|

市場調査レポート

商品コード

1740860

除雪車の市場機会、成長促進要因、産業動向分析、2025~2034年予測Snow Clearing Vehicles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 除雪車の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月30日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

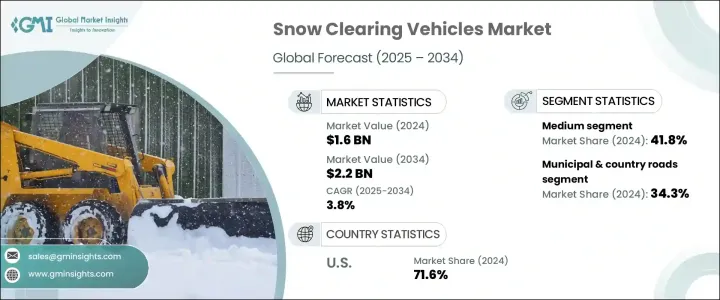

除雪車の世界市場規模は、2024年に16億米ドルとなり、CAGR 3.8%で成長し、2034年には22億米ドルに達すると予測されています。

この成長は、空港インフラの継続的な開発と、豪雪に見舞われやすい様々な地域の道路交通網の着実な増加が大きな要因となっています。空港のアップグレードと拡張に伴い、特に寒冷地では高性能除雪車両の需要が伸び続けています。効率的な除雪機器は、厳しい冬の状況下で中断のないサービスを維持するために不可欠です。市場はまた、スマート・インフラストラクチャーへの幅広いシフトも見ており、自治体やサービス・プロバイダーは、安全性と効率の両方を高める高度で信頼性の高い除雪技術を優先しています。持続可能性、燃料効率、低メンテナンス・ソリューションへの注目の高まりは、都市と農村の両方における除雪作業の管理方法に変化をもたらしています。

用途別では、市場セグメンテーションは空港、高速道路、市道・国道、その他の用途の4つの主要セグメントに分けられます。2024年には、市町村および田舎道セグメントが約34.3%の市場シェアでトップに立ち、予測期間を通じてCAGR 3.5%以上で成長すると予測されています。このセグメントは、地域特有の条件に合わせて除雪技術を適応させ、規模を拡大する能力があるため、極めて重要です。地方自治体は、耐腐食性部品、モジュラーシステム、高度な除氷技術を備えた多機能車両に頻繁に投資しています。これらのカスタマイズは、遠隔地やアクセスが困難な地域、または悪天候の影響を頻繁に受ける地域であっても、一貫したパフォーマンスを提供するのに役立ちます。自治体の路線や田舎道の除雪作業では、険しい地形、未舗装の路面、狭い道などを移動することがよくあります。このため、過酷な環境条件下での激しい作業にも対応できる、多関節ブレード、強化サスペンション、全地形対応タイヤなどの頑丈なハードウェアを備えた車両の需要が高まっています。市や町がよりスマートな雪管理方法を採用するにつれ、持続可能性と効果の両方を向上させるために、GPSガイド付き除雪システム、自動塩撒き機能、ハイブリッド推進オプションを備えた機器への関心が高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 16億米ドル |

| 予測金額 | 22億米ドル |

| CAGR | 3.8% |

市場はまた、車種別に小型車、中型車、大型車に区分されます。中型車セグメントは2024年に市場の約41.8%を占めて最大となり、2034年までのCAGRは4.3%以上で成長すると予測されます。これらの車両は、特に都市部や大規模な商業地区での除雪作業において重要な役割を果たしています。パワーとサイズのバランスにより、頻繁かつ正確な除雪が必要な環境でも効率的に作動します。多くのモデルが用意されているこれらの車両は、購入者が地形、降雪レベル、必要な操縦性に基づいて機器を選択できるようになっています。購入者は、オプションの機能やアタッチメントを含む価格の透明性が高まったことで、自治体や請負業者が限られた予算の中で賢く投資しやすくなりました。

