|

市場調査レポート

商品コード

1740897

先進戦闘ヘルメット市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測Advanced Combat Helmet Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 先進戦闘ヘルメット市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月30日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

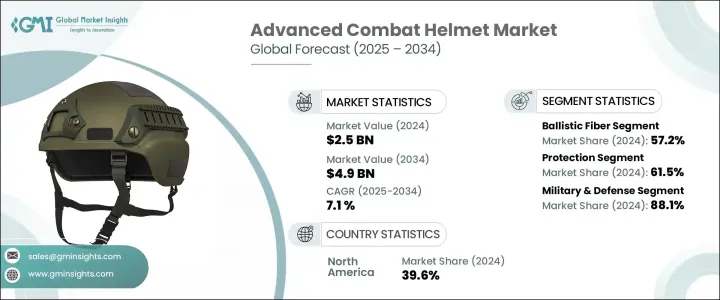

先進戦闘ヘルメットの世界市場は、2024年には25億米ドルと評価され、CAGR 7.1%で成長し、2034年には49億米ドルに達すると推定されています。

この拡大は、防衛軍が進化する戦場の脅威に対応するために兵士の保護具をアップグレードすることを優先しているため、様々な地域で軍事費が増加していることが主な要因です。高度な戦闘用ヘルメットはもはや頭部を保護するためだけのものではなく、通信、状況認識、他の戦闘システムとの統合のためのプラットフォームとしての役割を果たすようになっています。各国政府が軍隊の生存能力と作戦準備態勢の強化を目指す中、技術的に先進的なヘルメットへの需要は高まり続けています。これらのヘルメットは、統合型ヘッドアップディスプレイ、モジュール式アドオン、拡張現実システムとの互換性などの機能を含むよう、再構築されつつあります。

地政学的緊張と予測不可能な紛争地域が、軍事機関に次世代保護ヘッドギアへの投資をさらに促しています。しかし、外部経済要因も市場力学に影響を与えています。貿易政策の転換、特に輸入原材料への関税賦課は、サプライチェーンを混乱させ、ヘルメット製造に使用される必須部品のコストを上昇させました。こうした混乱は、生産スケジュールの長期化と調達コストの上昇につながっています。インフレ圧力はさらに複雑さを増し、調達サイクルを遅らせ、国防予算にさらなる負担をかける可能性があります。こうした課題にもかかわらず、市場は堅調な成長を維持すると予想され、各社は技術革新に注力し、勢いを維持するために新たな防衛契約を履行しています。防衛機関が多様な作戦環境に合わせた装備を求める中、特定の戦闘シナリオに合わせたカスタマイズと性能の最適化が重要な焦点となってきています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 25億米ドル |

| 予測金額 | 49億米ドル |

| CAGR | 7.1% |

素材別に、市場はバリスティックファイバー、熱可塑性プラスチック、金属に区分されます。2024年には、バリスティックファイバーが市場シェアの57.2%を占める。この素材は、優れた耐衝撃性、軽量特性、過酷な条件下での信頼性により、多くのメーカーに選ばれ続けています。メーカー各社は、これらの繊維の強度対重量比を改善する新たな方法を模索し続けており、兵士の敏捷性を損なうことなく最終製品が最大限の保護を提供できるようにしています。

用途別に見ると、市場は保護、通信、視覚支援に分けられます。2024年には、保護カテゴリーが61.5%のシェアを占め、このセグメントを支配しています。弾道弾の脅威や非対称戦争に対する懸念の高まりが、強固な防御機構を提供するヘルメットへの需要を強めています。最新の戦闘用ヘルメットは現在、さまざまな種類の弾薬や爆発物の衝撃に耐えながら、さまざまな地形でも機能性を維持できるように設計されています。快適性、装着性、多機能性が開発の中核であり、予測不可能でリスクの高い作戦で兵士をサポートします。

