|

|

市場調査レポート

商品コード

1797832

心臓マッピング市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Cardiac Mapping Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 心臓マッピング市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年07月25日

発行: Global Market Insights Inc.

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

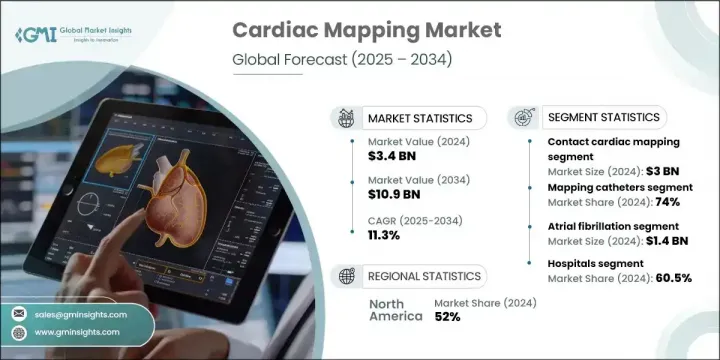

心臓マッピングの世界市場規模は、2024年に34億米ドルとなり、CAGR 11.3%で成長し、2034年には109億米ドルに達すると推定されます。

この堅調な成長の背景には、不整脈と診断される患者数の増加、マッピング技術の急速な革新、低侵襲診断手技への嗜好の高まりがあります。これらの要因に加え、電気生理学への投資の増加や、特に発展途上のヘルスケアシステムにおける心臓血管治療へのアクセスの拡大が、市場開拓を加速させています。世界中の循環器科がリアルタイムの可視化と正確なマッピングのための新しい技術を採用するにつれて、心臓マッピングツールに対する需要が急速に高まっています。病院や専門センターは、手技による合併症を減らし、患者の転帰を改善するため、精密誘導治療を重視しています。

ヘルスケアの近代化の推進は、支援的な償還の枠組みや世界の研究資金の増加と相まって、先進国、新興国を問わず、心臓マッピングテクノロジーに有望な未来を形成しています。病院が精密医療と個別化治療計画をますます優先するようになるにつれ、リアルタイムの心臓診断に対する需要が加速しています。ヘルスケアシステムは最先端の電気生理学ラボに投資しており、政府は低侵襲手技を採用するための財政的インセンティブを提供しています。同時に、公的および民間の資金提供機関は、マッピング精度の向上、手技リスクの低減、AIを搭載したマッピングプラットフォームの開発を目的とした研究にリソースを注いでいます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 34億米ドル |

| 予測金額 | 109億米ドル |

| CAGR | 11.3% |

2024年、マッピングカテーテル分野のシェアは74%。この分野は、複雑な心臓リズム障害の症例が増加していることや、低侵襲の電気生理学的処置の際に高精細な電気解剖学的データを必要とすることから、引き続き堅調です。高密度多電極カテーテルシステムは、医師が瞬時に何万ものデータポイントを収集し、比類のない詳細さと精度を提供できるため、急速にゴールドスタンダードになりつつあります。これらのマッピング・ソリューションは、より的を絞った効率的なアブレーションを促進することにより、心房細動や心室頻拍の同定と治療をサポートします。

コンタクト心臓マッピング分野は2024年に30億米ドルを生み出し、2034年までCAGR 11.6%で成長すると予測されています。これらのシステムは、心臓組織との継続的な接触を維持することにより、正確な電気的・解剖学的測定値を提供し、極めて明瞭な活性化マップと電圧マップを作成します。この詳細レベルは、しばしばピンポイントの正確さが要求される複雑な不整脈の診断や治療において特に重要です。その優れた信号品質により、コンタクトマッピングツールは臨床電気生理学で広く好まれています。さらに、電気信号をリアルタイムで追跡できる自動化された心臓マッピングシステムは、臨床医がより高い精度で問題のある組織を検出することにより、アブレーション治療の成功率を向上させながら、手技を短縮することを可能にしています。

