デジタル故障レコーダーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Digital Fault Recorder Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 123 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740903

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

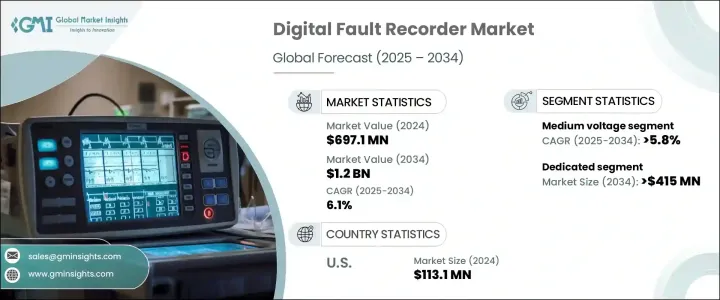

世界のデジタル故障レコーダー市場は、2024年には6億9,710万米ドルとなり、電力インフラが広く近代化されるにつれてCAGR 6.1%で成長し、2034年には12億米ドルに達すると推定されています。

エネルギー・システムが従来のモデルからインテリジェントで自動化されたネットワークへと進化するにつれ、正確なモニタリングと迅速な故障診断の必要性がこれまで以上に高まっています。DFRはこの変革において不可欠なツールとして台頭しており、ユーティリティ企業にグリッドの挙動をリアルタイムで把握させ、迅速な運用判断、停電の最小化、安定した電力供給の維持を可能にしています。

現代の電力システムは、より多くの再生可能エネルギー源、分散型エネルギー資産、スマート技術を統合しており、非常に複雑なネットワークを形成しています。この複雑さにより、従来の機能を超える高度な診断ツールが求められています。デジタル・フォールト・レコーダは、高速データ・キャプチャ、リモート・システム・アクセス、および高度な分析を提供することで、これらの要件を満たします。これにより、ユーティリティ企業は、詳細なイベント再構築を実行し、故障の原因をピンポイントで特定できるようになり、ダウンタイムが短縮されるだけでなく、長期的なグリッド効率も向上します。デジタル変電所とスマートグリッドソリューションの普及がこの動向を加速しており、インテリジェントで応答性の高い故障検出システムの需要がさらに高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 6億9,710万米ドル |

| 予測金額 | 12億米ドル |

| CAGR | 6.1% |

業界の優先事項が回復力と運用の透明性にシフトする中、DFRは電力管理戦略においてますます重要な役割を果たしています。DFRのデジタルアーキテクチャは、より広範な制御システムへのシームレスな統合を可能にし、最新のグリッド環境への高い適応性を実現しています。データ収集の自動化と実用的な洞察の提供により、デジタル・フォールト・レコーダーは、ユーティリティ企業がより合理的で予測的な保守体制を実現できるよう支援しています。これは、グリッドの信頼性、持続可能な配電、費用対効果の高いインフラのアップグレードに焦点を当てた世界のエネルギー目標に合致しています。

しかし、DFR業界はマクロ経済の圧力と無縁ではないです。輸入品、特にエレクトロニクス、鉄鋼、アルミニウム関連に導入された関税は、さまざまな産業部門の部品コストに影響を与えています。デジタル・フォールト・レコーダーには半導体、通信モジュール、金属ケーシングが含まれるため、これらの投入部品の価格変動は生産コストや利益率に影響を与える可能性があります。市場参入企業は、サプライチェーンを最適化し、現地生産に投資し、デリケートな材料への依存度を下げる設計革新を追求することで、こうした課題を乗り切らなければならないです。

製品タイプ別では、DFR専用分野は2034年までに4億1,500万米ドルを超えると予想されています。これらのデバイスは故障記録専用で、多機能システムよりも高い精度と安定性を提供します。他のグリッド制御要素から独立して動作するように設計された専用レコーダーは、中断のない性能が重要な高信頼性設備で特に評価されています。その精度と集中的な機能性により、補助的なプロセスの干渉を受けずに堅牢な故障検出を必要とする部門に好まれます。

中電圧カテゴリーは、通常1kVから36kVまでのシステムをカバーし、2034年までのCAGRは5.8%を超えると予測されています。この成長の原動力は、配電網、産業事業、再生可能エネルギーを統合する施設内での故障監視に対する需要の高まりです。公益事業者は、故障位置の精度を向上させ、サービス中断を減らすデジタル監視ツールを組み込むことで、レガシー・グリッド・インフラストラクチャを積極的にアップグレードしています。その結果、DFRは高圧ネットワークの近代化プロジェクトにおいて重要なコンポーネントとなりつつあり、ローカル診断と遠隔測定をサポートするその能力は、システムの信頼性を高めています。

米国では、デジタル故障レコーダー市場は着実な成長を続けています。2022年には1億350万米ドルに達し、2023年には1億810万米ドルに上昇、2024年には1億1,310万米ドルに再び上昇しました。老朽化したインフラのアップグレードへの投資の増加に加え、異常気象や変動するエネルギー需要に対する送電網の脆弱性が高まっているため、電力会社はより高度な故障解析ソリューションを採用するようになっています。業務の継続性を確保し、予測可能な中断と予期せぬ中断の両方からグリッドを保護することに重点が置かれています。

業界大手は、広範な世界事業と確立された研究開発能力によって競争力を維持しています。市場シェアの20%以上を占める企業は、北米、欧州、アジアを含む主要地域で製造施設を運営しています。世界なプレゼンスにより、コスト効率の高い生産と迅速な製品供給が可能となっています。技術革新と信頼性において長年の評判を持つこれらの企業は、デジタル時代への深化に伴い、デジタル故障レコーダー業界の軌跡を左右する立場にあります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略的ダッシュボード

