スペシャルティカーボンブラックの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Specialty Carbon Black Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740842

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

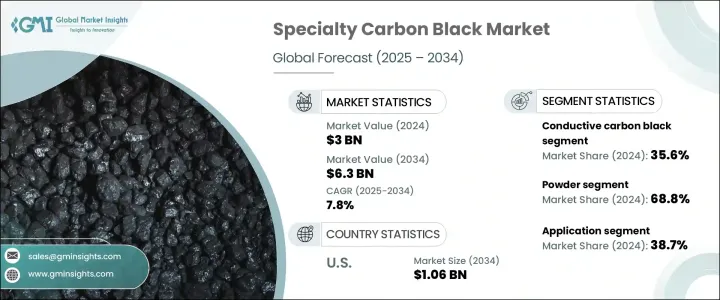

スペシャルティカーボンブラックの世界市場は、2024年には30億米ドルと評価され、CAGR 7.8%で成長し、2034年には63億米ドルに達すると推定されています。

同市場は、導電性、耐紫外線性、機械的耐久性の向上など、特定の特性を持つ高性能添加剤を必要とする複数の産業で利用が増加しているため、着実な勢いを見せています。主な成長要因のひとつは、一貫した性能と安定性が重要なエネルギー貯蔵システムを中心に、高度な電池技術におけるスペシャルティカーボンブラックの採用が増加していることです。並行して、プラスチックやポリマー産業においても、スペシャルティカーボンブラックの補強性や導電性が包装材料や様々な高性能プラスチック部品に採用されつつあります。この需要は、自動車から農業に至るまで、持続可能で効率的な材料ソリューションへの関心の高まりに支えられています。スペシャルティカーボンブラックを農業用フィルムや工業用袋に使用することで、UVカットや物理的弾力性が不可欠な屋外用途での需要がさらに高まります。また、市場参入企業は、現在進行中の次世代素材の開発においても、スペシャルティカーボンブラックの可能性を認めており、イノベーションパイプラインにおいて、スペシャルティカーボンブラックは不可欠な要素となっています。

2024年のスペシャルティカーボンブラック市場は、形状別に粉末と顆粒に区分され、合計市場価値は30億米ドルに達します。粉末ベースのスペシャルティカーボンブラックがこのセグメントを独占し、総シェアの68.8%を占めました。この形態は、導電性材料、高効率コーティング、リチウムイオン電池部品の製造に広く使用されており、そこでは微粒子の分散と材料の適合性が性能に不可欠です。プラスチック分野もパウダースペシャルティカーボンブラックの主要な消費者であり、特に見た目の均一性と構造的完全性が要求される精密用途で使用されています。現在、顆粒状は市場のごく一部を占めるに過ぎないが、そのダストフリー特性と加工性能の向上により、クリーンで効率的な産業環境に望ましい選択肢として、徐々に支持を集めつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 30億米ドル |

| 予測金額 | 63億米ドル |

| CAGR | 7.8% |

市場はグレード別にも分類され、主要セグメントは導電性カーボンブラック、ファイバーカーボンブラック、食品用カーボンブラック、その他です。2024年には、導電性カーボンブラックが市場全体の35.6%を占め、主要セグメントとして浮上しました。このグレードが好まれる主な理由は、導電性を高め、電荷保持を改善し、重要な用途の部品の動作寿命を延ばす効果があるためです。カーボンブラックは、進化するエネルギー分野と電子用途の先端材料開発で人気を集め続けています。ファイバーカーボンブラックは、高耐久性材料生産において強い関連性を維持し、セグメント内訳で僅差で続いています。

用途別では、ゴム産業が2024年に世界需要の38.7%を占めて最大の市場シェアを占めました。この優位性は、補強と耐環境性が不可欠なタイヤとタイヤ以外のゴム製品の両方で幅広く使用されていることに起因します。スペシャルティカーボンブラックをゴムコンパウンドに配合することで、製品の寿命、表面安定性、保護機能が向上し、さまざまなゴムベース製品の生産サイクルの要となる材料となっています。

地域別では、米国が世界のスペシャルティカーボンブラック市場で大きなシェアを占めており、2024年には市場全体の16.1%を占めました。このシェアは4億9,000万米ドルの市場価値に相当し、2034年には約10億6,000万米ドルに成長すると予測されています。米国の好調な市場実績は、高度な製造エコシステム、自動車やエネルギー貯蔵分野からの需要、持続可能な材料イノベーションへの継続的な投資と密接に関連しています。また、バイオベースの代替材料を推進する政府のイニシアティブも、採用率と国内生産能力の着実な増加に寄与しています。

スペシャルティカーボンブラック業界の競合構造は、戦略的提携、製品イノベーション、地域拡大を通じて市場シェア拡大に積極的に取り組む世界企業の存在によって形成されています。各社は、急速に進化する市場環境の中で差別化を図るため、サプライチェーンの強化、製品品質の向上、持続可能性の目標への取り組みに注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国

- 主要輸入国

注:上記の貿易統計は主要国についてのみ提供されます

- 利益率分析

- サプライヤーの情勢

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 導電性アプリケーションの需要の高まり

- 拡大する自動車部門と軽量化の傾向

- プラスチックおよびポリマー産業の成長

- 急成長する電気自動車(EV)とエネルギー貯蔵市場

- 高性能コーティングや塗料での使用が増加

- ポリマー複合材料の進歩

- 業界の潜在的リスク&課題

- 原材料費の高騰とサプライチェーンの不安定さ

- 炭素排出に関する厳しい環境規制

- 代替材料(グラフェン、シリカ、ナノチューブ)との競合

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:形態別、2021 –2034

- 主要動向

- 粉

- 顆粒

第6章 市場推計・予測:学年別、2021 –2034

- 主要動向

- 導電性カーボンブラック

- ファイバーカーボンブラック

- 食品グレードのカーボンブラック

- その他

第7章 市場推計・予測:用途別、2021 –2034

- 主要動向

- ゴム

- プラスチック

- 印刷インクとトナー

- 塗料とコーティング

- 電池電極

- その他

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Asahi Carbon Co. Ltd.