最終用途のセグメンテーションには、軍事・防衛、法執行機関が含まれます。軍と防衛が市場の大半を占め、2024年のシェアは88.1%でした。この優位性の背景には、兵士の生存能力を向上させ、任務を確実に成功させる必要性があります。ヘルメットには、ノイズキャンセリング通信システム、暗視装置、リアルタイムデータ伝送などの機能が搭載され、戦場での認識と対応力が強化されています。各機関は、保護機能だけでなく、統合されたシステムによって運用効率を高める装備を求め続けています。

地域別では、北米が2024年に39.6%のシェアで市場をリードしており、高い防衛費と最先端技術の早期導入への強い志向に支えられています。地域の防衛機関は、状況認識と戦場での連携を向上させる先進的なヘッドギアに積極的に投資しています。開発中のヘルメットには、ディスプレイや環境センサーが搭載され、人間工学に基づいて改良されたものが多く、現代戦の要求に応えています。

米国だけでも、2034年までに18億米ドルに達すると予測されています。国防の近代化に対する継続的な投資は依然として重要な推進力であり、快適性、保護性能、技術強化を兼ね備えた最先端のヘルメットの開発に重点が置かれています。軍備のアップグレードは、軍隊が進化する脅威に対して十分な装備を確保するために優先されます。

競合情勢は依然として激しく、上位5社で市場全体の約55~60%を占めています。主な企業は、世界の防衛部門からの拡大する要求に対応するヘルメットを提供するため、研究開発に力を注いでいます。国際的な軍事組織との戦略的提携や長期供給契約は、安定した注文量を確保し、市場でのポジショニングを高めるために結ばれています。戦場での要求が複雑化する中、ヘルメットメーカーは安全性と戦略的優位性の両方を提供する高性能製品を提供することで歩調を合わせています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 価格変動

- サプライチェーン再構築

- 生産コストへの影響

- 需要側への影響

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 戦闘用ヘルメットへの先進素材の採用増加

- 特殊作戦部隊や法執行部隊からの需要増加

- 世界の軍事費の増加

- 兵士の安全基準と規制の強化

- 軍事近代化プログラムの拡大

- 業界の潜在的リスク&課題

- 開発と調達費が高め

- C4ISRシステムとの複雑な統合

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材料別、2021-2034

- 主要動向

- バリスティックファイバー

- 熱可塑性

- 金属

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 保護

- コミュニケーション

- 視覚支援

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 軍事・防衛

- 法執行機関

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- 3M Company

- ArmorSource LLC

- DuPont de Nemours Inc.

- Galvion

- Gentex Corporation

- HARD SHELL

- Honeywell International Inc.

- Indian Armour Systems Pvt. Ltd.

- MKU Limited

- Point Blank Enterprises

- Revision Military Inc.

The Global Advanced Combat Helmet Market was valued at USD 2.5 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 4.9 billion by 2034. This expansion is largely driven by increased military expenditures across various regions as defense forces prioritize upgrading soldier protection gear to meet evolving battlefield threats. Advanced combat helmets are no longer just about head protection; they now serve as platforms for communication, situational awareness, and integration with other combat systems. As governments aim to enhance the survivability and operational readiness of their armed forces, demand for technologically advanced helmets continues to rise. These helmets are being reimagined to include features such as integrated heads-up displays, modular add-ons, and compatibility with augmented reality systems.

Geopolitical tensions and unpredictable conflict zones have further compelled military agencies to invest in next-generation protective headgear. However, external economic factors have also influenced market dynamics. Trade policy shifts, especially the imposition of tariffs on imported raw materials, have disrupted the supply chain and increased the cost of essential components used in manufacturing helmets. These disruptions have led to longer production timelines and rising procurement costs. Inflationary pressures add another layer of complexity, potentially slowing acquisition cycles and placing added strain on defense budgets. Despite these challenges, the market is expected to maintain steady growth, with companies focusing on innovation and fulfilling new defense contracts to maintain momentum. Customization and performance optimization for specific combat scenarios are becoming a key focus area as defense agencies seek gear tailored to diverse operational environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.5 Billion |

| Forecast Value | $4.9 Billion |

| CAGR | 7.1% |

Based on material, the market is segmented into ballistic fiber, thermoplastic, and metal. In 2024, ballistic fiber accounted for 57.2% of the market share. This material remains the preferred choice for many manufacturers due to its superior impact resistance, lightweight properties, and reliability under extreme conditions. Manufacturers continue to explore new ways to improve the strength-to-weight ratio of these fibers, ensuring the final product offers maximum protection without compromising soldier agility.

