電気配線相互接続システム市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Electrical Wiring Interconnection System (EWIS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 167 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740885

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

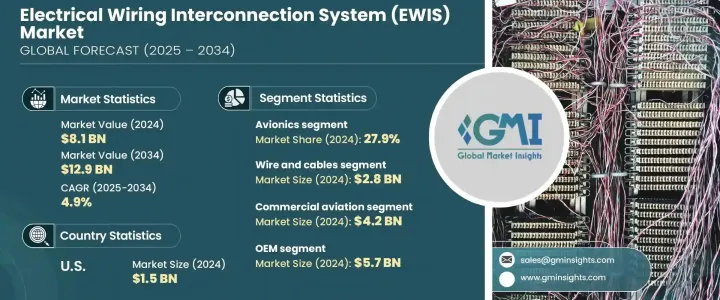

世界の電気配線相互接続システム市場は、2024年に81億米ドルと評価され、CAGR 4.9%で成長し、2034年には129億米ドルに達すると推定されています。

航空業界では、機内エンターテインメントやリアルタイムのコネクティビティ・システムの利用の高まりと相まって、統合された電気システムへの需要が高まっており、配線のインフラが再構築されつつあります。UAM(Urban Air Mobility)プラットフォームやeVTOL(Electric Vertical Takeoff and Landing)航空機の出現は、EWIS全体のイノベーションを加速させています。これらの航空機は、複雑な電気およびデータ伝送タスクを処理できる軽量で高性能な配線を必要とします。持続可能な航空と電化強化への関心の高まりは、進化する飛行技術とシームレスに統合する高度な配線システムへの依存度を高めています。

しかし、アルミニウム、銅、鋼鉄の関税による材料費高騰のため、業界は圧力に直面しています。これらの金属はコネクター、ケーブル、エンクロージャーを含むEWIS部品の生産に不可欠です。その結果、メーカーとエンドユーザーは生産コストの上昇を経験しています。さらに、中国からの電子部品や半導体の輸入に対する関税は、サプライチェーンを妨げ、次世代EWIS部品、特にデジタルシステムや自動化された航空機プラットフォームで使用される部品の開発に影響を及ぼしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 81億米ドル |

| 予測金額 | 129億米ドル |

| CAGR | 4.9% |

ワイヤ・ケーブル分野は、耐熱性、信号忠実性、軽量設計を提供する先端材料への需要が主因で、2024年に28億米ドルを生み出しました。現代の航空機はデジタル技術や電気技術をますます取り入れるようになっており、光ファイバーや配電ソリューションを含む高性能配線システムへの要求が高まっています。絶縁技術やシールド技術の革新により、より安全で効率的な運用が可能になると同時に、航空機全体の軽量化にも貢献します。

用途別では、アビオニクス部門が2024年に27.9%のシェアを占める。コックピット制御、通信システム、飛行データ処理のデジタル化に伴い、信頼性が高くコンパクトなEWISへの需要が大きく伸びています。高精度ルーティング、電磁干渉シールド、デジタル・ダッシュボードとの統合は、特に軍用機や民間機では今や標準となっています。これらのシステムは、高度な航空機サブシステム内での一貫した電力フローとデータ接続性を保証します。

米国の電気配線相互接続システム(EWIS)市場は、航空宇宙・防衛分野の拡大により、2024年に15億米ドルを創出しました。同国は、より多くの電動航空機、都市航空モビリティ・プロジェクトの増加、国防予算の増加に注力しており、先進EWISの展開をサポートしています。自動化およびモジュラー配線システムへの投資は、強力なOEMおよびサプライヤーネットワークとともに、引き続き国内需要を促進しています。

TE Connectivity、Collins Aerospace、Honeywell International Inc.、Amphenol Corporation、Safranなどの大手企業は、RandD施設の拡張、軽量材料の技術革新への投資、モジュール設計能力の強化などの戦略を採用しています。また、航空機メーカーや防衛機関と戦略的パートナーシップを結び、次世代ソリューションを共同開発しているところも多いです。各社は、迅速な航空機組立と長期的な運用信頼性をサポートするデジタル統合、スマート診断、拡張可能な配線システムに注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 民間および防衛分野における航空機納入の急増

