|

市場調査レポート

商品コード

1740889

低密度ポリエチレン包装の市場機会、成長促進要因、産業動向分析、2025~2034年予測Low-density Polyethylene Packaging (LDPE) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 低密度ポリエチレン包装の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月21日

発行: Global Market Insights Inc.

ページ情報: 英文 155 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

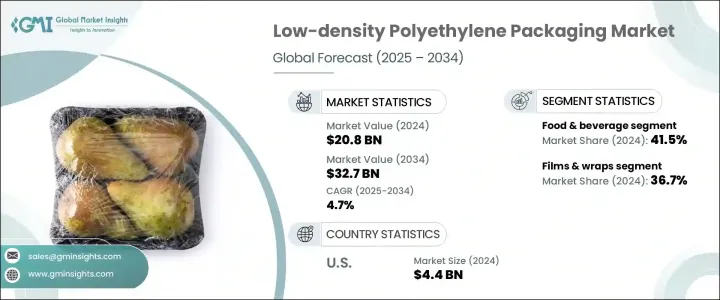

世界の低密度ポリエチレン包装市場は、2024年に208億米ドルと評価され、食品、医薬品、パーソナルケア業界全体の堅調な需要に牽引され、CAGR 4.7%で成長し、2034年には327億米ドルに達すると推定されています。

この成長は、消費者部門と産業部門の両方におけるLDPEパッケージングの用途拡大を反映しています。世界の包装産業が急速に進化する中、LDPEはその柔軟性、耐久性、低製造コスト、高い耐湿性により、依然として好まれている素材です。企業も消費者も製品の安全性と賞味期限を優先する中、LDPE包装はさまざまなサプライチェーンで製品の完全性を確保する上で重要な役割を果たしています。

また、eコマースやデジタルショッピングプラットフォームの動向の高まりも、製品を無傷のまま保ちながら輸送やハンドリングのストレスに耐えることのできる柔軟な包装材料への需要を後押ししています。さらに、輸送コストの削減に役立つ軽量で省スペースのパッケージングへのシフトにより、LDPEはメーカーにとって頼りになる素材となっています。食品の安全性と包装衛生に対する規制の焦点の高まりは、市場の可能性をさらに高めています。持続可能性への取り組みが進む中、メーカーは現在、リサイクル可能で環境に優しいLDPE包装ソリューションの製造に取り組んでおり、環境意識の高い消費者や規制当局の間で支持を集めています。業務効率とブランドアピールの向上を目指した包装形態と素材の革新が、世界の多くの包装企業の戦略的方向性を形成しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 208億米ドル |

| 予測金額 | 327億米ドル |

| CAGR | 4.7% |

LDPEは耐湿性と柔軟性に優れているため、飲食品分野で広く使用されており、生鮮品の包装に最適です。ライフスタイルの変化や都市化によってコンビニエンス・フードへの需要が高まっていることが、LDPEベースのパッケージの使用を大幅に後押ししています。消費者は、特に新興経済諸国において、すぐに食べられる食事や1回分の食品に大きく傾いており、鮮度と安全性を維持するためにLDPEフィルムや容器に依存しています。衛生的な特性を持つLDPEは、食品の賞味期限を延ばし、現代の消費習慣や流通モデルに合致しています。

医薬品およびパーソナルケア分野では、ヘルスケア意識の高まり、世界の高齢化、個人の健康増進への支出の増加により、LDPEパッケージングが引き続き支持を集めています。特にパンデミック後の状況では、衛生や汚染防止への関心が高まっており、使い捨てや改ざん防止の包装形態へのシフトが加速しています。LDPEはコスト効率が高く加工が容易なため、メーカーが厳しい安全基準と包装基準を満たす上で中心的な役割を果たしています。軟膏チューブや薬袋からパーソナルケア用小袋に至るまで、LDPEは複数の製品カテゴリーでその汎用性と有効性を証明しています。

しかし、市場は貿易関連の混乱という逆風に直面しています。トランプ政権時代に導入された鉄鋼、アルミニウム、中国製部品への関税は、パッケージングのサプライチェーン全体に波及効果をもたらしました。これらの政策は、LDPE樹脂や完成包装資材のコスト上昇につながり、生産コストの上昇圧力となり、最終的には消費者物価の上昇につながりました。メキシコやカナダなどの主要パートナーとの貿易摩擦も原材料の流れを制限し、必須部品の入手に課題をもたらし、メーカーの物流を複雑にしています。