By application, the market is divided into protection, communication, and visual assistance. The protection category dominated the segment in 2024, holding a 61.5% share. Rising concerns over ballistic threats and asymmetric warfare have intensified the demand for helmets offering robust defense mechanisms. Modern combat helmets are now being designed to withstand various types of ammunition and explosive impacts while also remaining functional in different terrains. Comfort, wearability, and multi-functionality are core to their development, supporting soldiers in unpredictable and high-risk operations.

End-use segmentation includes military and defense, and law enforcement agencies. Military and defense made up the majority of the market, with an 88.1% share in 2024. The need to improve soldier survivability and ensure mission success underlies this dominance. Helmets are being equipped with features like noise-canceling communication systems, night vision readiness, and real-time data transmission to enhance battlefield awareness and responsiveness. Agencies continue to demand gear that not only offers protection but also enhances operational efficiency through integrated systems.

Regionally, North America led the market with a 39.6% share in 2024, supported by high defense spending and a strong inclination toward early adoption of cutting-edge technologies. Regional defense bodies are actively investing in advanced headgear that improves situational awareness and battlefield coordination. Helmets in development often feature mounted displays, environmental sensors, and upgraded ergonomics to meet the demands of modern warfare.

The market in the United States alone is projected to reach USD 1.8 billion by 2034. Continuous investment in defense modernization remains a key driver, with a focus on developing state-of-the-art helmets that combine comfort, protection, and technological enhancement. Military equipment upgrades are prioritized to ensure forces are well-equipped for evolving threats.

The competitive landscape remains intense, with the top five companies accounting for roughly 55-60% of the total market. Key players are channeling efforts into research and development to offer helmets that address the expanding list of requirements from global defense sectors. Strategic alliances and long-term supply contracts with international military organizations are being formed to secure consistent order volumes and enhance market positioning. As battlefield requirements become more complex, helmet manufacturers are keeping pace by delivering high-performance products that offer both safety and strategic advantages.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump Administration Tariffs Analysis

- 3.2.1 Impact on Trade

- 3.2.1.1 Trade Volume Disruptions

- 3.2.1.2 Retaliatory Measures

- 3.2.2 Impact on the Industry

- 3.2.2.1 Supply-Side Impact (Raw material)

- 3.2.2.1.1 Price Volatility

- 3.2.2.1.2 Supply Chain Restructuring

- 3.2.2.1.3 Production Cost Implications

- 3.2.2.2 Demand-Side Impact

- 3.2.2.2.1 Price Transmission to End Markets

- 3.2.2.2.2 Market Share Dynamics

- 3.2.2.2.3 Consumer Response Patterns

- 3.2.2.1 Supply-Side Impact (Raw material)

- 3.2.3 Key Companies Impacted

- 3.2.4 Strategic Industry Responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on Trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing adoption of advanced materials for combat helmets

- 3.3.1.2 Rising demand from special operations and law enforcement units

- 3.3.1.3 Increased global military expenditure

- 3.3.1.4 Increased soldier safety standards and regulations

- 3.3.1.5 Growing military modernization programs

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High development and procurement costs

- 3.3.2.2 Complex integration with C4ISR systems

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Material, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Ballistic fiber

- 5.3 Thermoplastic

- 5.4 Metal

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Protection

- 6.3 Communication

- 6.4 Visual assistance

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 Military & defense

- 7.3 law enforcement agencies

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Bn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M Company

- 9.2 ArmorSource LLC

- 9.3 DuPont de Nemours Inc.

- 9.4 Galvion

- 9.5 Gentex Corporation

- 9.6 HARD SHELL

- 9.7 Honeywell International Inc.

- 9.8 Indian Armour Systems Pvt. Ltd.

- 9.9 MKU Limited

- 9.10 Point Blank Enterprises

- 9.11 Revision Military Inc.