バイポーラ電気外科用デバイスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Bipolar Electrosurgical Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740822

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

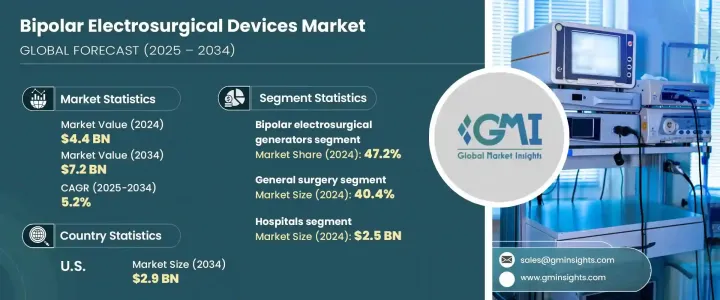

世界のバイポーラ電気外科用デバイス市場は、2024年には44億米ドルと評価され、CAGR 5.2%で成長し、2034年には72億米ドルに達すると推定されています。

低侵襲手術の需要が患者や外科医の間で高まる中、バイポーラ電気手術は現代の手術ワークフローに不可欠なものとなっています。こうした処置は、切開創の縮小、出血量の減少、退院時間の短縮、回復の早さなど、大きなメリットをもたらします。現在進行中の低侵襲アプローチへのシフトは、病院や外科センターにおけるバイポーラ電気外科技術の採用を大幅に増加させています。

バイポーラ電気外科器具は、周囲組織への危害を抑えながら、卓越した精度で切断と凝固の両方を行うように設計されています。そのため、術後の感染症や合併症の発生率が低くなります。血管シーリング機能の進歩、温度制御の改善、人間工学に基づいた器具の設計により、これらの器具は手術成績を向上させ続けています。精度と組織保全への注目の高まりは、神経外科、整形外科、婦人科などの外科分野での使用拡大を支え、市場拡大をさらに後押ししています。ロボットや腹腔鏡システムと互換性のある新しい機器の採用も、標準化された手術プロトコールでの地位を強化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 44億米ドル |

| 予測金額 | 72億米ドル |

| CAGR | 5.2% |

これらのデバイスは、バイポーラ構成を通じて印加される高周波電気エネルギーを用いて作動します。この場合、電流は2つの鉗子のような電極間の組織のみを流れます。この設計により、局所的なエネルギー供給と最小限の組織外傷が保証されます。市場は製品タイプによって区分され、カテゴリーにはバイポーラ電気外科用ジェネレーター、バイポーラ電気外科用器具、アクセサリーおよび消耗品が含まれます。このうち、バイポーラ電気外科用ジェネレーターは2024年に47.2%と最も高い売上シェアを占めています。これらのジェネレーターは、接続されたすべての器具やアクセサリーの中核となるエネルギー源として機能し、あらゆる電気外科セットアップに不可欠なものとなっています。再利用可能な器具や付属品に比べてコストが高いため、市場全体の収益に大きく貢献しています。

バイポーラ電気手術器具はさらに、鉗子、ハサミ、プローブまたは電極に分けられます。これらの器具は様々な外科手術に広く使用されているが、ジェネレーターに比べて価格が手ごろなため、このセグメントでは中堅レベルの収益貢献者となっています。ジェネレーターは資本集約的であり、システム機能にとって不可欠であるため、製品ベースのセグメンテーションでは支配的な地位を維持しています。

用途別では、一般外科、脳神経外科、心臓血管外科、婦人科外科、その他の専門分野に分類されます。一般外科は、2024年の市場シェア40.4%でセグメントをリードしています。胆嚢疾患、虫垂炎、ヘルニアなどの加齢に関連した疾患の有病率は、世界の高齢者人口の拡大とともに増加しています。高齢者は変性疾患や慢性疾患の頻度が高いため外科手術を受ける可能性が高く、バイポーラ装置のような信頼性が高く安全な手術器具の需要を押し上げています。出血を管理し、正確な切開を可能にする効率性により、一般外科で好んで使用されています。

