- 主要動向

- 固定翼

- 回転翼

- 無人航空機

- 先進エアモビリティ

第7章 市場推計・予測:出力別、2021~2034年

- 主要動向

- 最大10kW

- 10~200kW

- 200kW以上

第8章 市場推計・予測:用途別、2021~2034年

- 主要動向

- 推進システム

- 飛行制御システム

- 環境制御システム

- 作動システム

- 客室内装システム

- その他

第9章 市場推計・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- AMETEK

- ARC Systems

- Electromech Technologies

- Emrax

- Evolito

- H3X Technologies

- KDE Direct

- Liebherr Aerospace

- Maxon

- Meggitt

- MGM Compro

- Moog

- Safran Group

- THINGAP

- Turnigy Power Systems

- Windings

- Wright Electric

- Xoar International

目次

The Global Aircraft Electric Motors Market was valued at USD 8.8 billion in 2024 and is estimated to grow at a CAGR of 9.1% to reach USD 20.8 billion by 2034. This growth is primarily fueled by the rising demand for Urban Air Mobility (UAM) and electric Vertical Takeoff and Landing (eVTOL) aircraft, along with the increasing adoption of distributed electric propulsion (DEP). The market has also felt the impact of external factors, including tariffs, especially on Chinese aerospace and electrical components, which have driven up raw material costs and disrupted global supply chains. In response, manufacturers are diversifying suppliers and reshoring some production efforts to lessen dependence on imports. The electric motors used in aviation are becoming a critical part of the industry's efforts to develop cleaner, more sustainable technologies, and this trend is expected to accelerate as environmental concerns and regulatory pressures intensify.

The rapid development of Urban Air Mobility and eVTOL aircraft is a key driver of the aircraft electric motors market expansion. These aircraft are poised to revolutionize urban transportation by offering a cleaner and more efficient alternative to traditional ground travel. UAM and eVTOL technologies are specifically designed for short-distance, high-efficiency flights in urban areas, where congestion and traffic jams have become major challenges for daily commuters. Unlike traditional aircraft, eVTOLs do not require long runways, making them ideal for city environments where space for infrastructure is often limited. Their vertical takeoff and landing capabilities, coupled with their eco-friendly electric propulsion systems, are positioning them as the future of urban transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.8 Billion |

| Forecast Value | $20.8 Billion |

| CAGR | 9.1% |

As for the electric motors themselves, the market is divided into two main types: AC and DC motors. In 2024, AC motors dominate the market, holding a substantial share of USD 4.7 billion. The efficiency, low maintenance, and sustained power output capabilities of AC motors make them particularly well-suited for the high demands of electric and hybrid-electric aircraft. Technological advancements in power electronics, including variable frequency drives (VFDs), have further bolstered their popularity, especially for aviation applications requiring reliable, long-term performance. AC motors are crucial to the aviation industry's push toward more sustainable and efficient flight solutions.

The fixed-wing aircraft segment, valued at USD 4.8 billion in 2024, is another major contributor to the aircraft electric motors market's growth. This segment's expansion is driven by the growing emphasis on sustainable aviation technologies. Electric motors are ideal for short-haul and regional flights, where they help to lower emissions and reduce operational costs. As governments and regulators tighten environmental standards, there is an increasing push for hybrid and fully electric fixed-wing aircraft designs. Manufacturers are heavily investing in these innovations, focusing on improving motor efficiency while reducing airframe weight and enhancing overall performance.

In the U.S. market, the demand for aircraft electric motors is also surging. In 2024, the U.S. aircraft electric motors market generated USD 2.7 billion, supported by substantial federal investments in advanced hybrid-electric research and development. Government-backed initiatives, such as NASA's electric powertrain flight demonstration program, are playing a significant role in this growth by helping to accelerate technological breakthroughs in electric propulsion systems for both civil and military aviation applications. These initiatives are also focused on overcoming the integration challenges of electric motors into aircraft systems, ensuring the technology's feasibility for widespread use.

Leading players in the Aircraft Electric Motors Market include Emrax, Safran Group, H3X Technologies, Liebherr Aerospace, Moog, Maxon, Wright Electric, THINGAP, and Electromech Technologies. These companies are heavily investing in research and development to enhance the efficiency, durability, and overall performance of their electric motors. They are also forming strategic partnerships with aircraft manufacturers to integrate electric propulsion systems into new aircraft designs. By focusing on innovation and developing motors specifically tailored for hybrid-electric applications, these companies are positioning themselves at the forefront of the growing demand for sustainable aviation solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump Administration Tariffs

- 3.2.1 Impact on Trade

- 3.2.1.1 Trade Volume Disruptions

- 3.2.1.2 Retaliatory Measures

- 3.2.2 Impact on the Industry

- 3.2.2.1 Supply-Side Impact

- 3.2.2.1.1 Price Volatility in Key Components

- 3.2.2.1.2 Supply Chain Restructuring

- 3.2.2.1.3 Production Cost Implications

- 3.2.2.2 Demand-Side Impact (Selling Price)

- 3.2.2.2.1 Price Transmission to End Markets

- 3.2.2.2.2 Market Share Dynamics

- 3.2.2.2.3 Consumer Response Patterns

- 3.2.2.1 Supply-Side Impact

- 3.2.3 Key Companies Impacted

- 3.2.4 Strategic Industry Responses

- 3.2.4.1 Supply Chain Reconfiguration

- 3.2.4.2 Pricing and Product Strategies

- 3.2.4.3 Policy Engagement

- 3.2.5 Outlook and Future Considerations

- 3.2.1 Impact on Trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Surge in urban air mobility (UAM) & eVTOL development

- 3.3.1.2 Increasing demand for short-haul flights

- 3.3.1.3 Rise of distributed electric propulsion (DEP)

- 3.3.1.4 Hybrid-electric aircraft development

- 3.3.1.5 Technological advancements in electric motors

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Limited energy density of batteries

- 3.3.2.2 Thermal management & safety risks

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 AC motor

- 5.3 DC motor

Chapter 6 Market Estimates and Forecast, By Aircraft Type, 2021 - 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 Fixed wing

- 6.3 Rotary wing

- 6.4 Unmanned aerial vehicles

- 6.5 Advanced air mobility

Chapter 7 Market Estimates and Forecast, By Output Power, 2021 - 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Up to 10 kW

- 7.3 10–200 kW

- 7.4 Above 200 kW

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 Propulsion systems

- 8.3 Flight control systems

- 8.4 Environmental control systems

- 8.5 Actuation systems

- 8.6 Cabin interior systems

- 8.7 Other

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million & Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AMETEK

- 10.2 ARC Systems

- 10.3 Electromech Technologies

- 10.4 Emrax

- 10.5 Evolito

- 10.6 H3X Technologies

- 10.7 KDE Direct

- 10.8 Liebherr Aerospace

- 10.9 Maxon

- 10.10 Meggitt

- 10.11 MGM Compro

- 10.12 Moog

- 10.13 Safran Group

- 10.14 THINGAP

- 10.15 Turnigy Power Systems

- 10.16 Windings

- 10.17 Wright Electric

- 10.18 Xoar International

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日