推進力タイプ別に分類すると、市場には内燃機関車(ICE)、電気自動車、ハイブリッド車が含まれます。ICE機関車は、高トルク、一貫した信頼性、凍結や険しい条件下での長い運転耐久性を提供する能力が実証されているため、2024年においても支配的な選択肢であり続ける。これらの車両は、除雪車や散布機のような重量のある除雪機器を運転する際の性能で、オペレーターに支持されています。ICEベースのシステムが依然として最も一般的であるが、進化する性能・環境基準を満たすため、最新の燃料管理システム、低排出ガス技術、ナビゲーション機能で強化する方向に徐々にシフトしています。

地域別では、米国が2024年の除雪車市場をリードし、約5億米ドルを生み出し、北米全体のシェアの約71.6%を占めています。同国の多様な冬の気候と、積雪時の交通安全の維持に重点が置かれていることが、除雪ソリューションに対する一貫した強い需要を生み出しています。確立されたサプライチェーンと継続的な技術の進歩により、米国は除雪車と機器の主要市場であり続けています。

業界が進化し続ける中、メーカーは除雪車の素材や技術を改良した設計に力を入れています。強化された油圧、耐腐食性の表面、高トルクの駆動システムが標準になりつつあります。これらのアップデートは、車両の寿命を延ばすだけでなく、厳しい冬期作業においてトップクラスの性能を保証します。硬化鋼、軽量合金、高度な複合材などの高性能コンポーネントは、極端な天候や厳しい環境下での操縦性を高め、燃料消費量を削減し、構造耐久性を向上させるために、ますます統合されつつあります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料サプライヤー

- 部品サプライヤー

- 製造業者

- テクノロジープロバイダー

- サービスプロバイダー

- 流通チャネル

- 最終用途

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(顧客へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 価格分析

- 推進

- 地域

- 影響要因

- 促進要因

- 異常気象の頻度の増加

- 空港インフラの拡張

- 都市化と自治体の投資

- 道路輸送網の成長

- 業界の潜在的リスク&課題

- 高い資本コストと維持費

- 環境規制と燃費基準

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:用途別、2021-2034

- 主要動向

- 空港

- 高速道路

- 市街地道路と田舎道

- その他

第6章 市場推計・予測:車両別、2021-2034

- 主要動向

- コンパクト

- 中

- 重い

第7章 市場推計・予測:推進力別、2021-2034

- 主要動向

- ICE

- 電気

- ハイブリッド

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 政府および地方自治体

- 民間請負業者

- 農業部門

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Aebi Schmidt Holding

- Alamo

- Boschung Holding

- Caterpillar

- Daimler(Mercedes-Benz Trucks)

- Doosan Bobcat

- Faymonville

- Hako Group

- John Deere

- Kassbohrer Gelandefahrzeug

- Kodiak America

- M-B Companies

- Montana Manufacturing

- Oshkosh

- Rosenbauer International

- Schmidt Group

- Swarco

- Ventrac

- Wausau Equipment Company

- Zoomlion

The Global Snow Clearing Vehicles Market was valued at USD 1.6 billion in 2024 and is estimated to grow at a CAGR of 3.8% to reach USD 2.2 billion by 2034. This growth is largely fueled by the ongoing development of airport infrastructure and the steady rise in road transportation networks across various regions prone to heavy snowfall. As airports upgrade and expand, especially in colder areas, the demand for high-performance snow removal vehicles continues to grow. Efficient snow clearing equipment is essential to maintaining uninterrupted services during severe winter conditions. The market is also seeing a broader shift toward smart infrastructure, where municipalities and service providers are prioritizing advanced and reliable snow clearing technologies that enhance both safety and efficiency. A growing focus on sustainability, fuel efficiency, and low-maintenance solutions is transforming how snow removal operations are managed in both urban and rural settings.

