陸上地球物理学サービスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Land Based Geophysical Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740876

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

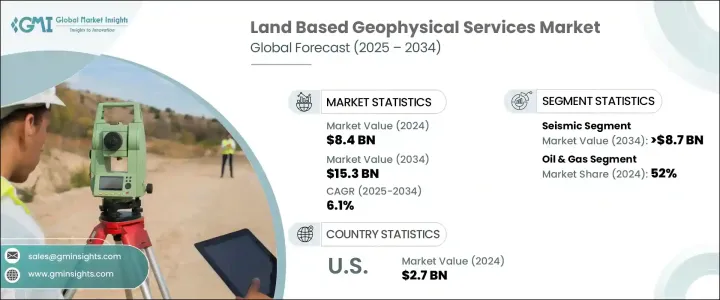

世界の陸上地球物理学サービス市場は、2024年に84億米ドルと評価され、急速な都市化、活況を呈する建設活動、精密な地下データに対する需要の急増を背景に、CAGR 6.1%で成長し、2034年には153億米ドルに達すると予測されています。

世界の都市が拡大し近代化するにつれ、安全で弾力性のあるインフラの必要性が高まっています。建設業者、開発業者、都市計画担当者は、大規模プロジェクトを立ち上げる前に、地下のユーティリティをマッピングし、地盤の安定性を評価し、地震リスクを軽減するために、ますます高度な地球物理学技術に頼るようになっています。陸上地球物理学サービスの役割は、補助的な機能から、計画、エンジニアリング、リスク管理戦略の中核的要素へと変化しています。

環境問題への関心の高まり、規制枠組みの強化、災害に強いインフラの緊急ニーズが、市場の需要をさらに押し上げています。技術革新も業界を再構築しており、利害関係者は、より迅速で安全かつ正確な結果を提供する、リアルタイムの非侵襲的調査方法を求めています。新興経済諸国が都市開発や資源探査プロジェクトを活発化させる中、費用対効果が高く、環境に配慮した地球物理学サービスへの需要が加速しています。企業は、スピード、持続可能性、精度を優先する進化する市場で競争力を維持するため、AI統合ソリューション、モバイル測量ユニット、リモートセンシングプラットフォームに多額の投資を行っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 84億米ドル |

| 予測金額 | 153億米ドル |

| CAGR | 6.1% |

世界各国の政府は、災害に強いインフラや災害軽減への投資を強化しており、先進的な陸上地球物理学サービスへの一貫した需要を後押ししています。今日の顧客は、環境を破壊することなく正確な洞察を提供する、よりスマートな調査技術を期待しています。新興地域では、従来の土地探査手法が運用コストや環境上の課題からますます実行不可能になり、革新的な地球物理学的ソリューションの機会が生まれています。プレーヤーは、より良い意思決定のためのリアルタイムデータを提供しながら、進化する安全性と持続可能性の基準を満たすAIを搭載したプラットフォームで対応しています。

環境保全は極めて重要な要素になりつつあり、利害関係者は土地の埋め立て、資源採掘、環境浄化プロジェクトにおいて、非侵襲的で環境に優しい測量方法を好むようになっています。開発途上地域では、操業上のハードルと高い探査コストが、効率的な鉱物・エネルギー資源探査に物理探査サービスを魅力的な選択肢にしています。政府の貿易政策の変化も機器の調達やサービスモデルに影響を与えており、プロバイダーはコスト効率に優れた技術主導の戦略を採用する必要に迫られています。リアルタイムで高精度の地下洞察の必要性は、業界が探査と開発に取り組む方法の根本的な転換を促しています。

地震探査分野は、イメージング解像度の向上とタイムラプス地震探査技術の利用拡大に支えられ、2034年までに87億米ドルに達すると予想されています。地震探査サービスは、炭化水素探査に不可欠な高解像度の地下データのゴールドスタンダードであり続けています。磁気探査と電磁気探査は、特に正確な地質図作成が不可欠な、到達困難な採掘地域で人気を集めています。

石油・ガスセクターは、2024年の最終用途セグメントで52%のシェアを占め、重力・磁気探査が掘削コストの削減と探査成果の向上に重要な役割を果たし続けています。エレクトロニクスや再生可能エネルギー産業で必要とされる重要鉱物の需要増も、鉱業用途での地球物理学サービスの採用拡大に拍車をかけています。

米国の陸上地球物理学サービス市場は2024年に27億米ドルとなり、大規模なインフラ投資と持続可能で電化された操業を促進する規制上のインセンティブが原動力となっています。地震屈折法と地中レーダー技術は、地下ユーティリティのマッピングと建設の安全に広く利用されています。カナダでは、非侵襲的で環境に配慮した調査手法の推進も、特に天然資源評価と環境埋め立てのために浸透しつつあります。

競合情勢を形成している主な企業は、CGG、フグロ、SLB、Getech Group、Abitibi Geophysics、Weatherford、TGS、PGS、Gardline、Ramboll Group、Dawson Geophysical Company、SAExploration、Spectrum Geophysicsなどです。各社はリアルタイムデータ分析、AI統合、新興市場への進出に注力し、その地位を強化しています。持続可能な調査手法への投資とともに、エネルギー・鉱業部門との戦略的提携が成長戦略の中核になりつつあります。モバイル調査ユニットとリモートセンシング技術の革新は、精度とスピードが求められる市場において主要な差別化要因として浮上しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:技術別、2021-2034

