家畜乳房の健康の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Udder Health Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740839

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

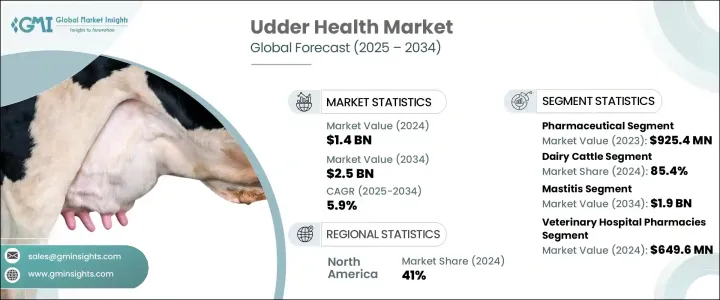

家畜乳房の健康の世界市場は、2024年には14億米ドルとなり、乳房疾患、特に乳房炎に対する懸念の高まりと乳製品に対する世界の需要の急増により、CAGR 5.9%で成長し、2034年には25億米ドルに達すると予測されています。

酪農経営が世界的に拡大・激化する中、事前予防的管理の重要性がこれまで以上に高まっています。乳房炎は乳牛に影響を及ぼす最も一般的で費用のかかる病気の1つであり、生乳生産量の大幅な損失、獣医費用の増加、長期的な牛群の健康問題につながります。酪農家は、収益性と動物福祉を維持するため、早期発見と予防に一層力を入れています。さらに、持続可能な農業を目指す世界の動きは、従来の抗生物質に代わる選択肢の採用を促し、家畜乳房の健康市場に変化をもたらしています。

主要な酪農生産国の規制機関は、抗菌剤の使用についてより厳しい規制を実施しており、革新的な治療法、ワクチン、プロバイオティクス、免疫強化ソリューションの需要をさらに加速させています。AIを活用した健康モニタリング、精密治療プラットフォーム、高度な牛群管理システムなどの治療技術は、酪農家の家畜乳房の健康への取り組み方を再構築しています。倫理的に調達された抗生物質不使用の乳製品に対する消費者の需要が高まる中、技術革新、進化する農法、動物福祉と食品安全に対する意識の高まりの組み合わせに支えられ、市場は今後10年間で力強い成長を遂げると思われます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 14億米ドル |

| 予測金額 | 25億米ドル |

| CAGR | 5.9% |

乳房炎は酪農牛群で頻繁に発生する懸念事項であり、効果的な診断、治療、予防ソリューションへの需要が引き続き高まっています。酪農の集約化が進むにつれ、抗菌剤耐性を最小限に抑えるため、標的抗生物質や非侵襲的治療法などの新しい治療法が開発されています。ワクチン、プロバイオティクス、免疫療法における画期的な進歩は、慢性感染症を減らし、乳量を増加させることにより、牛群の健康を著しく改善しています。最新のワクチンは乳房炎やその他の乳房感染症の予防に非常に効果的になりつつあり、プロバイオティクスや免疫刺激療法は乳牛のマイクロバイオームを健全に保つために極めて重要であることが証明されつつあります。これらの進歩は、動物の福祉を向上させるだけでなく、抗生物質への依存度を下げることで、より持続可能な酪農を促進しています。

市場は医薬品とサプリメントに区分されます。医薬品セグメントは、2023年に9億2,540万米ドルを創出し、乳房感染症の発生率の増加と抗菌剤耐性に対する懸念の高まりに後押しされました。AIを活用した処方システムの採用が増加し、治療精度と牛群の健康が強化され、医薬品分野の成長をさらに後押ししています。

動物の種類別では、乳牛が2024年のシェア85.4%で市場を独占しています。早期診断技術、遺伝学、耐病性への投資の増加により、牛群管理の方法が再構築されつつあります。世界の抗生物質規制の中、酪農家はプロバイオティクスや免疫療法薬の採用を増やしており、AIを活用したモニタリングや自動搾乳システムが人気を集めています。

北米家畜乳房の健康2024年の世界売上高の41%を占め、2025年から2034年にかけてCAGR 5.8%で成長すると予測されます。米国では生乳生産が好調で、精密ツールや持続可能な管理戦略など、先進的な家畜乳房の健康ソリューションへの需要が高まっています。FDA(米国食品医薬品局)やUSDA(米国農務省)が主導する抗生物質使用削減のための規制強化は、ワクチン、プロバイオティクス、免疫刺激療法の普及をさらに後押ししています。

世界の家畜乳房の健康業界の主要企業は、Merck、BouMatic、AHV International、Albert Kerbl、Boehringer Ingelheim、Ceva Sante Animale、Ecolab、Elanco Animal Health、DeLaval、G Shepherd Animal Health、Virbac、Zoetisなどです。これらの企業は、抗菌剤耐性の懸念に対処するための革新的な治療法への投資、診断のためのAIと自動化機能の拡大、製品採用を改善するための動物病院や農家との提携、環境に優しい製品開発や農家教育イニシアティブを通じた持続可能性への取り組みの強化を行っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 世界的に乳製品の消費量と生産量が増加