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:タイプ別、2021-2034

- 主要動向

- 専用型

- 多機能

第6章 市場規模・予測:電圧別、2021-2034

- 主要動向

- 中電圧

- 高電圧

- 超高電圧

第7章 市場規模・予測:用途別、2021-2034

- 主要動向

- 高速外乱

- 低速外乱

- 定常状態

第8章 市場規模・予測:設備別、2021-2034

- 主要動向

- 発電

- 送電

- 配電

第9章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- アジア太平洋地域

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第10章 企業プロファイル

- ABB

- Ametek

- Ducati Energia

- Eaton

- Elspec

- E-Max Instruments

- Erlphase

- General Electric

- Hitachi

- Kinkei

- Kocos

- Logiclab

- Mehta Tech

- Qualitrol

- Schneider Electric

- Siemens

目次

The Global Digital Fault Recorder Market was valued at USD 697.1 million in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 1.2 billion by 2034 as power infrastructure undergoes widespread modernization. As energy systems evolve from traditional models to intelligent, automated networks, the need for precise monitoring and rapid fault diagnosis is becoming more critical than ever. DFRs are emerging as indispensable tools in this transformation, offering utilities real-time insight into grid behavior, allowing them to make swift operational decisions, minimize outages, and maintain consistent power delivery.

Modern electrical systems are integrating more renewable energy sources, distributed energy assets, and smart technologies, creating highly complex networks. This complexity demands advanced diagnostic tools that go beyond conventional capabilities. Digital fault recorders meet these requirements by offering high-speed data capture, remote system access, and advanced analytics. They enable utilities to perform detailed event reconstruction and pinpoint the origin of faults, which not only reduces downtime but also enhances long-term grid efficiency. The widespread adoption of digital substations and smart grid solutions is accelerating this trend, further boosting demand for intelligent, responsive fault detection systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $697.1 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 6.1% |

As industry priorities shift toward resilience and operational transparency, DFRs are playing an increasingly vital role in power management strategies. Their digital architecture allows seamless integration into broader control systems, making them highly adaptable in modern grid environments. With their ability to automate data collection and provide actionable insights, digital fault recorders are empowering utilities to achieve more streamlined and predictive maintenance regimes. This aligns with global energy goals focused on grid reliability, sustainable power distribution, and cost-effective infrastructure upgrades.

However, the DFR industry is not immune to macroeconomic pressures. Tariffs introduced on imported goods, particularly those related to electronics, steel, and aluminum, are impacting component costs across various industrial sectors. Since digital fault recorders include semiconductors, communication modules, and metal casings, any price volatility in these inputs can influence production costs and profit margins. Market participants must navigate these challenges by optimizing supply chains, investing in localized manufacturing, and pursuing design innovations that reduce dependency on sensitive materials.

In terms of product types, the dedicated DFR segment is expected to generate more than USD 415 million by 2034. These devices are purpose-built for fault recording and offer higher accuracy and stability than multifunctional systems. Designed to operate independently of other grid control elements, dedicated recorders are especially valued in high-reliability installations where uninterrupted performance is critical. Their precision and focused functionality make them a preferred choice for sectors that demand robust fault detection without the interference of ancillary processes.

The medium voltage category, typically covering systems between 1kV and 36kV, is forecast to expand at a CAGR exceeding 5.8% through 2034. This growth is driven by heightened demand for fault monitoring within distribution networks, industrial operations, and facilities integrating renewable energy. Utilities are actively upgrading legacy grid infrastructure by embedding digital monitoring tools that improve fault location accuracy and reduce service interruptions. As a result, DFRs are becoming key components in medium-voltage network modernization projects, where their ability to support local diagnostics and telemetry enhances system reliability.

Within the United States, the digital fault recorder market continues to show steady progress. It reached USD 103.5 million in 2022, climbed to USD 108.1 million in 2023, and rose again to USD 113.1 million in 2024. The growing investment in aging infrastructure upgrades, along with increased grid vulnerability to extreme weather events and fluctuating energy demands, is encouraging utilities to adopt more sophisticated fault analysis solutions. The focus is on ensuring operational continuity and protecting the grid from both predictable and unexpected disruptions.

Industry leaders maintain a competitive edge through extensive global operations and well-established research and development capabilities. Companies holding more than 20% of the market share collectively operate manufacturing facilities in key regions including North America, Europe, and Asia. Their global presence allows for cost-effective production and quick product delivery. With long-standing reputations for innovation and reliability, these firms are positioned to influence the trajectory of the digital fault recorder industry as it moves deeper into the digital age.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Dedicated

- 5.3 Multifunctional

Chapter 6 Market Size and Forecast, By Voltage, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Medium voltage

- 6.3 High voltage

- 6.4 Extra high voltage

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 High speed disturbance

- 7.3 Low speed disturbance

- 7.4 Steady state

Chapter 8 Market Size and Forecast, By Installation, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Generation

- 8.3 Transmission

- 8.4 Distribution

Chapter 9 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 France

- 9.3.3 Germany

- 9.3.4 Italy

- 9.3.5 Russia

- 9.3.6 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Australia

- 9.4.3 India

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Turkey

- 9.5.4 South Africa

- 9.5.5 Egypt

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 Ametek

- 10.3 Ducati Energia

- 10.4 Eaton

- 10.5 Elspec

- 10.6 E-Max Instruments

- 10.7 Erlphase

- 10.8 General Electric

- 10.9 Hitachi

- 10.10 Kinkei

- 10.11 Kocos

- 10.12 Logiclab

- 10.13 Mehta Tech

- 10.14 Qualitrol

- 10.15 Schneider Electric

- 10.16 Siemens

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 123 Pages

- 納期

- 2~3営業日