製品セグメンテーションでは、フィルムとラップのカテゴリーが2024年の市場シェア36.7%を占めました。これらの製品は、その適応性と防湿性により、食品包装、工業用包装、eコマース出荷に広く使用されています。手頃な価格と使いやすさから、製品の安全性を確保しながら包装コストを最適化したい企業に好まれています。保護包装のニーズが各分野で高まるにつれ、この分野は成長を続けています。

2024年には、飲食品産業が圧倒的な最終用途セグメントとして浮上し、41.5%の市場シェアを占めています。LDPE包装は鮮度と衛生を守るために広く使用されており、冷凍食品、スナック菓子、乳製品、加工食品に不可欠です。消費者がペースの速い、外出の多いライフスタイルを受け入れているため、LDPEのような柔軟で耐久性のある包装への依存度は、特に包装食品の消費が急増している新興市場において、高まる一方であると予想されます。

米国の低密度ポリエチレン(LDPE)包装市場は、2024年に44億米ドルと評価されました。ここでの成長は、主に食品、医薬品、eコマース部門からの安定した需要が牽引しています。加工技術の進歩と、安全性、衛生、規制遵守への関心の高まりが技術革新を促進しています。同時に、持続可能なパッケージングへの関心の高まりが、メーカーにリサイクルLDPEソリューションへの投資を促しています。こうした取り組みにより、企業は世界の持続可能性の目標に沿いながら、顧客の期待に応えることができるようになっています。

世界のLDPEパッケージング市場の主要企業には、Constantia Flexibles、Berry Global Inc.、Sealed Air、Amcor plcなどがあります。これらの企業は、競争力を維持するために技術的なアップグレードと持続可能な実践を活用しています。主な戦略には、製品ラインの拡大、サプライチェーンの回復力の向上、LDPE製品のリサイクル性の強化などがあり、環境問題への懸念や規制枠組みの進化に対応しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界の対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 影響要因

- 促進要因

- 包装食品・飲料部門の成長

- 医薬品とパーソナルケアの需要増加

- eコマースと小売流通の拡大

- 産業および農業用途での採用増加

- 軽量化と材料効率

- 業界の潜在的リスク&課題

- 環境問題と規制圧力

- リサイクル率が低く、循環性が限られている

- 促進要因

- 成長可能性分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 将来の市場動向

- ポーター分析

- PESTEL分析

- 規制情勢

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:包装形態別、2021-2034

- 主要動向

- バッグ&ポーチ

- ボトルと容器

- フィルム&ラップ

- チューブ

- その他

第6章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 飲食品

- パーソナルケア&化粧品

- 電気・電子機器

- 消費財

- 医薬品

- eコマース

- その他

第7章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- Amcor plc

- BENZ Packaging

- Berry Global Inc.

- Constantia Flexibles

- EPL Limited

- FKuR

- Inteplast Group

- Origin Pharma Packaging

- RKW Group

- SABIC

- Sealed Air

- Silgan Holdings

- Sirane Group

- Sonoco Products Company

- Strobel GmbH

- TC Transcontinental

- Thermo Fisher Scientific Inc.

- Westlake Corporation

The Global Low-Density Polyethylene Packaging Market was valued at USD 20.8 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 32.7 billion by 2034, driven by robust demand across food, pharmaceutical, and personal care industries. This growth reflects the expanding applications of LDPE packaging in both consumer and industrial sectors. With the global packaging industry rapidly evolving, LDPE remains a preferred material due to its flexibility, durability, low production cost, and high resistance to moisture. As businesses and consumers alike prioritize product safety and shelf-life, LDPE packaging plays a key role in ensuring product integrity across various supply chains.

The rising trend of e-commerce and digital shopping platforms also fuels the demand for flexible packaging materials that can withstand shipping and handling stress while keeping products intact. In addition, the shift toward lightweight, space-saving packaging that helps reduce transportation costs is making LDPE a go-to material for manufacturers. Growing regulatory focus on food safety and packaging hygiene is further enhancing the market potential. Amid ongoing efforts toward sustainability, manufacturers are now working on producing recyclable and eco-friendly LDPE packaging solutions, which are gaining traction among environmentally conscious consumers and regulators. Innovation in packaging formats and materials, aimed at boosting operational efficiency and brand appeal, is shaping the strategic direction of many packaging firms globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $20.8 billion |

| Forecast Value | $32.7 billion |

| CAGR | 4.7% |

LDPE is widely used in the food and beverage sector due to its moisture resistance and flexibility, making it ideal for packaging perishable products. The increasing demand for convenience food, driven by changing lifestyles and urbanization, is significantly boosting the use of LDPE-based packaging. Consumers are leaning heavily toward ready-to-eat meals and single-serve food products, especially in developing economies, which rely on LDPE films and containers to maintain freshness and safety. With its hygienic attributes, LDPE ensures an extended shelf life for food items, aligning with modern consumption habits and distribution models.