- 家畜乳房の健康管理に関する意識の向上

- 獣医診断と治療の進歩

- 業界の潜在的リスク&課題

- 乳製品業界における抗生物質の使用に関する厳格な規制

- 家畜乳房の健康治療と診断の高コスト

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 医薬品

- 抗生物質

- ワクチン

- 抗炎症薬

- 乳頭消毒剤

- 乳房内注入

- その他の医薬品

- 補足

- ビタミンとミネラル

- プロバイオティクスとプレバイオティクス

- その他のサプリメント

第6章 市場推計・予測:動物の種類別、2021-2034

- 主要動向

- 乳牛

- その他の動物の種類

第7章 市場推計・予測:病気の種類別、2021-2034

- 主要動向

- 乳腺炎

- 臨床的乳腺炎

- 潜在性乳腺炎

- その他の病気の種類

第8章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 動物病院薬局

- 小売薬局

- その他の流通チャネル

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AHV International

- Albert Kerbl

- Boehringer Ingelheim

- BouMatic

- Ceva Sante Animale

- DeLaval

- Ecolab

- Elanco Animal Health

- G Shepherd Animal Health

- Merck

- Virbac

- Zoetis

目次

The Global Udder Health Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 2.5 billion by 2034, driven by rising concerns over udder diseases, especially mastitis, along with the surging global demand for dairy products. As dairy farming operations expand and intensify worldwide, the importance of proactive udder health management is becoming more critical than ever. Mastitis remains one of the most common and costly diseases affecting dairy cows, leading to significant losses in milk production, increased veterinary expenses, and long-term herd health issues. Farmers are focusing more on early detection and prevention to maintain profitability and animal welfare. Moreover, the global push for sustainable farming practices is transforming the udder health market, encouraging the adoption of alternatives to traditional antibiotics.

Regulatory bodies across major dairy-producing nations are enforcing stricter controls on antimicrobial use, further accelerating the demand for innovative treatments, vaccines, probiotics, and immune-boosting solutions. Technologies such as AI-driven health monitoring, precision treatment platforms, and advanced herd management systems are reshaping how farmers approach udder health. With consumer demand rising for ethically sourced and antibiotic-free dairy products, the market is set to experience robust growth over the next decade, supported by a combination of technological innovations, evolving farming practices, and increasing awareness about animal welfare and food safety.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.5 Billion |

| CAGR | 5.9% |

Mastitis, a frequent concern in dairy herds, continues to drive demand for effective diagnostic, therapeutic, and preventive solutions. As dairy farming grows more intensive, new treatments such as targeted antibiotics and non-invasive therapies are being developed to minimize antimicrobial resistance. Breakthroughs in vaccines, probiotics, and immunotherapies are significantly improving herd health by reducing chronic infections and boosting milk yields. Modern vaccines are becoming highly effective at preventing mastitis and other udder infections, while probiotics and immune-stimulant therapies are proving crucial for maintaining a healthy microbiome in dairy cows. These advancements are not only enhancing animal welfare but are also promoting more sustainable dairy farming by lowering antibiotic reliance.

The market is segmented into pharmaceutical products and supplements. The pharmaceutical segment generated USD 925.4 million in 2023, fueled by the growing incidence of udder infections and heightened concerns over antimicrobial resistance. The rising adoption of AI-powered prescription systems is enhancing treatment precision and herd health, further supporting growth in the pharmaceutical sector.

In terms of animal type, dairy cattle dominated the market with an 85.4% share in 2024. Rising investments in early diagnostic technologies, genetics, and disease resistance are reshaping herd management practices. Farmers are increasingly adopting probiotics and immunotherapy drugs amid global antibiotic restrictions, with AI-driven monitoring and automated milking systems gaining traction.

North America Udder Health Market accounted for 41% of global revenue in 2024 and is projected to grow at a CAGR of 5.8% from 2025 to 2034. Strong milk production across the U.S. is fueling the demand for advanced udder health solutions, including precision tools and sustainable management strategies. Regulatory pushes to reduce antibiotic use, led by the FDA and USDA, are further boosting the uptake of vaccines, probiotics, and immune-stimulant therapies.

Major players in the global udder health industry include Merck, BouMatic, AHV International, Albert Kerbl, Boehringer Ingelheim, Ceva Sante Animale, Ecolab, Elanco Animal Health, DeLaval, G Shepherd Animal Health, Virbac, and Zoetis. These companies are investing in innovative treatments to address antimicrobial resistance concerns, expanding AI and automation capabilities for diagnostics, partnering with veterinary clinics and farmers to improve product adoption, and enhancing sustainability efforts through eco-friendly product development and farmer education initiatives.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising dairy consumption and production globally

- 3.2.1.2 Increased awareness about udder health management

- 3.2.1.3 Advancements in veterinary diagnostics and treatment

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulations on antibiotic use in dairy industry

- 3.2.2.2 High cost of udder health treatments and diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pharmaceuticals

- 5.2.1 Antibiotics

- 5.2.2 Vaccines

- 5.2.3 Anti-inflammatory drugs

- 5.2.4 Teat disinfectants

- 5.2.5 Intramammary infusions

- 5.2.6 Other pharmaceuticals

- 5.3 Supplement

- 5.3.1 Vitamins and minerals

- 5.3.2 Probiotics and prebiotics

- 5.3.3 Other supplements

Chapter 6 Market Estimates and Forecast, By Animal Type, 2021-2034 ($ Mn)

- 6.1 Key trends

- 6.2 Dairy cattle

- 6.3 Other animal types

Chapter 7 Market Estimates and Forecast, By Disease Type, 2021-2034 ($ Mn)

- 7.1 Key trends

- 7.2 Mastitis

- 7.2.1 Clinical mastitis

- 7.2.2 Sub-clinical mastitis

- 7.3 Other disease types

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021-2034 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Other distribution channels

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AHV International

- 10.2 Albert Kerbl

- 10.3 Boehringer Ingelheim

- 10.4 BouMatic

- 10.5 Ceva Sante Animale

- 10.6 DeLaval

- 10.7 Ecolab

- 10.8 Elanco Animal Health

- 10.9 G Shepherd Animal Health

- 10.10 Merck

- 10.11 Virbac

- 10.12 Zoetis

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日