- 軽量で燃費の良い航空機の需要の増加

- 航空機の電動化および全電動化への移行の増加(MEA/AESA)

- 機内エンターテイメント(IFE)と接続システムの普及が進む

- 都市型航空モビリティ(UAM)とeVTOL航空機の出現

- 業界の潜在的リスク&課題

- 開発・製造コストが高め

- 厳格な規制遵守と認証の遅延

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- ワイヤーとケーブル(1フィートあたり)

- コネクタ

- 電気接地およびボンディング装置

- 電気接続部

- クランプ

- 圧力シール

- その他

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 航空電子機器

- コックピットコントロール

- 飛行制御システム(FCS)

- 飛行管理システム(FMS)

- その他

- インテリア

- 機内エンターテイメント(IFE)

- ガレー船

- 座席電源

- キャビン管理

- 推進システム

- エンジン

- 補助動力装置(APU)

- その他

- 機体

- 翼

- しっぽ

- その他

第7章 市場推計・予測:航空機種別、2021-2034

- 主要動向

- 商用航空

- ナローボディ機(NBA)

- ワイドボディ機(WBA)

- 超大型航空機(VLA)

- 地域輸送機(RTA)

- 軍事航空

- 戦闘機

- 輸送機

- 軍用ヘリコプター

- ビジネス航空および一般航空

- ビジネスジェット

- ヘリコプター

- ピストン航空機

- ターボプロップ機

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Amphenol Corporation

- Boeing

- Collins Aerospace(Raytheon Technologies)

- Co-Operative Industries Aerospace &Defense(kSARIA)

- Ducommun

- E.I.S. Electronics GmbH

- Elektro Metall Export

- Honeywell International Inc.

- InterConnect Wiring

- JST Sales America

- kSARIA Corporation

- Leonardo

- Molex

- PEI-Genesis

- Pic Wire &Cable(Angelus Corporation)

- Safran

- TE Connectivity

- W. L. Gore &Associates

目次

The Global Electrical Wiring Interconnection System Market was valued at USD 8.1 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 12.9 billion by 2034, driven by the rapid transition toward all-electric and more-electric aircraft playing a central role in driving this growth. Increased demand for integrated electric systems in aviation, combined with the rising use of in-flight entertainment and real-time connectivity systems, is reshaping wiring infrastructure. The emergence of Urban Air Mobility (UAM) platforms and electric vertical takeoff and landing (eVTOL) aircraft are accelerating innovation across the EWIS landscape. These aircraft require lightweight, high-performance wiring capable of handling complex electrical and data transmission tasks. Rising interest in sustainable aviation and enhanced electrification is increasing dependency on advanced wiring systems that integrate seamlessly with evolving flight technologies.

However, the industry faces pressure due to elevated material costs from tariffs on aluminum, copper, and steel. These metals are critical to producing EWIS components, including connectors, cables, and enclosures. As a result, manufacturers and end-users are experiencing increased production costs. In addition, tariffs on electronic and semiconductor imports from China are hampering supply chains and affecting the development of next-gen EWIS components, particularly those used in digital systems and automated aircraft platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.1 Billion |

| Forecast Value | $12.9 Billion |

| CAGR | 4.9% |

The wire and cables segment generated USD 2.8 billion in 2024, largely due to demand for advanced materials that offer thermal resistance, signal fidelity, and lightweight designs. As modern aircraft increasingly incorporate digital and electric technologies, there's a heightened requirement for high-performance wiring systems, including fiber optics and power distribution solutions. Innovations in insulation and shielding technologies enable safer and more efficient operations while helping reduce overall aircraft weight.

