|

市場調査レポート

商品コード

1740881

アルミニウム板とコイルの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Aluminum Sheets and Coils Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| アルミニウム板とコイルの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月25日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

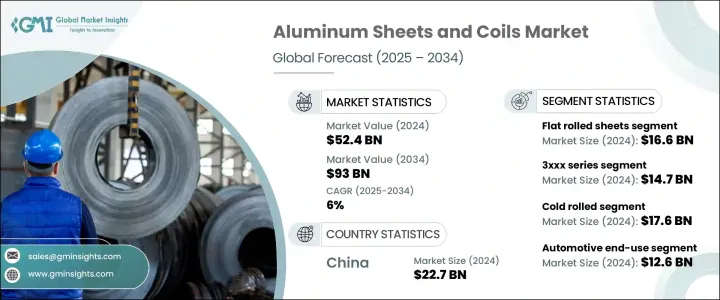

アルミニウム板とコイルの世界市場規模は、2024年に524億米ドルとなり、CAGR 6%で成長し、2034年には930億米ドルに達すると推定されています。

この成長は、工業生産性の継続的な上昇と持続可能な材料への嗜好の高まりに大きく起因しています。アルミニウムの軽量特性は、エネルギー効率の改善と排出量の削減を目指す部門にとって理想的です。産業が電化や先端技術を取り入れるにつれて、強度を損なうことなく製品の軽量化に貢献できるアルミニウムは、不可欠な存在になりつつあります。よりクリーンなエネルギーや輸送手段へのシフトが加速しており、特に電動モビリティの需要が高まっていることも、市場の拡大に拍車をかけています。これと並行して、自動化やデジタル化といった進化する製造技術は、増大する世界的需要に対応するため、より迅速で精密な生産を可能にしています。軽量で耐久性に優れ、リサイクル可能な素材を優先する業界のニーズに対応するため、生産業者は競争を繰り広げており、こうした効率化は極めて重要です。市場はまた、熾烈な競争と、各地域で高まる低排出ガス生産ソリューションの推進によって形成されており、世界の持続可能性目標に沿った、費用対効果の高い高性能アルミニウムソリューションの必要性が高まっています。

平板圧延アルミニウム板とコイルは2024年に166億米ドルの市場規模を記録し、2025年から2034年にかけてCAGR 5.7%で成長すると予想されています。特に耐久性、柔軟性、軽量性が大量生産で重視される場合、その適応性と経済性が基幹産業全体の最重要選択肢となります。これらの材料は、マテリアルハンドリングが容易で、複数の製造工程に適合するため、一般的に好まれています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 524億米ドル |

| 予測金額 | 930億米ドル |

| CAGR | 6% |

クラッド板と陽極酸化板は、耐食性、外観、表面耐久性を必要とする用途で引き続き関心を集めています。これらのアルミニウムは、精密さが要求される分野で好まれており、表面の完全性を向上させるためのコーティング技術や合金組成の革新を促しています。このようなアルミニウムの採用増加は、特殊な製品カテゴリーにおける競合を激化させています。

模様入り、波形、穴あきアルミニウム板などの動向は、性能と構造を強化する機能的デザインへの傾向を反映し、美的および工業的用途に関連性を見出しています。これらのタイプは、構造補強や建築のディテールにおける汎用性で注目を集めています。

合金の種類の中では、3xxxシリーズが2024年に147億米ドルの評価額に達し、2034年までCAGR 6.1%で成長すると予測されています。このシリーズは1xxxグループと並んで、耐食性、導電性、コストパフォーマンスの高さから市場シェアを独占しています。これらのグレードは、機能的性能と手頃な価格が重要な要素となる分野で特に人気が高く、生産者は高い生産効率と一貫した品質を維持しながら、コスト競争力を維持することに重点を置いています。

一方、5xxxおよび6xxxシリーズは、高強度で溶接可能なアルミニウムを必要とする分野、特にインフラストラクチャーや重要用途で安定した需要を獲得し続けています。2XXX、7XXX、8XXXシリーズの高グレードアルミニウムは、耐久性と精度が重要な、技術的に高度な市場での性能ニーズを満たします。

加工方法に関しては、冷間圧延アルミセグメントは2024年に176億米ドルの市場価値を持ち、2034年までCAGR 6.4%で成長すると予想されます。このカテゴリーは、優れた表面仕上げ、厳しい公差、強化された機械的特性などの利点があり、重要な用途で幅広く使用されています。熱間圧延材は精度が劣るが、厳しい環境下での強度と信頼性のためによく選ばれています。

