|

市場調査レポート

商品コード

1740855

バイオ医薬品包装市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Biopharmaceutical Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| バイオ医薬品包装市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月22日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

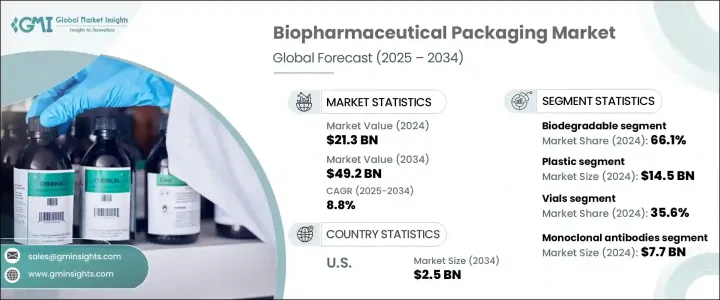

世界のバイオ医薬品包装市場は、2024年に213億米ドルと評価され、2034年にはCAGR 8.8%で成長し492億米ドルに達すると推定されています。

バイオ医薬品業界が、モノクローナル抗体、細胞・遺伝子治療、mRNAベースの医薬品など、複雑で高価値の治療法への注力を拡大し続けているため、先進パッケージング・ソリューションの重要性が急激に高まっています。バイオ医薬品は環境の変化に非常に敏感で、管理された保管・輸送条件が必要とされます。このため、サプライチェーン全体を通じて医薬品の安定性を保護するように設計された革新的な材料や技術に対する需要が急増しています。世界中の規制当局が包装の安全基準を強化する中、製薬会社は生物製剤の保護方法を再考しています。その上、より多くの生物製剤が世界市場に参入するにつれて、無菌性を確保し、リアルタイムのモニタリングを可能にし、持続可能性の目標に沿った包装形態がより強く求められています。

より革新的で堅牢なパッケージング・ソリューションへのシフトは、コールドチェーン・ロジスティクスへの投資の拡大と生物製剤の世界の消費者層の拡大によってさらに後押しされています。バイオ医薬品企業は、極端な高温に耐え、製造現場からポイント・オブ・ケア・デリバリーまで製品の有効性を維持できる高性能素材を採用することで対応しています。持続可能性を重視する傾向が強まっていることも、設計の選択に影響を与えています。ヘルスケアプロバイダーもエンドユーザーも、より安全で環境に優しい選択肢を求めているため、包装企業はリサイクル可能、生分解性、再利用可能なソリューションの開発を加速させています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 213億米ドル |

| 予測金額 | 492億米ドル |

| CAGR | 8.8% |

貿易政策の変化、特に医薬品関連の輸入品に課された報復関税は、市場力学に新たな複雑さを加えています。これらの関税は、特に国際的に調達される高品位プラスチックや医薬品用ガラスの原材料コストを引き上げています。その結果、国内での製造コストが上昇し、バリューチェーン全体の調達戦略に影響を及ぼしています。企業は現在、コンプライアンスと品質基準を維持しつつ、投入コストの上昇を相殺するために、現地に根ざしたサプライチェーンや代替調達モデルを模索しています。

同時に、テクノロジーはバイオ医薬品の包装やモニタリングのあり方を変えつつあります。特に温度に敏感な生物製剤では、スマートな包装形態がゲームチェンジャーになりつつあります。RFIDタグやセンサーと統合されたソリューションは、温度、湿度、製品の完全性といった重要なパラメーターのリアルタイム追跡を可能にしています。このようなインテリジェント・システムは、無駄を最小限に抑え、危険な製品のリスクを低減し、患者の安全性を全体的に向上させるのに役立ちます。ドラッグデリバリーや保管における精度の要求が高まり続ける中、スマート包装は、この競争の激しい業界において、贅沢品から必需品へと急速に移行しつつあります。

2024年には、生分解性包装材料が世界市場の66.1%を占め、持続可能性への決定的なシフトを示します。この動向は、消費者の環境意識の高まりへの対応だけでなく、医薬品用途における使い捨てプラスチックの段階的廃止を求める規制圧力の強化を反映しています。生分解性素材は大きく進化し、現在では医薬品用途に必要な耐久性、耐薬品性、バリア性を備えています。これらの技術革新により、生分解性包装はニッチな地位を超え、幅広い医薬品フォーマットにおいて従来のプラスチック製ソリューションに代わる競争力のある選択肢となっています。

このような変化にもかかわらず、2024年の市場規模は145億米ドルで、プラスチック包装が依然として支配的な地位を占めています。その広範な使用は、費用対効果、設計の柔軟性、優れた保護品質によって支えられています。プラスチックは特に、改ざん防止機能、高い耐湿性、チャイルドセーフ・クロージャーやシングルユースシステムのような特殊な部品との互換性を必要とする用途で好まれています。ポリマー科学の絶え間ない進歩により、プラスチックパッケージングの性能は向上し、医薬品の保管や流通におけるますます厳しくなる要求に応えることができるようになりました。