- Atlas Organics Private Limited

- Birla Carbon

- Black Bear Carbon B.V.

- Cabot Corporation

- Continental Carbon Company

- Denka Company Limited

- Himadri Specialty Chemical Ltd

- Omsk Carbon Group

- Orion Engineered Carbons GmbH

- Phillips Carbon Black Limited

- Ralson

- Tokai Carbon Co.、Ltd.

目次

The Global Specialty Carbon Black Market was valued at USD 3 billion in 2024 and is estimated to grow at a CAGR of 7.8% to reach USD 6.3 billion by 2034. The market is witnessing steady momentum due to increasing utilization across several industries demanding high-performance additives with specific attributes like electrical conductivity, ultraviolet resistance, and enhanced mechanical durability. One of the primary growth drivers is the rising adoption of specialty carbon black in advanced battery technologies, particularly in energy storage systems where consistent performance and stability are critical. A parallel growth trend is observed in the plastics and polymer industries, which are incorporating specialty carbon black for its reinforcing and conductive properties in packaging materials and various high-performance plastic components. This demand is further supported by increased interest in sustainable and efficient material solutions across sectors ranging from automotive to agriculture. The use of specialty carbon black in agricultural films and industrial sacks adds another layer of demand in outdoor applications, where UV protection and physical resilience are essential. Market participants are also recognizing its potential in the ongoing development of next-generation materials, which positions specialty carbon black as a vital component in the innovation pipeline.

In terms of form, the specialty carbon black market in 2024 was segmented into powder and granules, with a combined market value of USD 3 billion. Powder-based specialty carbon black dominated the segment, accounting for 68.8% of the total share. This form is widely used in the production of conductive materials, high-efficiency coatings, and lithium-ion battery components, where fine particle dispersion and material compatibility are essential for performance. The plastics sector is also a key consumer of powder specialty carbon black, particularly in precision applications where visual uniformity and structural integrity are required. Although the granule form currently holds a smaller portion of the market, it is gradually gaining traction due to its dust-free properties and improved processing performance, making it a desirable option for clean and efficient industrial environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3 Billion |

| Forecast Value | $6.3 Billion |

| CAGR | 7.8% |

The market is also categorized by grade, with the major segments including conductive carbon black, fiber carbon black, food-grade carbon black, and others. In 2024, conductive carbon black emerged as the leading segment, representing 35.6% of the overall market. The preference for this grade is largely driven by its effectiveness in enhancing electrical conductivity, improving charge retention, and extending the operational life of components in critical applications. It continues to gain popularity in the evolving energy sector and advanced material development for electronic applications. Fiber carbon black follows closely in the segment breakdown, maintaining strong relevance in high-durability material production.

By application, the rubber industry held the largest market share in 2024, accounting for 38.7% of the global demand. This dominance stems from its broad use in both tire and non-tire rubber products, where reinforcement and environmental resistance are essential. The integration of specialty carbon black in rubber compounds improves product lifespan, surface stability, and protective functionality, making it a cornerstone material in the production cycle of various rubber-based goods.

Geographically, the United States accounted for a significant share of the global specialty carbon black market, capturing 16.1% of the total market in 2024. This share translates to a market value of USD 490 million, with projections indicating growth to approximately USD 1.06 billion by 2034. The strong market performance in the U.S. is closely linked to its advanced manufacturing ecosystem, demand from the automotive and energy storage sectors, and ongoing investments in sustainable material innovations. Government-backed initiatives promoting bio-based alternatives are also contributing to a steady increase in adoption and domestic production capabilities.

The competitive structure of the specialty carbon black industry is shaped by the presence of several global players actively working to expand their market share through strategic alliances, product innovations, and regional expansions. Companies are focusing on enhancing their supply chains, improving product quality, and addressing sustainability goals to differentiate themselves in a rapidly evolving market landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Profit margin analysis

- 3.5 Supplier landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising demand for conductive applications

- 3.8.1.2 Expanding automotive sector and lightweighting trend

- 3.8.1.3 Growth in plastics and polymers industry

- 3.8.1.4 Booming electric vehicle (EV) and energy storage market

- 3.8.1.5 Increasing use in high-performance coatings and paints

- 3.8.1.6 Advancements in polymer composite materials

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High raw material costs and supply chain volatility

- 3.8.2.2 Stringent environmental regulations on carbon emissions

- 3.8.2.3 Competition from alternative materials (graphene, silica, and nanotubes)

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Form, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Powder

- 5.3 Granules

Chapter 6 Market Estimates and Forecast, By Grade, 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Conductive carbon black

- 6.3 Fiber carbon black

- 6.4 Food-grade carbon black

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Rubber

- 7.3 Plastics

- 7.4 Printing inks & toners

- 7.5 Paints & coatings

- 7.6 Battery electrodes

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Asahi Carbon Co. Ltd.

- 9.2 Atlas Organics Private Limited

- 9.3 Birla Carbon

- 9.4 Black Bear Carbon B.V.

- 9.5 Cabot Corporation

- 9.6 Continental Carbon Company

- 9.7 Denka Company Limited

- 9.8 Himadri Specialty Chemical Ltd

- 9.9 Omsk Carbon Group

- 9.10 Orion Engineered Carbons GmbH

- 9.11 Phillips Carbon Black Limited

- 9.12 Ralson

- 9.13 Tokai Carbon Co., Ltd.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日