フォトニック集積回路の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Photonic Integrated Circuit (PIC) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740880

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

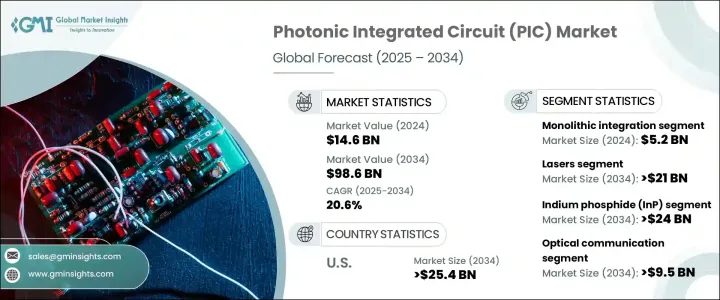

世界のフォトニック集積回路市場は、2024年に146億米ドルと評価され、CAGR 20.6%で成長し、2034年には986億米ドルに達すると推定されています。

人工知能(AI)および機械学習(ML)アプリケーションの爆発的な成長、特にデータセンター全体が市場拡大に拍車をかけ続けています。高性能コンピューティングの需要は新たな高みへと急上昇しており、従来の電子部品の限界が露呈しています。優れた帯域幅とエネルギー効率を提供するフォトニック集積回路は、こうした次世代コンピューティング要件に対応する理想的なソリューションとして浮上しています。世界中の政府、ハイテク企業、研究機関は、フォトニクスの研究開発への投資を強化しており、この技術が産業全体に果たす変革的役割を認識しています。

通信などの分野では、フォトニクスはより高速なデータ伝送を可能にし、超効率的なネットワークシステムの基盤を構築しています。ヘルスケアでは、イメージングと診断におけるフォトニクスベースのイノベーションが、患者ケアと臨床ワークフローを再構築しています。5Gネットワーク、量子コンピューティング、自律走行車、光センシングへの注目の高まりは、市場の応用分野をさらに広げ、フォトニックイノベーションへの世界の後押しを強めています。産業界がより高速で信頼性が高く、エネルギー効率の高いシステムを目指す中、PICは技術進化の中心に位置付けられ、企業や消費者の新たな可能性を引き出しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 146億米ドル |

| 予測金額 | 986億米ドル |

| CAGR | 20.6% |

フォトニック集積回路市場は、集積タイプ別にモノリシック、ハイブリッド、モジュール集積に区分されます。モノリシック集積は、2024年に52億米ドルと評価されており、リン化インジウム(InP)のような単一基板上にすべてのフォトニックコンポーネントを集積できるようにすることで、業界の主要な進歩を牽引しています。このアプローチにより、相互接続損失が大幅に削減され、システム全体の性能が向上し、製造コストが削減されます。モノリシックPICは、特に高速トランシーバーや光プロセッサーに不可欠であり、通信やデータ通信などの業界が求めるコンパクトでスケーラブルなソリューションを提供します。効率的な生産、最小限のスペース要件、信頼性の高い高速性能が重視されるようになっていることから、モノリシック集積は予測期間を通じて力強い勢いを維持すると予想されます。

コンポーネント別では、変調器、レーザー、光検出器、マルチプレクサ/デマルチプレクサ、導波路、減衰器、光増幅器、その他の重要部品が含まれます。中でもレーザーは極めて重要な役割を担っており、2034年までに210億米ドルの売上が見込まれています。InPベースのレーザは、高速光通信、光ファイバ、LIDARシステムに必要不可欠なコヒーレント光源を提供し、フォトニック集積回路に不可欠なものとなりつつあります。そのシームレスな統合能力はシステムの拡張性と性能を高め、産業界が広帯域幅アプリケーションの需要増に対応するのに役立っています。

米国のフォトニック集積回路市場は2034年までに254億米ドルに達する勢いであり、技術大手による強力なエコシステム、研究イニシアティブ、シリコンフォトニクスへの深い投資が原動力となっています。インテル、シスコ、ロックレー・フォトニクスのような企業は、光通信、データセンター、医療診断の分野で技術革新を主導しています。National Photonics Initiative(NPI)のようなイニシアチブは、防衛、航空宇宙、バイオメディカルアプリケーションのような重要な分野での商業化の努力をさらに加速させています。

