|

市場調査レポート

商品コード

1740830

航空機用DC-DCコンバータ市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測Aircraft DC-DC Converter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 航空機用DC-DCコンバータ市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月25日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

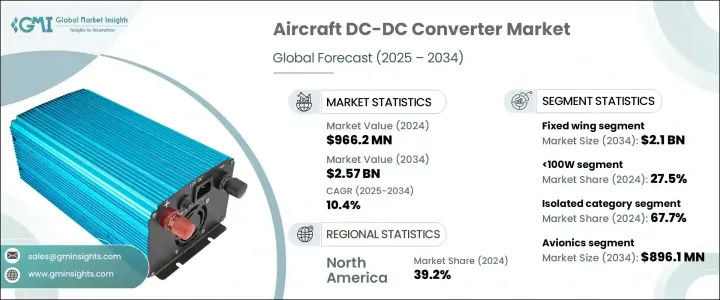

航空機用DC-DCコンバータの世界市場は、2024年には9億6,620万米ドルとなり、CAGR 10.4%で成長し、2034年には25億7,000万米ドルに達すると予測されています。

世界中で生産される航空機の数が増加していることが、航空システムで使用されるDC-DCコンバータの需要を促進している主な要因です。これらのコンポーネントは、ますます高度化する航空機の電源システムで電圧レベルを管理するために不可欠です。しかし、半導体や受動電子部品などの重要な輸入品に対する関税を含む国際貿易政策の転換が、原材料コストの上昇につながっています。相互貿易制限に起因する不確実性は、世界・サプライ・チェーンを混乱させ、調達の遅れや生産サイクルの長期化をもたらしています。複雑なシステムへの電気部品の一貫した統合に依存している航空機メーカーは、こうした貿易障壁と遅延の結果、課題に直面しています。

同時に、航空分野における近代化の取り組みは、高度な電源管理システムへの需要を押し上げています。新世代の航空機では、さまざまな機内システムに効率的で安定した電力供給が求められるため、DC-DCコンバータの役割はますます重要になっています。これらのコンバータは、航空機の電気インフラの新旧間の互換性を確保し、次世代アビオニクスと電子システムの統合をサポートします。航空機は現在、繊細なフライト・エレクトロニクスをサポートするために特定の電圧レベルを必要としており、DC-DCコンバータは、これらのニーズを満たすために電力を安定化させ、変換するという重要な役割を担っています。航空機が空気圧や油圧システムへの依存を減らし、より電気的に駆動するプラットフォームへと進化するにつれて、電力変換技術もまた、より軽量で効率的な設計をサポートするために進歩しなければなりません。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 9億6,620万米ドル |

| 予測金額 | 25億7,000万米ドル |

| CAGR | 10.4% |

航空機の種類によって、市場は固定翼と回転翼に分類されます。固定翼セグメントは、2034年までに21億米ドルに達すると予測されています。固定翼機では電動システムへの移行が進んでおり、幅広い電圧要件を管理するために不可欠なDC-DCコンバータの採用が進んでいます。これらのシステムは、エネルギー効率の向上と軽量化のために、より電気的なアーキテクチャ(MEA)への依存度が高まっている新しい航空機モデルにおいて特に重要です。固定翼プラットフォームにおける高度なオンボード・システムに対する需要の高まりが、このセグメントにおけるDC-DCコンバータの成長を引き続き促進しています。

出力電力では、市場セグメンテーションは100W、100W~500W、500W以上に区分されます。100Wセグメントは、2024年の市場の27.5%を占めています。この成長は、航空機内での低電力エレクトロニクス、センサー、アビオニクス・モジュールの使用増加によって支えられています。これらの部品は安定した低出力電圧を必要とするが、100Wコンバータはこの要件を効果的に満たします。さらに、古い航空機を最新の低電力システムに改修することで、既存の電力インフラとのシームレスな統合が可能になるため、この出力カテゴリーの需要をさらに後押ししています。

市場はさらに、製品カテゴリーに基づいて絶縁型コンバータと非絶縁型コンバータに分けられます。2024年には、絶縁型コンバータが67.7%で最大のシェアを占めています。これらは、システムの安全性と安定性を確保するために電気的絶縁が必要とされる最新の航空機に不可欠です。絶縁型コンバータは高ワット数のアプリケーションに対応するように設計されており、最新の航空機設計における複雑な電気操作に最適です。推進システムで広く使用されているほか、機内の電子機器にクリーンで安定した電力を供給するためにも使用されており、さまざまな航空機サブシステムの性能と電気的安全性を維持する上で極めて重要です。

