注射器と注射薬包装の市場機会と促進要因、業界動向分析、2025年~2034年予測

Syringes and Injectable Drugs Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740831

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

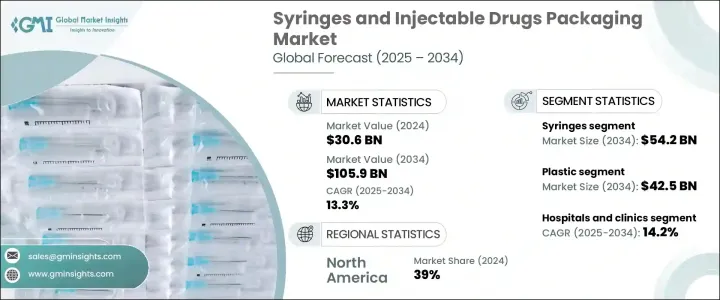

世界の注射器と注射薬包装市場は、2024年に306億米ドルと評価され、特に慢性疾患や感染症の症例が増加する中、注射療法に対する需要の高まりに牽引され、CAGR 13.3%で成長し、2034年には1,059億米ドルに達すると推定されています。

ヘルスケア業界では、即効性と正確な投与が可能なドラッグデリバリーへのシフトが急速に進んでいます。このシフトは、医薬品包装の展望を再構築し、メーカーに革新と進化する医療ニーズへの適応を促しています。低侵襲治療の急増、生物製剤の拡大、自己投与薬への嗜好の高まりは、先進パッケージングシステムの重要な役割を強化しています。製薬会社が注射剤ポートフォリオを拡大し続ける中、無菌性、使いやすさ、規制遵守を保証するパッケージングに対する需要は、これまで以上に緊急性を増しています。さらに、世界の健康危機と人口の高齢化により、特に救急、外来、在宅医療の現場において、効果的で安全かつ拡張性の高いドラッグデリバリーへのニーズがさらに高まっています。

特に外来や救急医療では、迅速な薬剤投与のために注射剤の使用が増加しており、薬剤の完全性と患者の安全性を維持する安全で無菌の包装に対するニーズが高まっています。注射器と注射薬のパッケージングが厳格な安全基準を満たしていることを確認することは、汚染を防ぎ、薬剤の安定性を維持し、臨床現場における医療規制を遵守するために不可欠です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 306億米ドル |

| 予測金額 | 1,059億米ドル |

| CAGR | 13.3% |

急速な成長にもかかわらず、市場は注目すべき課題に直面しています。医療部品に対する貿易政策と関税の変化が価格構造を複雑にし、製品の入手を制限しています。輸入材料に対する最近の関税引き上げは、特に無菌注射剤や低価格治療薬の製造コストを押し上げています。業界各社は原材料を備蓄し、段階的な政策転換を推進することで対応しているが、品質やコスト効率を落とさずに需要の増加に対応しようとするメーカーにとって、サプライチェーンの混乱は依然として大きなハードルとなっています。

製品タイプ別に見ると、市場は注射器と注射薬に合わせた包装形態に区分されます。病院、診療所、在宅医療の現場では、汚染リスクを低減しドラッグデリバリーの安全性を高めるため、滅菌済みで開封が容易なソリューションの採用が増加しており、注射器だけでも2034年までに542億米ドルの売上が見込まれています。また、ワクチン、糖尿病、自己免疫疾患などにおける注射療法の使用拡大も、シングルユースで安全性を高めたシリンジシステムの採用を後押ししています。

素材別では、プラスチック、ガラス、その他の特殊基板が市場に含まれます。プラスチックは軽量で割れにくく、価格も手ごろであることから、2034年の市場規模は425億米ドルと推定され、リードすると予測されています。プラスチックはプレフィルドシリンジや自己注射器用の材料として選ばれており、引き込み式注射針や投与量追跡システムなどの安全機能を統合した設計をサポートしています。

北米は2024年に39%の市場シェアを占め、強力な医薬品製造インフラと先進ヘルスケアシステムのおかげで、引き続き優位を保っています。病院や在宅介護事業者が感染率の低下と薬剤投与の合理化を求めているため、プレフィルド・使い捨て注射剤パッケージの需要が急速に高まっています。

ニプロ・欧州・グループ・カンパニーズ、ゲレスハイマー、ウェスト・ファーマシューティカル・サービス、ショットAG、BDなどの主要企業は、研究開発への投資、製造拠点の拡大、生産ラインの自動化、戦略的パートナーシップの構築を行い、製品の安全性の向上、生産効率の向上、世界市場での規制遵守の維持に努めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 注射ドラッグデリバリーの需要増加

- 消費者向けワクチンおよびその他の医薬品の成長

- 包装における技術の進歩

- 持続可能性と環境への圧力

- 人口の高齢化と世界のヘルスケアアクセスの拡大

- 業界の潜在的リスク&課題

- デバイスの互換性と薬剤の安定性の問題

- 原材料供給の制約

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 注射器

- プレフィルドシリンジ

- 従来の注射器

- 注射薬の包装

- バイアル

- アンプル

- カートリッジ

- ボトル

第6章 市場推計・予測:材質別、2021-2034

- 主要動向

- プラスチック

- ポリプロピレン(PP)

- ポリエチレン(PE)

- ポリカーボネート(PC)

- その他

- ガラス

- その他

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院と診療所

- 外来手術センター(ASC)

- 製薬・バイオテクノロジー企業

- 在宅ヘルスケア環境

- ワクチン接種センター

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- BD

- AptarGroup、Inc.

- Bormioli Pharma S.p.A.

- Catalent、Inc

- Credence MedSystems、Inc.