米国の心臓マッピング市場は2024年に17億米ドルを創出。市場は2025年から2034年にかけてCAGR 10.6%で成長すると予測されています。同国は、高度に発達したヘルスケア・インフラの恩恵を受けており、電気生理学専門のラボや高度なマッピング・システムを備えた心臓センターなどがあります。主要な病院や学術研究センターでは、手技の精度と安全性を高める高度な技術を用いて、複雑なアブレーション手技を日常的に行っています。EP治療に対する良好な償還環境と幅広い保険適用が、高い手技量を支え、迅速な技術導入を促進しています。

世界の競合情勢を形成している主要企業は、Medtronic、Abbott Laboratories、Johnson &Johnson、Boston Scientific、Lepu Medical、Kardium、MicroPort Scientific、APN Health、EnChannel Medicalなどです。これらの企業は、イノベーションと戦略的イニシアティブを通じて市場の進化に積極的に貢献しています。主要な心臓マッピング企業は、技術革新、臨床提携、地理的拡大の組み合わせを通じて市場での地位を強化しています。これらの企業は、強化された電極設計と高速信号取得機能を備えた次世代カテーテルを導入するため、研究開発に多額の投資を行っています。一流病院や学術機関との提携により、先進的な電気解剖学的マッピング・プラットフォームの実地試験が可能になっています。多くの企業が、アブレーション手技中のデータ解析を改善するため、自動化とAI統合ソフトウェアに注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 心血管疾患の発生率が高め

- 心血管疾患の治療法に関する意識の高まり

- 調査と資金に対する政府の有利な政策

- 製品における技術的進歩

- 業界の潜在的リスク&課題

- 心臓マッピングシステムの高コスト

- 熟練した経験豊富な電気生理学者の不足

- 市場機会

- 小児心臓病学におけるマッピングシステムの使用増加

- 3D電気解剖マッピングの採用増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 米国

- 欧州

- テクノロジーの情勢

- 償還シナリオ

- ギャップ分析

- 製品別、世界の価格分析、2024

- マッピングシステム

- マッピングカテーテル

- ポーター分析

- PESTEL分析

- 将来の市場動向

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 地域別

- 競合ポジショニングマトリックス

- 主要市場企業の競合分析

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- マッピングカテーテル

- マッピングシステム

第6章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 接触型心臓マッピング

- 非接触型心臓マッピング

第7章 市場推計・予測:適応症別、2021年~2034年

- 主要動向

- 心房細動

- 心房粗動

- 心室頻拍

- その他の適応症

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- EPラボ

- その他の用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Abbott Laboratories

- APN Health

- Boston Scientific

- EnChannel Medical

- Johnson &Johnson

- Kardium

- Lepu Medical

- Medtronic

- MicroPort Scientific

The Global Cardiac Mapping Market was valued at USD 3.4 billion in 2024 and is estimated to grow at a CAGR of 11.3% to reach USD 10.9 billion by 2034. This robust growth is being driven by a rising number of patients diagnosed with cardiac arrhythmias, rapid innovation in mapping technologies, and increased preference for minimally invasive diagnostic procedures. Alongside these factors, growing investments in electrophysiology and expanded access to cardiovascular care-particularly in developing healthcare systems-are accelerating market development. As cardiology departments worldwide adopt new techniques for real-time visualization and accurate mapping, the demand for cardiac mapping tools is rapidly increasing. Hospitals and specialty centers are emphasizing precision-guided treatments to reduce procedural complications and improve patient outcomes.

The push toward healthcare modernization, coupled with supportive reimbursement frameworks and an uptick in global research funding, is shaping a promising future for cardiac mapping technologies across both established and emerging economies. As hospitals increasingly prioritize precision medicine and personalized treatment plans, the demand for real-time cardiac diagnostics is accelerating. Healthcare systems are investing in cutting-edge electrophysiology labs, and governments are offering financial incentives to adopt minimally invasive procedures. At the same time, public and private funding bodies are channeling resources into research aimed at improving mapping accuracy, reducing procedural risks, and developing AI-powered mapping platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.4 Billion |

| Forecast Value | $10.9 Billion |

| CAGR | 11.3% |

In 2024, the mapping catheters segment held 74% share. This segment remains strong due to growing cases of complex heart rhythm disorders and the need for high-definition electroanatomical data during minimally invasive electrophysiological procedures. High-density and multi-electrode catheter systems are rapidly becoming the gold standard as they allow physicians to collect tens of thousands of data points within moments, offering unmatched detail and accuracy. These mapping solutions support the identification and treatment of atrial fibrillation and ventricular tachycardia by facilitating more targeted and efficient ablation.