世界のフォトニック集積回路業界の大手企業には、Intel Corporation、Cisco Systems, Inc.、Infinera Corporation、Broadcom Inc.などがあります。市場での存在感を高めるため、これらの企業は製品ポートフォリオを拡大し、ハイテク企業や研究機関と戦略的パートナーシップを結び、AIや通信ネットワークにおけるフォトニクスの性能を押し上げるためにRandDに多額の投資を行っています。また、イノベーションを迅速に進め、新興市場での競争力を確保するために、フォトニクス技術に特化した中小企業を買収するケースも多いです。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- データセンターの拡張と高速通信の需要

- シリコンフォトニクスの進歩

- ヘルスケアとバイオセンシングでの使用増加

- 5Gおよび次世代通信インフラの需要

- フォトニクス研究開発に対する政府および防衛機関の資金提供

- 業界の潜在的リスク&課題

- 初期資本投資が高く、製造が複雑

- PICプラットフォーム間の標準化の欠如

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:統合タイプ別、2021-2034

- モノリシック統合

- ハイブリッド統合

- モジュール統合

第6章 市場推計・予測:コンポーネント別、2021-2034

- レーザー

- 変調器

- 光検出器

- 導波管

- マルチプレクサ/デマルチプレクサ

- 減衰器

- 光増幅器

- その他

第7章 市場推計・予測:材料別、2021-2034

- リン化インジウム(InP)

- シリコンオンインシュレータ(SOI)

- シリコンフォトニクス

- ガリウムヒ素(GaAs)

- ニオブ酸リチウム

- その他

第8章 市場推計・予測:用途別、2021-2034

- 光通信

- センシング

- バイオフォトニクス

- 光信号処理

- 量子コンピューティング

- その他

第9章 市場推計・予測:最終用途別、2021-2034

- 通信

- データセンター

- 家電

- ヘルスケアとライフサイエンス

- 防衛・航空宇宙

- 産業

- 自動車

- その他

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- Intel Corporation

- Infinera Corporation

- Cisco Systems、Inc.

- Broadcom Inc.

- NeoPhotonics Corporation

- Lumentum Holdings Inc.

- II-VI Incorporated

- Coherent Corp.

- Acacia Communications

- Enablence Technologies Inc.

- HPE

- Mellanox Technologies

- Luxtera

- Rockley Photonics

- POET Technologies Inc.

- Ciena Corporation

- Alcatel-Lucent

- Fujitsu Optical Components

- IBM Corporation

- STMicroelectronics

- Hewlett Packard Labs

- TE Connectivity

- VLC Photonics(a Hitachi Group company)

- Effect Photonics

目次

The Global Photonic Integrated Circuit Market was valued at USD 14.6 billion in 2024 and is estimated to grow at a CAGR of 20.6% to reach USD 98.6 billion by 2034. The explosive growth of artificial intelligence (AI) and machine learning (ML) applications, especially across data centers, continues to fuel market expansion. High-performance computing demands have surged to new heights, exposing the limitations of traditional electronic components. Photonic circuits, offering superior bandwidth and energy efficiency, have emerged as the ideal solution to address these next-generation computing requirements. Governments, tech companies, and research institutions worldwide are ramping up investments in photonics research and development, recognizing the transformative role this technology will play across industries.

In sectors like telecommunications, photonics is enabling faster data transmission and building the foundation for ultra-efficient networking systems. In healthcare, photonics-based innovations in imaging and diagnostics are reshaping patient care and clinical workflows. The growing focus on 5G networks, quantum computing, autonomous vehicles, and optical sensing is further broadening the market's application landscape, strengthening the global push toward photonic innovation. As industries aim for faster, more reliable, and energy-efficient systems, PICs are positioned at the heart of technological evolution, unlocking new possibilities for businesses and consumers alike.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.6 billion |

| Forecast Value | $98.6 billion |

| CAGR | 20.6% |

The photonic integrated circuit market is segmented by integration type into monolithic, hybrid, and module integration. Monolithic integration, valued at USD 5.2 billion in 2024, is driving major industry advancements by enabling the integration of all photonic components onto a single substrate like Indium Phosphide (InP). This approach drastically reduces interconnect losses, boosts overall system performance, and lowers production costs. Monolithic PICs are especially crucial for high-speed transceivers and optical processors, delivering the compact, scalable solutions demanded by industries such as telecommunications and data communications. With the growing emphasis on efficient production, minimal space requirements, and reliable high-speed performance, monolithic integration is expected to maintain strong momentum through the forecast period.