In the pharmaceutical and personal care segments, LDPE packaging continues to gain traction due to rising healthcare awareness, an aging global population, and higher spending on personal wellness. The heightened focus on hygiene and contamination prevention, particularly in the post-pandemic landscape, is accelerating the shift toward single-use and tamper-proof packaging formats. LDPE, being cost-effective and easy to process, is playing a central role in helping manufacturers meet stringent safety and packaging standards. From ointment tubes and medicine pouches to personal care sachets, LDPE is proving its versatility and effectiveness across multiple product categories.

However, the market has faced headwinds in the form of trade-related disruptions. Tariffs on steel, aluminum, and Chinese components introduced during the Trump administration caused a ripple effect throughout the packaging supply chain. These policies led to increased costs for LDPE resins and finished packaging materials, putting upward pressure on production expenses and ultimately raising consumer prices. Trade tensions with key partners like Mexico and Canada also restricted raw material flow, challenging the availability of essential components and adding to logistical complexity for manufacturers.

In terms of product segmentation, the films and wraps category accounted for a 36.7% market share in 2024. These products are widely used in food packaging, industrial wrapping, and e-commerce shipping due to their adaptability and moisture barrier properties. Their affordability and ease of use make them a preferred choice for businesses looking to optimize packaging costs while ensuring product safety. As the need for protective packaging grows across sectors, this segment continues to thrive.

The food and beverage industry emerged as the dominant end-use segment in 2024, holding a 41.5% market share. LDPE packaging is extensively used to safeguard freshness and hygiene, making it indispensable for frozen foods, snacks, dairy, and processed meals. As consumers embrace fast-paced, on-the-go lifestyles, the reliance on flexible and durable packaging like LDPE is only expected to grow, especially in emerging markets where packaged food consumption is surging.

The United States Low-Density Polyethylene (LDPE) Packaging Market was valued at USD 4.4 billion in 2024. Growth here is primarily driven by consistent demand from the food, pharmaceutical, and e-commerce sectors. Technological advancements in processing and the rising focus on safety, hygiene, and regulatory compliance are driving innovation. At the same time, increased interest in sustainable packaging is pushing manufacturers to invest in recycled LDPE solutions. These efforts are enabling businesses to meet customer expectations while aligning with global sustainability goals.

Major players in the global LDPE packaging market include Constantia Flexibles, Berry Global Inc., Sealed Air, and Amcor plc. These companies are leveraging technological upgrades and sustainable practices to stay competitive. Key strategies involve expanding product lines, improving supply chain resilience, and enhancing the recyclability of LDPE products to address environmental concerns and evolving regulatory frameworks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key raw material

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 key companies impacted

- 3.2.4 strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Growth in packaged food & beverage sector

- 3.3.1.2 Rising demand in pharmaceuticals & personal care

- 3.3.1.3 Expansion of e-commerce & retail distribution

- 3.3.1.4 Increased adoption in industrial and agricultural applications

- 3.3.1.5 Lightweighting and material efficiency

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 Environmental concerns and regulatory pressure

- 3.3.2.2 Low recycling rate and limited circularity

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Technological & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news and initiatives

- 3.8 Future market trends

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Regulatory landscape

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Packaging Type, 2021 - 2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Bags & pouches

- 5.3 Bottles & containers

- 5.4 Films & wraps

- 5.5 Tubes

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Food and beverages

- 6.3 Personal care & cosmetics

- 6.4 Electricals & electronics

- 6.5 Consumer goods

- 6.6 Pharmaceuticals

- 6.7 E-commerce

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Amcor plc

- 8.2 BENZ Packaging

- 8.3 Berry Global Inc.

- 8.4 Constantia Flexibles

- 8.5 EPL Limited

- 8.6 FKuR

- 8.7 Inteplast Group

- 8.8 Origin Pharma Packaging

- 8.9 RKW Group

- 8.10 SABIC

- 8.11 Sealed Air

- 8.12 Silgan Holdings

- 8.13 Sirane Group

- 8.14 Sonoco Products Company

- 8.15 Strobel GmbH

- 8.16 TC Transcontinental

- 8.17 Thermo Fisher Scientific Inc.

- 8.18 Westlake Corporation