自動車セクターで使用されるアルミニウム板とコイルは、2024年に126億米ドルを占め、24%の市場シェアを占め、予測期間を通じてCAGR 6.1%で成長する見込みです。これらの材料は、特に車両の軽量化と燃費の向上を実現するために、現代の車両設計に不可欠なものです。その用途は構造部品やエネルギー貯蔵システムにまで及んでおり、メーカー各社は主要な車両アーキテクチャにアルミニウムの採用を増やしています。

建築・建設業界も需要に大きく貢献しており、アルミニウムの弾力性、軽量性、美観を活かした構造、屋根、断熱のニーズがあります。包装や電子機器では、アルミニウムはその安全性、リサイクル性、耐汚染性により、信頼できる選択肢であり続けています。世界的にリサイクルが重視されているため、消費者向けパッケージング用途での価値がさらに高まっています。

地域別では、中国が2024年に227億米ドルの評価額で市場をリードし、2034年までCAGR 5.9%で拡大すると予想されます。高い国内需要と世界で最も大規模なアルミニウム生産能力を持つ中国は、依然として圧倒的な強さを誇っています。一方、米国はインフラ整備とエネルギー転換を支援する政策転換に後押しされ、安定した消費パターンを記録し続けています。しかし、両国とも複雑な世界貿易力学を操り、調達戦略を形成し、サプライチェーンの地域化を促しています。

主な市場参入企業には、Alcoa Corporation、China Hongqiao Group、Rusal、Rio Tinto、Norsk Hydro ASAなどがあります。これらの企業は、低排出技術や持続可能なアルミニウム製造への戦略的投資を通じて生産能力を向上させています。業界のリーダーたちは、急速に進化する市場で競争力を維持するため、デジタル革新、高品位合金、リサイクル事業の拡大に注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国

- 主要輸入国

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 自動車業界における軽量素材の需要の高まり

- 持続可能なインフラに向けた政府の取り組み

- 航空宇宙・防衛部門の成長

- 家電製品の需要拡大

- 業界の潜在的リスク&課題

- 原材料価格の変動

- アルミニウム生産の環境影響

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 平板ロールシート

- コイルシート

- クラッドシート

- 陽極酸化シート

- 柄物シーツ

- 波形シート

- 穴あきシート

第6章 市場推計・予測:グレード/合金種類別、2021-2034

- 主要動向

- 1xxxシリーズ

- 2xxxシリーズ

- 3xxxシリーズ

- 5xxxシリーズ

- 6xxxシリーズ

- 7xxxシリーズ

- 8xxxシリーズ

第7章 市場推計・予測:加工方法別、2021-2034

- 主要動向

- 冷間圧延

- 熱間圧延

- 常用鋳造

- ダイレクトチル(DC)鋳造

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 自動車

- 建築・建設

- 航空宇宙

- 電気・電子工学

- 食品・飲料

- 機械・装置

- 耐久消費財

- その他

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Alcoa Corporation

- Novelis Inc.

- Arconic Corporation

- Kaiser Aluminum

- Hindalco Industries

- Constellium SE

- UACJ Corporation

- Norsk Hydro ASA

- JW Aluminum

- Aleris Corporation

- Hindalco Industries Ltd.

- BALCO(Bharat Aluminium)

- China Hongqiao Group

The Global Aluminum Sheets And Coils Market was valued at USD 52.4 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 93 billion by 2034. This growth stems largely from the ongoing rise in industrial productivity and the increasing preference for sustainable materials. Aluminum's lightweight properties make it ideal for sectors aiming to improve energy efficiency and reduce emissions. As industries embrace electrification and advanced technologies, aluminum is becoming more integral due to its ability to contribute to lower product weight without compromising strength. The accelerating shift toward cleaner energy and transportation, especially the rising demand for electric mobility, is also fueling market expansion. Alongside this, evolving manufacturing techniques, such as automation and digitalization, are enabling faster, more precise production to match growing global demand. These efficiencies are critical as producers race to meet the needs of industries prioritizing lightweight, durable, and recyclable materials. The market is also shaped by fierce competition and the increasing push for low-emission production solutions across regions, reinforcing the need for cost-effective, high-performance aluminum solutions that align with global sustainability goals.

Flat rolled aluminum sheets and coils commanded a market size of USD 16.6 billion in 2024 and are expected to grow at a CAGR of 5.7% from 2025 to 2034. Their adaptability and economic feasibility make them a top choice across core industries, especially where durability, flexibility, and lightweight characteristics are valued for mass production. These materials are commonly favored due to their ease of handling and compatibility with multiple manufacturing processes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $52.4 Billion |

| Forecast Value | $93 Billion |

| CAGR | 6% |

Clad and anodized sheets continue to attract interest for applications requiring corrosion resistance, visual appeal, and surface durability. These aluminum variants are preferred in precision-demanding sectors and are prompting innovation in coating technologies and alloy compositions to improve surface integrity. Their increased adoption is intensifying competition in specialized product categories.