米国のバイオ医薬品包装市場は、同国の強力な医薬品製造エコシステムとバイオテクノロジーの革新に牽引され、2034年までに25億米ドルに達すると予測されています。厳しい規制基準と、安全性、完全性、持続可能性に関する消費者の期待の高まりが相まって、包装企業はより迅速な技術革新に取り組んでいます。業界がドラッグデリバリーやコンプライアンスにおける新たな課題や機会に適応していく中で、スマートでトレーサブル、かつ環境に配慮した包装形態が不可欠となっています。

Amcor、Schott AG、Gerresheimer AG、Becton, Dickinson &Co.、CCL Industriesのような企業は、先を行くために研究開発に積極的に投資しています。これらの企業は製薬会社と提携し、次世代パッケージング・ソリューションの共同開発、環境に優しい代替品の拡大、サプライチェーンの可視化と規制調整のためのデジタルツールの導入を行っています。世界市場が成熟する中、バイオ医薬品包装における戦略的イノベーションは、世界の最先端治療を安全かつ効率的に提供するための中心的存在であり続けると思われます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 持続可能で環境に優しい包装ソリューションに対する需要の高まり

- ヘルスケアインフラの世界展開と近代化

- 慢性疾患や生活習慣病の増加

- スマート包装システムなどの急速な技術革新

- バイオ医薬品と個別化医療の研究開発への投資増加

- 業界の潜在的リスク&課題

- 初期投資と運用コストが高め

- 複雑なサプライチェーン物流と厳格な品質基準

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- 生分解性

- 生分解性なし

第6章 市場推計・予測:材料別、2021-2034

- 主要動向

- プラスチック

- ポリ塩化ビニル(PVC)

- ポリプロピレン(PP)

- ポリエチレンテレフタレート(PET)

- ポリスチレン(PS)

- ポリエチレン(PE)

- HDPE

- 低密度ポリエチレン

- LLDPE

- その他

- ガラス

第7章 市場推計・予測:製品別、2021-2034

- 主要動向

- バイアル

- アンプル

- ボトル

- プレフィルドシリンジ

- カートリッジ

第8章 市場推計・予測:用途別、2021-2034

- 主要動向

- ワクチン

- サイトカイン

- 酵素

- モノクローナル抗体

- 遺伝子治療

- その他

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- オーストラリア

- 韓国

- 日本

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

第10章 企業プロファイル

- Adelphi

- Amcor

- Becton、Dickinson &Co.

- Berry Global

- CCL Industries

- Gerresheimer AG

- LOG Pharma Packaging

- Medical Packaging Inc.、LLC

- Merck KGaA

- PCI

- Piramal Glass Private Limited

- Schott AG

- Shandong Pharmaceutical Glass Co

- Sonoco

- Stevanato Group

- West Pharmaceutical Services、Inc.

The Global Biopharmaceutical Packaging Market was valued at USD 21.3 billion in 2024 and is estimated to grow at a CAGR of 8.8% to reach USD 49.2 billion by 2034, fueled by the rising demand for specialized packaging solutions capable of preserving the integrity and efficacy of sensitive biological drugs. As the biopharma sector keeps expanding its focus on complex, high-value therapies-including monoclonal antibodies, cell and gene therapies, and mRNA-based drugs-the importance of advanced packaging solutions is rising sharply. Biopharmaceuticals are highly sensitive to environmental changes, requiring controlled storage and transportation conditions. This has led to a surge in demand for innovative materials and technologies designed to protect drug stability throughout the supply chain. With regulatory authorities around the globe tightening packaging safety standards, pharmaceutical companies are rethinking how they protect their biologics. On top of that, as more biologics enter the global market, there's a stronger push for packaging formats that ensure sterility, enable real-time monitoring, and align with sustainability goals.

The shift toward more innovative and robust packaging solutions is further supported by growing investments in cold chain logistics and an expanding global base of biologic drug consumers. Biopharmaceutical companies are responding by adopting high-performance materials that can endure extreme temperatures and maintain product efficacy from manufacturing sites to point-of-care delivery. Rising emphasis on sustainability is also influencing design choices. As healthcare providers and end users alike demand safer and greener options, packaging firms are accelerating the development of recyclable, biodegradable, and reusable solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.3 Billion |

| Forecast Value | $49.2 Billion |

| CAGR | 8.8% |

Trade policy shifts, especially the retaliatory tariffs placed on pharma-related imports, have added another layer of complexity to market dynamics. These tariffs are increasing raw material costs, particularly for high-grade plastics and pharmaceutical-grade glass sourced internationally. The resulting cost surge has made domestic manufacturing more expensive, which is impacting procurement strategies across the value chain. Companies are now exploring localized supply chains and alternative sourcing models to offset rising input costs while maintaining compliance and quality standards.

At the same time, technology is reshaping how biopharmaceutical products are packaged and monitored. Smart packaging formats are becoming a game changer, especially for temperature-sensitive biologics. Solutions integrated with RFID tags and sensors are enabling real-time tracking of critical parameters like temperature, humidity, and product integrity. These intelligent systems help minimize waste, reduce the risk of compromised products, and improve overall patient safety. As demand for precision in drug delivery and storage continues to grow, smart packaging is quickly moving from a luxury to a necessity in this high-stakes industry.