The contact cardiac mapping segment generated USD 3 billion in 2024 and is forecasted to grow at a CAGR of 11.6% through 2034. These systems provide precise electrical and anatomical readings by maintaining continuous contact with cardiac tissue, producing exceptionally clear activation and voltage maps. This level of detail is particularly crucial in diagnosing and treating complex arrhythmias that often require pinpoint accuracy. Due to their superior signal quality, contact mapping tools are widely preferred in clinical electrophysiology. Furthermore, automated cardiac mapping systems capable of tracking electrical signals in real time are enabling clinicians to shorten procedures while improving success rates in ablation therapies by detecting problematic tissue with greater accuracy.

United States Cardiac Mapping Market generated USD 1.7 billion in 2024. The market is projected to grow at a CAGR of 10.6% from 2025 to 2034. The country benefits from a highly developed healthcare infrastructure, including specialized electrophysiology labs and cardiac centers outfitted with advanced mapping systems. Leading hospitals and academic research centers routinely perform complex ablation procedures with sophisticated technologies that enhance procedural accuracy and safety. A favorable reimbursement environment and wide insurance coverage for EP treatments support high procedure volumes and facilitate quicker technology adoption.

Key players shaping the competitive landscape in the Global Cardiac Mapping Market include Medtronic, Abbott Laboratories, Johnson & Johnson, Boston Scientific, Lepu Medical, Kardium, MicroPort Scientific, APN Health, and EnChannel Medical. These companies are actively contributing to market evolution through innovation and strategic initiatives. Major cardiac mapping firms are reinforcing their market standing through a combination of innovation, clinical partnerships, and geographic expansion. These companies are investing heavily in R&D to introduce next-generation catheters with enhanced electrode designs and faster signal acquisition capabilities. Collaborations with top-tier hospitals and academic institutions are enabling real-world testing of advanced electroanatomical mapping platforms. Many players are focusing on automation and AI-integrated software to improve data analysis during ablation procedures.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Type trends

- 2.2.4 Indication trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High incidence of cardiovascular diseases

- 3.2.1.2 Rising awareness about the treatment options for cardiovascular diseases

- 3.2.1.3 Favourable government policies for research and funding

- 3.2.1.4 Technological advancements in the products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of the cardiac mapping systems

- 3.2.2.2 Lack of skilled and experienced electrophysiologists

- 3.2.3 Market opportunities

- 3.2.3.1 Growing use of mapping systems in pediatric cardiology

- 3.2.3.2 Increasing adoption of 3D electroanatomical mapping

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Gap analysis

- 3.8 Pricing analysis, by product, at global level, 2024

- 3.8.1 Mapping systems

- 3.8.2 Mapping catheters

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Future market trends

- 3.12 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 By Region

- 4.3.1.1 North America

- 4.3.1.2 Europe

- 4.3.1.3 Asia Pacific

- 4.3.1.4 Latin America

- 4.3.1.5 MEA

- 4.3.1 By Region

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Mapping catheters

- 5.3 Mapping systems

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Contact cardiac mapping

- 6.3 Non-contact cardiac mapping

Chapter 7 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Atrial fibrillation

- 7.3 Atrial flutter

- 7.4 Ventricular tachycardia

- 7.5 Other indications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 EP labs

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 APN Health

- 10.3 Boston Scientific

- 10.4 EnChannel Medical

- 10.5 Johnson & Johnson

- 10.6 Kardium

- 10.7 Lepu Medical

- 10.8 Medtronic

- 10.9 MicroPort Scientific