- DWK Life Sciences.

- Gerresheimer

- J.Penner Corporation

- Laboratorios Farmaceuticos Rovi S.A.

- Nipro Europe Group Companies

- Schott AG

- SGD Pharma

- Shandong Province Medicinal Glass Co.、Ltd.

- Stevanato Group

- Terumo Europe NV

- USIN Advance Co.、Ltd.

- Weigao Group

- West Pharmaceutical Services、Inc.

目次

The Global Syringes and Injectable Drugs Packaging Market was valued at USD 30.6 billion in 2024 and is estimated to grow at a CAGR of 13.3% to reach USD 105.9 billion by 2034, driven by the rising demand for injectable therapies, especially amid increasing cases of chronic and infectious diseases. The healthcare industry is experiencing a rapid shift toward injectable drug delivery due to its ability to provide fast-acting relief and precise dosing. This shift is reshaping the pharmaceutical packaging landscape, pushing manufacturers to innovate and adapt to evolving medical needs. The surge in minimally invasive treatments, expansion of biologics, and growing preference for self-administered drugs are reinforcing the critical role of advanced packaging systems. As pharmaceutical companies continue to expand their injectable portfolios, the demand for packaging that ensures sterility, ease of use, and regulatory compliance is becoming more urgent than ever. Moreover, global health crises and aging populations are further intensifying the need for effective, safe, and scalable drug delivery solutions, particularly in emergency, ambulatory, and home-based care settings.

The increasing use of injectables for quick drug administration, especially in outpatient and emergency care, has created a heightened need for secure, sterile packaging that upholds drug integrity and patient safety. Ensuring the packaging of syringes and injectable drugs meets strict safety standards is essential to prevent contamination, maintain drug stability, and comply with healthcare regulations across clinical settings.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $30.6 Billion |

| Forecast Value | $105.9 Billion |

| CAGR | 13.3% |

Despite its rapid growth, the market is facing notable challenges. Shifting trade policies and tariffs on medical components are complicating pricing structures and limiting product availability. Recent tariff hikes on imported materials have driven up manufacturing costs, especially for sterile injectables and low-cost therapies where affordability is critical. Industry players are responding by stockpiling raw materials and pushing for phased policy shifts, but supply chain disruptions remain a significant hurdle for manufacturers aiming to meet rising demand without compromising quality or cost-efficiency.

Based on product type, the market is segmented into syringes and packaging formats tailored to injectable drugs. Syringes alone are expected to generate USD 54.2 billion by 2034 as hospitals, clinics, and home care settings increasingly adopt pre-sterilized, tamper-evident solutions to reduce contamination risks and enhance drug delivery safety. The expanding use of injectable therapies across vaccines, diabetes, and autoimmune diseases is also driving the adoption of single-use, safety-enhanced syringe systems.

In terms of material, the market includes plastic, glass, and other specialized substrates. Plastic is projected to lead with an estimated market size of USD 42.5 billion by 2034 due to its lightweight, break-resistant, and affordable properties. Plastic is the material of choice for prefilled syringes and self-injection devices, supporting designs with integrated safety features like retractable needles and dose-tracking systems.

North America held a 39% market share in 2024 and continues to dominate, thanks to its strong pharmaceutical manufacturing infrastructure and advanced healthcare systems. The demand for prefilled and disposable injectable packaging is rising fast as hospitals and home care providers seek to reduce infection rates and streamline drug administration.

Leading companies, including Nipro Europe Group Companies, Gerresheimer, West Pharmaceutical Services, Inc., Schott AG, and BD, are investing in R&D, expanding manufacturing footprints, automating production lines, and building strategic partnerships to improve product safety, boost production efficiency, and maintain regulatory compliance across global markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increased demand for injectable drug delivery

- 3.3.1.2 Growth in consumer vaccination and other drugs

- 3.3.1.3 Technological advancements in packaging

- 3.3.1.4 Sustainability and environmental pressures

- 3.3.1.5 Aging population and increasing global healthcare access

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Device compatibility and drug stability issues

- 3.3.2.2 Raw material supply constraints

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Syringes

- 5.2.1 Prefilled syringes

- 5.2.2 Conventional syringes

- 5.3 Injectable drugs packaging

- 5.3.1 Vials

- 5.3.2 Ampoules

- 5.3.3 Cartridges

- 5.3.4 Bottles

Chapter 6 Market Estimates & Forecast, By Material Type, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Plastic

- 6.2.1 Polypropylene (PP)

- 6.2.2 Polyethylene (PE)

- 6.2.3 Polycarbonate (PC)

- 6.2.4 Others

- 6.3 Glass

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Ambulatory surgical centers (ASCs)

- 7.4 Pharmaceutical & biotechnology companies

- 7.5 Home healthcare settings

- 7.6 Vaccination centers

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BD

- 9.2 AptarGroup, Inc.

- 9.3 Bormioli Pharma S.p.A.

- 9.4 Catalent, Inc

- 9.5 Credence MedSystems, Inc.

- 9.6 DWK Life Sciences.

- 9.7 Gerresheimer

- 9.8 J.Penner Corporation

- 9.9 Laboratorios Farmaceuticos Rovi S.A.

- 9.10 Nipro Europe Group Companies

- 9.11 Schott AG

- 9.12 SGD Pharma

- 9.13 Shandong Province Medicinal Glass Co., Ltd.

- 9.14 Stevanato Group

- 9.15 Terumo Europe NV

- 9.16 USIN Advance Co., Ltd.

- 9.17 Weigao Group

- 9.18 West Pharmaceutical Services, Inc.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日