- 主要動向

- 地震

- 磁気

- 電磁

- 勾配法

- その他

第6章 市場規模・予測:最終用途別、2021-2034

- 主要動向

- 石油・ガス

- 鉱業

- 農業

- その他

第7章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ノルウェー

- ロシア

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- イラク

- イラン

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- Abitibi Geophysics

- CGG

- Dawson Geophysical Company

- Fugro

- Gardline

- Getech Group

- PGS

- Ramboll Group

- SAExploration

- SLB

- Spectrum Geophysics

- TGS

- Weatherford

目次

The Global Land Based Geophysical Services Market was valued at USD 8.4 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 15.3 billion by 2034, driven by rapid urbanization, booming construction activities, and surging demand for precise subsurface data. As cities worldwide expand and modernize, the need for safe, resilient infrastructure is intensifying. Builders, developers, and urban planners are increasingly relying on advanced geophysical technologies to map underground utilities, assess ground stability, and mitigate seismic risks before launching large-scale projects. The role of land based geophysical services has shifted from a supportive function to a core element of planning, engineering, and risk management strategies.

Rising environmental concerns, tighter regulatory frameworks, and the urgent need for disaster-resilient infrastructure are further boosting market demand. Technological innovation is also reshaping the industry, with stakeholders seeking real-time, non-invasive survey methods that provide faster, safer, and more accurate results. As emerging economies ramp up urban development and resource exploration projects, the appetite for cost-effective and eco-conscious geophysical services is accelerating. Companies are investing heavily in AI-integrated solutions, mobile survey units, and remote sensing platforms to stay competitive in an evolving market that prioritizes speed, sustainability, and precision.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.4 Billion |

| Forecast Value | $15.3 Billion |

| CAGR | 6.1% |

Governments worldwide are stepping up investments in resilient infrastructure and disaster mitigation, helping fuel consistent demand for advanced land based geophysical services. Customers today expect smarter survey technologies that deliver accurate insights without disrupting the environment. In emerging regions, traditional land exploration methods are increasingly unviable due to operational costs and environmental challenges, creating opportunities for innovative geophysical solutions. Players are responding with AI-powered platforms that meet evolving safety and sustainability standards while delivering real-time data for better decision-making.

Environmental stewardship is becoming a crucial factor, pushing stakeholders to prefer non-invasive, eco-friendly surveying methods for land reclamation, resource extraction, and environmental cleanup projects. In developing regions, operational hurdles and high exploration costs make geophysical services an attractive option for efficient mineral and energy resource identification. Shifts in government trade policies are also impacting equipment sourcing and service models, pushing providers to adopt cost-efficient, technology-driven strategies. The need for real-time, high-precision subsurface insights is driving a fundamental shift in how the industry approaches exploration and development.

The seismic segment is expected to reach USD 8.7 billion by 2034, supported by advancements in imaging resolution and the growing use of time-lapse seismic technologies. Seismic services remain the gold standard for high-definition subsurface data, critical to hydrocarbon exploration. Magnetic and electromagnetic surveys are gaining traction, especially in hard-to-reach mining areas where accurate geological mapping is essential.

The oil and gas sector dominated the end-use segment with a 52% share in 2024, where gravity and magnetic surveys continue to play a vital role in reducing drilling costs and improving exploration outcomes. Rising demand for critical minerals needed in electronics and renewable energy industries is also fueling greater adoption of geophysical services in mining applications.

The U.S. Land Based Geophysical Services Market stood at USD 2.7 billion in 2024, powered by major infrastructure investments and regulatory incentives promoting sustainable and electrified operations. Seismic refraction and ground-penetrating radar technologies are widely used for underground utility mapping and construction safety. In Canada, the push for non-invasive, environmentally sensitive survey methods is also gaining ground, particularly for natural resource assessment and environmental reclamation.

Key players defining the competitive landscape include CGG, Fugro, SLB, Getech Group, Abitibi Geophysics, Weatherford, TGS, PGS, Gardline, Ramboll Group, Dawson Geophysical Company, SAExploration, and Spectrum Geophysics. Companies are focusing on real-time data analytics, AI integration, and expanding into emerging markets to strengthen their positions. Strategic partnerships with energy and mining sectors, along with investments in sustainable survey methods, are becoming core growth strategies. Innovation in mobile survey units and remote sensing technologies is emerging as a major differentiator in a market driven by precision and speed.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 - 2034, (USD Million)

- 5.1 Key trends

- 5.2 Seismic

- 5.3 Magnetic

- 5.4 Electromagnetic

- 5.5 Gradiometric

- 5.6 Others

Chapter 6 Market Size and Forecast, By End Use, 2021 - 2034, (USD Million)

- 6.1 Key trends

- 6.2 Oil & gas

- 6.3 Mining

- 6.4 Agriculture

- 6.5 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034, (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Norway

- 7.3.5 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.5 Middle East & Africa

- 7.5.1 UAE

- 7.5.2 Saudi Arabia

- 7.5.3 Iraq

- 7.5.4 Iran

- 7.5.5 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Abitibi Geophysics

- 8.2 CGG

- 8.3 Dawson Geophysical Company

- 8.4 Fugro

- 8.5 Gardline

- 8.6 Getech Group

- 8.7 PGS

- 8.8 Ramboll Group

- 8.9 SAExploration

- 8.10 SLB

- 8.11 Spectrum Geophysics

- 8.12 TGS

- 8.13 Weatherford

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日