In terms of application, the snow clearing vehicles market is divided into four main segments: airports, highways, municipal and country roads, and other uses. In 2024, the municipal and country roads segment took the lead with an approximate 34.3% market share and is projected to grow at over 3.5% CAGR throughout the forecast period. This segment is pivotal due to its ability to adapt and scale snow clearing technologies to suit unique regional conditions. Local governments frequently invest in multi-functional vehicles equipped with corrosion-resistant parts, modular systems, and advanced de-icing technology. These customizations help deliver consistent performance even in areas that are remote, hard to reach, or frequently impacted by adverse weather. Clearing snow from municipal routes and country roads often involves navigating steep terrain, unpaved surfaces, and narrow paths. This has led to a growing demand for vehicles built with rugged hardware like articulated blades, reinforced suspensions, and all-terrain tires that can handle intense workloads under harsh environmental conditions. As cities and towns adopt smarter snow management practices, there is a growing interest in equipment with GPS-guided plow systems, automated salting features, and hybrid propulsion options to improve both sustainability and effectiveness.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 3.8% |

The market is also segmented by vehicle type into compact, medium, and heavy vehicles. The medium vehicle segment emerged as the largest in 2024, accounting for approximately 41.8% of the market, and is expected to grow at a CAGR of over 4.3% through 2034. These vehicles play a critical role in snow clearing operations, particularly in urban areas and large commercial zones. Their balance of power and size allows them to operate efficiently in environments that require frequent and precise snow removal. Available in numerous models, these vehicles allow purchasers to select equipment based on terrain, snowfall levels and required maneuverability. Buyers now benefit from greater transparency in pricing, which includes optional features and attachments, making it easier for municipalities and contractors to invest wisely within limited budgets.

When classified by propulsion type, the market includes internal combustion engine (ICE), electric, and hybrid-powered vehicles. ICE vehicles remain the dominant choice in 2024 due to their proven ability to deliver high torque, consistent reliability, and long operational endurance in freezing and rugged conditions. These vehicles are favored by operators for their performance in driving heavy snow removal equipment such as plows and spreaders. Although ICE-based systems are still the most common, there's a gradual shift toward enhancing them with modern fuel management systems, low-emission technology, and navigation features to meet evolving performance and environmental standards.

Regionally, the United States led the snow clearing vehicles market in 2024, generating around USD 500 million and holding nearly 71.6% of the total share in North America. The country's diverse winter climate and emphasis on maintaining road safety during snow events have created a strong and consistent demand for snow clearing solutions. A well-established supply chain, coupled with ongoing technological advancements, has allowed the U.S. to remain a leading market for snow clearing vehicles and equipment.

As the industry continues to evolve, manufacturers are focusing on designing snow clearing vehicles with improved materials and technology. Reinforced hydraulics, corrosion-resistant surfaces, and high-torque drive systems are becoming standard. These updates not only extend vehicle life but also ensure top-tier performance in demanding winter operations. High-performance components such as hardened steel, lightweight alloys, and advanced composites are being increasingly integrated to boost maneuverability, reduce fuel consumption, and enhance structural durability in extreme weather and challenging landscapes.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component Suppliers

- 3.2.3 Manufacturers

- 3.2.4 Technology Providers

- 3.2.5 Service Providers

- 3.2.6 Distribution channel

- 3.2.7 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Pricing analysis

- 3.9.1 Propulsion

- 3.9.2 Region

- 3.10 Impact on forces

- 3.10.1 Growth drivers

- 3.10.1.1 Increasing frequency of extreme weather events

- 3.10.1.2 Expansion of airport infrastructure

- 3.10.1.3 Urbanization and municipal investments

- 3.10.1.4 Growth in road transportation networks

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High capital and maintenance costs

- 3.10.2.2 Environmental regulations and fuel efficiency standards

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Airports

- 5.3 Highways

- 5.4 Municipal & country roads

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Compact

- 6.3 Medium

- 6.4 Heavy

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Government & municipalities

- 8.3 Private contractor

- 8.4 Agricultural sector

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Aebi Schmidt Holding

- 10.2 Alamo

- 10.3 Boschung Holding

- 10.4 Caterpillar

- 10.5 Daimler (Mercedes-Benz Trucks)

- 10.6 Doosan Bobcat

- 10.7 Faymonville

- 10.8 Hako Group

- 10.9 John Deere

- 10.10 Kassbohrer Gelandefahrzeug

- 10.11 Kodiak America

- 10.12 M-B Companies

- 10.13 Montana Manufacturing

- 10.14 Oshkosh

- 10.15 Rosenbauer International

- 10.16 Schmidt Group

- 10.17 Swarco

- 10.18 Ventrac

- 10.19 Wausau Equipment Company

- 10.20 Zoomlion