Component-wise, the market includes modulators, lasers, photodetectors, multiplexers/demultiplexers, waveguides, attenuators, optical amplifiers, and other critical parts. Among these, lasers play a pivotal role and are expected to generate USD 21 billion by 2034. Lasers based on InP are becoming indispensable across photonic integrated circuits, offering essential coherent light sources needed for high-speed optical communications, fiber optics, and LIDAR systems. Their seamless integration capabilities enhance system scalability and performance, helping industries meet the increasing demand for high-bandwidth applications.

The U.S. photonic integrated circuit market is on track to reach USD 25.4 billion by 2034, powered by a strong ecosystem of technology giants, research initiatives, and deep investments in silicon photonics. Companies like Intel, Cisco, and Rockley Photonics are leading innovations across optical communication, data centers, and healthcare diagnostics. Initiatives like the National Photonics Initiative (NPI) are further accelerating commercialization efforts in critical sectors such as defense, aerospace, and biomedical applications.

Leading players in the global photonic integrated circuit industry include Intel Corporation, Cisco Systems, Inc., Infinera Corporation, and Broadcom Inc. To strengthen their market presence, these companies are expanding product portfolios, forming strategic partnerships with tech firms and research bodies, and investing heavily in RandD to push photonics performance in AI and telecom networks. Many are also acquiring smaller, specialized photonic technology firms to fast-track innovation and secure a competitive edge in emerging markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Data center expansion & high speed communication demand

- 3.3.1.2 Advancements in silicon photonics

- 3.3.1.3 Growing use in healthcare & biosensing

- 3.3.1.4 Demand for 5g & next-gen telecom infrastructure

- 3.3.1.5 Government & defense funding for photonics R&D

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High initial capital investment & fabrication complexity

- 3.3.2.2 Lack of standardization across PIC platforms

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Integration Type, 2021 - 2034 (USD Million and Units)

- 5.1 Monolithic integration

- 5.2 Hybrid integration

- 5.3 Module integration

Chapter 6 Market estimates & forecast, By Component, 2021 - 2034 (USD Million and Units)

- 6.1 Lasers

- 6.2 Modulators

- 6.3 Photodetectors

- 6.4 Waveguides

- 6.5 Multiplexers/demultiplexers

- 6.6 Attenuators

- 6.7 Optical amplifiers

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034 (USD Million and Units)

- 7.1 Indium phosphide (InP)

- 7.2 Silicon-on-insulator (SOI)

- 7.3 Silicon photonics

- 7.4 Gallium arsenide (GaAs)

- 7.5 Lithium niobate

- 7.6 Others

Chapter 8 Market estimates & forecast, By Application, 2021 - 2034 (USD Million and Units)

- 8.1 Optical communication

- 8.2 Sensing

- 8.3 Biophotonics

- 8.4 Optical signal processing

- 8.5 Quantum computing

- 8.6 Others

Chapter 9 Market estimates & forecast, By End Use, 2021 - 2034 (USD Million and Units)

- 9.1 Telecommunications

- 9.2 Data centers

- 9.3 Consumer electronics

- 9.4 Healthcare & life sciences

- 9.5 Defense & aerospace

- 9.6 Industrial

- 9.7 Automotive

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million and Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Intel Corporation

- 11.2 Infinera Corporation

- 11.3 Cisco Systems, Inc.

- 11.4 Broadcom Inc.

- 11.5 NeoPhotonics Corporation

- 11.6 Lumentum Holdings Inc.

- 11.7 II-VI Incorporated

- 11.8 Coherent Corp.

- 11.9 Acacia Communications

- 11.10 Enablence Technologies Inc.

- 11.11 HPE

- 11.12 Mellanox Technologies

- 11.13 Luxtera

- 11.14 Rockley Photonics

- 11.15 POET Technologies Inc.

- 11.16 Ciena Corporation

- 11.17 Alcatel-Lucent

- 11.18 Fujitsu Optical Components

- 11.19 IBM Corporation

- 11.20 STMicroelectronics

- 11.21 Hewlett Packard Labs

- 11.22 TE Connectivity

- 11.23 VLC Photonics (a Hitachi Group company)

- 11.24 Effect Photonics

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日