用途別では、アビオニクス、配電、照明システム、レーダー・電子戦システム、機内エンターテインメントなどがあります。このうち、アビオニクス分野は2034年までに8億9,610万米ドルを生み出すと予測されています。航空電子工学システムの複雑化と高度化が進むにつれて、安定した干渉のない電力へのニーズも並行して高まっています。DC-DCコンバータは、エンジン制御ユニット、コックピットディスプレイ、フライトナビゲーションシステムなどのミッションクリティカルな電子機器に信頼性の高い電圧を供給するのに役立ちます。航空機がデジタルアビオニクス技術を採用し続けるにつれて、高度なコンバータによる効率的な電源管理に対する需要も増加しています。

地域別では、北米が2024年に39.2%のシェアで市場をリードしました。この主導的地位は、同地域における民間航空の拡大と航空機の近代化に起因しています。航空会社や製造業者は先進的な電子飛行システムの採用を増やしており、これらは電力安定性のために高性能DC-DCコンバータに大きく依存しています。さらに、地域の航空機にMEAシステムを導入することへの注目が高まっており、次世代電力変換ソリューションへの需要がさらに高まっています。

航空機用DC-DCコンバータ市場は競争が激しく、Honeywell International Inc.、村田製作所、TDKラムダ株式会社、Advanced Energy、Vicor Corporationなどの主要企業が市場全体の30%以上のシェアを占めています。これらの企業は、厳格な航空認証基準を満たす、コンパクトでエネルギー効率が高く、熱的に最適化されたコンバーター・ソリューションの開発に積極的に投資しています。進化する航空機技術をサポートするため、主要メーカーは窒化ガリウム(GaN)ベースの設計、モジュラー・ソリューション、共振トポロジーなどの先進的な製品アーキテクチャも導入しています。これらのイノベーションは、信頼性が高く、拡張性があり、さまざまな電圧とワット数の要件に対応できる電力変換器に対する民間航空部門と防衛航空部門の両方からの高まる需要に対応することを目的としています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 航空機の生産増加

- 先進的な航空電子機器と電子システムの統合の強化

- 軽量で高効率な電力ソリューションの需要

- 燃費と排出ガス削減への重点強化

- 先進的な航空モビリティへの注目が高まる

- 業界の潜在的リスク&課題

- 高い規制と認証の障壁

- 設計の複雑さと統合の制約

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:機種別、2021-2034

- 主要動向

- 固定翼

- 回転翼

第6章 市場推計・予測:出力別、2021-2034

- 主要動向

- 100W未満

- 100W~500W

- 500W以上

第7章 市場推計・予測:カテゴリー別、2021-2034

- 主要動向

- 孤立した

- 非孤立型

第8章 市場推計・予測:用途別、2021-2034

- 主要動向

- 航空電子機器

- 電力配分

- 照明システム

- レーダーおよび電子戦システム

- 機内エンターテイメント(IFE)

- その他

第9章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Abbott Technologies

- Advanced Energy

- AJ's Power Source Inc.

- BrightLoop

- Crane Aerospace &Electronics

- Helios Power Solutions

- Honeywell International Inc.

- KGS Electronics

- Meggitt PLC.

- Murata Manufacturing Co.、Ltd.

- Pico Electronics

- SynQor、Inc.

- Tame-Power

- TDK-Lambda Corporation

- Texas Instruments Incorporated

- Vicor Corporation

- VPT、Inc.

- XP Power

The Global Aircraft DC-DC Converter Market was valued at USD 966.2 million in 2024 and is estimated to grow at a CAGR of 10.4% to reach USD 2.57 billion by 2034. The increasing number of aircraft being produced worldwide is a major factor driving demand for DC-DC converters used in aviation systems. These components are vital for managing voltage levels in increasingly sophisticated aircraft power systems. However, shifts in international trade policies, including tariffs on critical imports such as semiconductors and passive electronic components, have led to rising raw material costs. The uncertainty caused by reciprocal trade restrictions has disrupted global supply chains, creating procurement delays and extending production cycles. Aircraft manufacturers, who rely on consistent integration of electrical components into complex systems, have faced challenges as a result of these trade barriers and delays.

At the same time, modernization efforts in the aviation sector are boosting demand for advanced power management systems. As new-generation aircraft require efficient, stable power delivery for a variety of onboard systems, the role of DC-DC converters becomes increasingly critical. These converters help ensure compatibility between older and newer aircraft electrical infrastructures, supporting the integration of next-gen avionics and electronic systems. Aircraft now require specific voltage levels to support sensitive flight electronics, and DC-DC converters fill the essential role of stabilizing and converting power to meet those needs. As aircraft evolve into more electrically driven platforms, with reduced reliance on pneumatic and hydraulic systems, power conversion technology must also advance to support lighter, more efficient designs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $966.2 Million |

| Forecast Value | $2.57 Billion |

| CAGR | 10.4% |

Based on aircraft type, the market is categorized into fixed wing and rotary wing. The fixed wing segment is anticipated to reach USD 2.1 billion by 2034. The growing transition toward electrically powered systems in fixed wing aircraft is encouraging the adoption of DC-DC converters, which are essential for managing a wide range of voltage requirements. These systems are especially important in newer aircraft models, which increasingly rely on more electric architecture (MEA) to enhance energy efficiency and reduce weight. The rising demand for advanced onboard systems in fixed wing platforms continues to drive the growth of DC-DC converters in this segment.