Textured variants like patterned, corrugated, and perforated aluminum sheets find relevance in aesthetic and industrial applications, reflecting a trend towards functional design that also enhances performance and structure. These types are gaining attention for their versatility in structural reinforcement and architectural detailing.

Among alloy types, the 3xxx series reached a valuation of USD 14.7 billion in 2024 and is forecasted to grow at a CAGR of 6.1% through 2034. This series, along with the 1xxx group, dominates market share due to its corrosion resistance, electrical conductivity, and cost-effectiveness. These grades are especially popular in sectors where functional performance and affordability are key factors, and producers are focused on maintaining high output efficiency and consistent quality while keeping costs competitive.

Meanwhile, the 5xxx and 6xxx series continue to find steady demand in sectors requiring high-strength, weldable aluminum, notably in infrastructure and heavy-duty applications. Higher-grade aluminum from the 2xxx, 7xxx, and 8xxx series fulfills the need for performance in technologically advanced markets, where durability and precision are crucial.

In terms of processing methods, the cold rolled aluminum segment held a market value of USD 17.6 billion in 2024 and is anticipated to grow at a CAGR of 6.4% through 2034. This category benefits from superior surface finish, tight tolerances, and enhanced mechanical properties, contributing to its extensive use across critical applications. While hot rolled variants are less precise, they are often chosen for their strength and reliability in demanding environments.

Aluminum sheets and coils used in the automotive sector accounted for USD 12.6 billion in 2024, representing a 24% market share and are poised to grow at 6.1% CAGR through the forecast period. These materials are integral in modern vehicle design, particularly for reducing vehicle weight and achieving better fuel efficiency. Their application spans structural components and energy storage systems, as manufacturers continue to incorporate more aluminum into mainstream vehicle architecture.

The building and construction industry also contributes significantly to demand, leveraging aluminum's resilience, light weight, and aesthetic properties for structural, roofing, and insulation needs. In packaging and electronics, aluminum remains a reliable choice due to its safety, recyclability, and resistance to contamination. The global emphasis on recycling further enhances its value in consumer packaging applications.

In regional terms, China led the market with a valuation of USD 22.7 billion in 2024, and it is expected to expand at a CAGR of 5.9% through 2034. With high domestic demand and the world's most extensive aluminum production capacity, China remains a dominant force. Meanwhile, the United States continues to register stable consumption patterns, bolstered by policy shifts supporting infrastructure development and energy transformation. However, both nations navigate complex global trade dynamics, which are shaping sourcing strategies and encouraging localized supply chains.

Major market participants include Alcoa Corporation, China Hongqiao Group, Rusal, Rio Tinto, and Norsk Hydro ASA. These companies are advancing production capabilities through low-emission technologies and strategic investments in sustainable aluminum manufacturing. Industry leaders are focusing on digital innovation, high-grade alloys, and expanding recycling operations to remain competitive in a rapidly evolving market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising demand for lightweight materials in automotive industry

- 3.7.1.2 Government initiatives for sustainable infrastructure

- 3.7.1.3 Growth in aerospace and defense sector

- 3.7.1.4 Expanding demand in consumer electronics

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Fluctuating raw material prices

- 3.7.2.2 Environmental impact of aluminum production

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 Pestel analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Flat rolled sheets

- 5.3 Coiled sheets

- 5.4 Clad sheets

- 5.5 Anodized sheets

- 5.6 Patterned sheets

- 5.7 Corrugated sheets

- 5.8 Perforated sheets

Chapter 6 Market Estimates & Forecast, By Grade/Alloy Type, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 1xxx series

- 6.3 2xxx series

- 6.4 3xxx series

- 6.5 5xxx series

- 6.6 6xxx series

- 6.7 7xxx series

- 6.8 8xxx series

Chapter 7 Market Estimates & Forecast, By Processing Method, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Cold rolled

- 7.3 Hot rolled

- 7.4 Continuous casting

- 7.5 Direct chill (DC) casting

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Building & construction

- 8.4 Aerospace

- 8.5 Electrical & electronics

- 8.6 Food & beverage

- 8.7 Machinery & equipment

- 8.8 Consumer durables

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alcoa Corporation

- 10.2 Novelis Inc.

- 10.3 Arconic Corporation

- 10.4 Kaiser Aluminum

- 10.5 Hindalco Industries

- 10.6 Constellium SE

- 10.7 UACJ Corporation

- 10.8 Norsk Hydro ASA

- 10.9 JW Aluminum

- 10.10 Aleris Corporation

- 10.11 Hindalco Industries Ltd.

- 10.12 BALCO (Bharat Aluminium)

- 10.13 China Hongqiao Group