In terms of application, the avionics segment held a 27.9% share in 2024. With the digital transformation of cockpit controls, communication systems, and flight data processing, the demand for reliable and compact EWIS is growing significantly. Precision routing, electromagnetic interference shielding, and integration with digital dashboards are now standard, especially in military and commercial fleets. These systems ensure consistent power flow and data connectivity within advanced aircraft subsystems.

U.S. Electrical Wiring Interconnection System (EWIS) Market generated USD 1.5 billion in 2024 due to its expanding aerospace and defense sectors. The country's focus on more electric aircraft, increasing urban air mobility projects, and rising defense budgets support advanced EWIS deployment. Investments in automation and modular wiring systems, along with strong OEM and supplier networks, continue to fuel national demand.

Leading players such as TE Connectivity, Collins Aerospace, Honeywell International Inc., Amphenol Corporation, and Safran are adopting strategies like expanding RandD facilities, investing in lightweight material innovation, and enhancing modular design capabilities. Many are forming strategic partnerships with aircraft manufacturers and defense agencies to co-develop next-gen solutions. Companies focus on digital integration, smart diagnostics, and scalable wiring systems that support rapid aircraft assembly and long-term operational reliability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Surge in aircraft deliveries across commercial and defense segments

- 3.7.1.2 Growth in demand for lightweight and fuel-efficient aircraft

- 3.7.1.3 Rise in shift toward more-electric and all-electric aircraft (MEA/AESA)

- 3.7.1.4 Increasing proliferation of in-flight entertainment (IFE) and connectivity systems

- 3.7.1.5 Emergence of Urban Air Mobility (UAM) and eVTOL Aircraft

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High development and manufacturing costs

- 3.7.2.2 Stringent regulatory compliance and certification delays

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Million, Foot & Units)

- 5.1 Key trends

- 5.2 Wire and cables (per foot)

- 5.3 Connectors

- 5.4 Electrical grounding and bonding devices

- 5.5 Electrical splices

- 5.6 Clamps

- 5.7 Pressure seals

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Avionics

- 6.2.1 Cockpit controls

- 6.2.2 Flight control systems (FCS)

- 6.2.3 Flight management systems (FMS)

- 6.2.4 Others

- 6.3 Interiors

- 6.3.1 Inflight entertainment (IFE)

- 6.3.2 Galleys

- 6.3.3 In-seat power

- 6.3.4 Cabin management

- 6.4 Propulsion system

- 6.4.1 Engine

- 6.4.2 Auxiallry power unit (APU)

- 6.4.3 Other

- 6.5 Airframe

- 6.5.1 Wings

- 6.5.2 Tail

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Aviation Type, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Commercial aviation

- 7.2.1 Narrow body aircraft (NBA)

- 7.2.2 Wide body aircraft (WBA)

- 7.2.3 Very large aircraft (VLA)

- 7.2.4 Regional transport aircraft (RTA)

- 7.3 Military aviation

- 7.3.1 Fighter jets

- 7.3.2 Transport aircraft

- 7.3.3 Military helicopters

- 7.4 Business and general aviation

- 7.4.1 Business jets

- 7.4.2 Helicopters

- 7.4.3 Piston aircraft

- 7.4.4 Turboprop aircraft

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Amphenol Corporation

- 10.2 Boeing

- 10.3 Collins Aerospace (Raytheon Technologies)

- 10.4 Co-Operative Industries Aerospace & Defense (kSARIA)

- 10.5 Ducommun

- 10.6 E.I.S. Electronics GmbH

- 10.7 Elektro Metall Export

- 10.8 Honeywell International Inc.

- 10.9 InterConnect Wiring

- 10.10 JST Sales America

- 10.11 kSARIA Corporation

- 10.12 Leonardo

- 10.13 Molex

- 10.14 PEI-Genesis

- 10.15 Pic Wire & Cable (Angelus Corporation)

- 10.16 Safran

- 10.17 TE Connectivity

- 10.18 W. L. Gore & Associates

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 167 Pages

- 納期

- 2~3営業日