In terms of output power, the aircraft DC-DC converter market is segmented into 100W, 100W-500W, and above 500W categories. The 100W segment accounted for 27.5% of the market in 2024. This growth is supported by the rising usage of low-power electronics, sensors, and avionics modules within aircraft. These components require stable, low-output voltage, and 100W converters meet this requirement effectively. Additionally, the retrofitting of older aircraft with modern low-power systems further supports the demand for this output category, as it allows for seamless integration with existing power infrastructure.

The market is further divided into isolated and non-isolated converters based on product category. In 2024, isolated converters held the largest share at 67.7%. These are essential in modern aircraft, where electrical isolation is needed to ensure system safety and stability. Isolated converters are designed to handle high-wattage applications, making them ideal for complex electrical operations in newer aircraft designs. They are used extensively in propulsion systems and to provide clean, stable power to onboard electronics, which is crucial for maintaining performance and electrical safety across various aircraft subsystems.

By application, the market includes avionics, power distribution, lighting systems, radar and electronic warfare systems, in-flight entertainment, and others. Among these, the avionics segment is projected to generate USD 896.1 million by 2034. As the complexity and sophistication of avionics systems continue to rise, the need for stable, interference-free power grows in parallel. DC-DC converters help provide reliable voltage for mission-critical electronics such as engine control units, cockpit displays, and flight navigation systems. As aircraft continue to adopt digital avionics technologies, the demand for efficient power management through advanced converters also increases.

Regionally, North America led the market in 2024 with a 39.2% share. This leadership position is attributed to the expansion of commercial aviation and the modernization of aircraft fleets in the region. Airlines and manufacturers are increasingly adopting advanced electronic flight systems, which rely heavily on high-performance DC-DC converters for power stability. Moreover, the growing focus on implementing MEA systems in regional fleets is creating further demand for next-gen power conversion solutions.

The aircraft DC-DC converter market is highly competitive, with major players such as Honeywell International Inc., Murata Manufacturing Co., TDK-Lambda Corporation, Ltd., Advanced Energy, and Vicor Corporation collectively accounting for over 30% of the total market share. These companies are actively investing in the development of compact, energy-efficient, and thermally optimized converter solutions that meet rigorous aviation certification standards. To support evolving aircraft technologies, key manufacturers are also introducing advanced product architectures such as gallium nitride (GaN)-based designs, modular solutions, and resonant topologies. Their innovations aim to address the growing demand from both commercial and defense aviation sectors for power converters that are reliable, scalable, and capable of handling varied voltage and wattage requirements.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw material)

- 3.2.2.1.1 Price volatility

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw material)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising production of aircraft

- 3.3.1.2 Increasing integration of advanced avionics and electronic systems

- 3.3.1.3 Demand for lightweight and high-efficiency power solutions

- 3.3.1.4 Increased focus on fuel efficiency and emission reduction

- 3.3.1.5 Growing focus towards advanced air mobility

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High regulatory and certification barriers

- 3.3.2.2 Design complexity and integration constraints

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Aircraft Type, 2021-2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Fixed wing

- 5.3 Rotary wing

Chapter 6 Market Estimates & Forecast, By Output Power, 2021-2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 <100W

- 6.3 100W–500W

- 6.4 >500W

Chapter 7 Market Estimates & Forecast, By Category, 2021-2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Isolated

- 7.3 Non-isolated

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 Avionics

- 8.3 Power distribution

- 8.4 Lighting systems

- 8.5 Radar & electronic warfare systems

- 8.6 In-flight entertainment (IFE)

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Technologies

- 10.2 Advanced Energy

- 10.3 AJ's Power Source Inc.

- 10.4 BrightLoop

- 10.5 Crane Aerospace & Electronics

- 10.6 Helios Power Solutions

- 10.7 Honeywell International Inc.

- 10.8 KGS Electronics

- 10.9 Meggitt PLC.

- 10.10 Murata Manufacturing Co., Ltd.

- 10.11 Pico Electronics

- 10.12 SynQor, Inc.

- 10.13 Tame-Power

- 10.14 TDK-Lambda Corporation

- 10.15 Texas Instruments Incorporated

- 10.16 Vicor Corporation

- 10.17 VPT, Inc.

- 10.18 XP Power