In 2024, biodegradable packaging materials accounted for 66.1% of the global market, underlining a decisive shift toward sustainability. This trend reflects not just a response to growing environmental awareness among consumers but also stronger regulatory pressure to phase out single-use plastics in pharmaceutical applications. Biodegradable materials have evolved significantly and now offer the durability, chemical resistance, and barrier protection required for pharmaceutical use. These innovations have helped biodegradable packaging move beyond niche status, making it a competitive alternative to traditional plastic solutions across a broad range of drug formats.

Despite this shift, plastic packaging still held a dominant position in 2024, with a market value of USD 14.5 billion. Its widespread use continues to be supported by its cost-effectiveness, design flexibility, and excellent protective qualities. Plastics are especially favored in applications requiring tamper-evident features, high moisture resistance, and compatibility with specialized components like child-safe closures and single-use systems. Continuous advancements in polymer science have enhanced the performance of plastic packaging, enabling it to meet the increasingly stringent demands of pharmaceutical storage and distribution.

The U.S. Biopharmaceutical Packaging Market is projected to hit USD 2.5 billion by 2034, driven by the country's strong pharmaceutical manufacturing ecosystem and innovation in biotech. A combination of strict regulatory standards and rising consumer expectations around safety, integrity, and sustainability is pushing packaging firms to innovate faster. Smart, traceable, and eco-conscious packaging formats are becoming essential as the industry adapts to new challenges and opportunities in drug delivery and compliance.

Companies like Amcor, Schott AG, Gerresheimer AG, Becton, Dickinson & Co., and CCL Industries are actively investing in R&D to stay ahead. These firms are partnering with pharmaceutical companies to co-develop next-gen packaging solutions, scale up eco-friendly alternatives, and adopt digital tools for supply chain visibility and regulatory alignment. As the global market matures, strategic innovation in biopharmaceutical packaging will remain central to supporting the safe and efficient delivery of the world's most advanced therapies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research Approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.1.3 Impact on the industry

- 3.2.2 Supply-side impact (raw materials)

- 3.2.2.1 Price volatility in key materials

- 3.2.2.2 Supply chain restructuring

- 3.2.2.3 Production cost implications

- 3.2.3 Demand-side impact (selling price)

- 3.2.3.1 Price transmission to end markets

- 3.2.3.2 Market share dynamics

- 3.2.3.3 Consumer response patterns

- 3.2.4 Key companies impacted

- 3.2.5 Strategic industry responses

- 3.2.5.1 Supply chain reconfiguration

- 3.2.5.2 Pricing and product strategies

- 3.2.5.3 Policy engagement

- 3.2.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Growing demand for sustainable and eco-friendly packaging solutions

- 3.3.1.2 Global expansion and modernization of healthcare infrastructure

- 3.3.1.3 The growing prevalence of chronic and lifestyle diseases

- 3.3.1.4 Rapid technological innovations such as smart packaging systems

- 3.3.1.5 Rising investments in R&D for biologics and personalized medicines

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High initial investment and operational costs

- 3.3.2.2 Complex supply chain logistics and stringent quality standards

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn & Units)

- 5.1 Key trends

- 5.2 Biodegradable

- 5.3 Non-biodegradable

Chapter 6 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn & Units)

- 6.1 Key trends

- 6.2 Plastic

- 6.2.1 Polyvinyl Chloride (PVC)

- 6.2.2 Polypropylene (PP)

- 6.2.3 Polyethylene Terephthalate (PET)

- 6.2.4 Polystyrene (PS)

- 6.2.5 Polyethylene (PE)

- 6.2.5.1 HDPE

- 6.2.5.2 LDPE

- 6.2.5.3 LLDPE

- 6.2.6 Others

- 6.3 Glass

Chapter 7 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn & Units)

- 7.1 Key trends

- 7.2 Vials

- 7.3 Ampoules

- 7.4 Bottles

- 7.5 Pre-filled syringes

- 7.6 Cartridges

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn & Units)

- 8.1 Key trends

- 8.2 Vaccines

- 8.3 Cytokines

- 8.4 Enzymes

- 8.5 Monoclonal antibodies

- 8.6 Gene therapies

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Australia

- 9.4.4 South Korea

- 9.4.5 Japan

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 U.A.E.

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Adelphi

- 10.2 Amcor

- 10.3 Becton, Dickinson & Co.

- 10.4 Berry Global

- 10.5 CCL Industries

- 10.6 Gerresheimer AG

- 10.7 LOG Pharma Packaging

- 10.8 Medical Packaging Inc., LLC

- 10.9 Merck KGaA

- 10.10 PCI

- 10.11 Piramal Glass Private Limited

- 10.12 Schott AG

- 10.13 Shandong Pharmaceutical Glass Co

- 10.14 Sonoco

- 10.15 Stevanato Group

- 10.16 West Pharmaceutical Services, Inc.