エンドユーザー別では、市場は病院、外来手術センター、専門クリニック、学術・研究機関に区分されます。2024年の売上高は25億米ドルに達し、病院がこのセグメントを支配しています。患者の安全性を高め、手技の正確性を向上させ、回復時間を短縮することに重点を置いているため、先進的な手術機器への投資に拍車がかかっています。バイポーラ機器は、熱拡散の最小化、出血の減少、偶発的な火傷の減少などの主な利点を提供し、より良い臨床転帰と処置期間の短縮をサポートします。病院がロボットや腹腔鏡などの最先端手術システムと互換性のある機器へのアップグレードを続けているため、バイポーラ電気外科用デバイスの需要は増加すると予想されます。

地域別では、北米が市場動向の形成に極めて重要な役割を果たしています。米国だけのバイポーラ電気外科用デバイス市場は、2024年の18億米ドルから2034年には29億米ドルに増加すると予測されています。心血管障害、糖尿病、肥満などの生活習慣病が急増し、手術件数が増加しています。慢性疾患が蔓延するにつれ、効率的で精度の高い手術器具の必要性が高まっています。バイポーラ電気手術ユニットは、このような臨床需要に効果的に応え、米国のヘルスケア施設全体でその価値を高めています。

競合情勢としては、世界の企業と地域的な企業が混在し、高まる手術需要に対応したソリューションを提供しています。メドトロニック、ジョンソン・エンド・ジョンソン、B.ブラウン、ストライカー、オリンパスなどの主要企業は、合わせて世界市場の約65%を占めています。これらの企業は、先進国市場と新興国市場の双方で関連性を維持するために、継続的な技術革新、製品のカスタマイズ、価格戦略を通じて競争しています。コストに敏感な地域では、国内プレーヤーが手頃な価格で高品質の機器を提供することで多国籍ブランドに課題しており、世界リーダーは安全性と性能の基準への準拠を確保しながら、そのアプローチを適応させるよう促されています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 低侵襲手術の需要増加

- 慢性疾患と外科的介入の増加

- 電気外科機器の技術的進歩

- 外来手術センターの拡張

- 業界の潜在的リスク&課題

- 高度な電気外科システムの高コスト

- 火傷、神経損傷、手術による煙などの合併症のリスク

- 促進要因

- 成長可能性分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項トランプ政権の関税

- 貿易への影響

- 業界バリューチェーン分析

- 原材料分析

- 規制情勢

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 競合ダッシュボード

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- バイポーラ電気外科用発電機

- バイポーラ電気外科器具

- バイポーラ鉗子

- バイポーラシザーズ

- バイポーラプローブと電極

- アクセサリーと消耗品

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 一般外科

- 脳神経外科

- 婦人科手術

- 心臓血管外科

- その他の用途

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 外来手術センター

- 専門クリニック

- 学術研究機関

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- メキシコ

- ブラジル

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Applied Medical

- B Braun

- Boston Scientific

- Bovie Medical

- BOWA Medical

- ConMed

- Encision

- Erbe Elektromedizin

- Johnson and Johnson

- KLS Martin Group

- Medtronic

- Olympus

- Smith and Nephew

- Stryker

- Zimmer Biomet

目次

The Global Bipolar Electrosurgical Devices Market was valued at USD 4.4 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 7.2 billion by 2034. As the demand for minimally invasive procedures gains momentum among patients and surgeons alike, bipolar electrosurgery has become an integral part of modern surgical workflows. These procedures offer substantial benefits, including smaller incisions, reduced blood loss, quicker discharge times, and faster recovery. The ongoing shift towards minimally invasive approaches has significantly increased the adoption of bipolar electrosurgical technologies in hospitals and surgical centers.

Bipolar electrosurgical instruments are designed to perform both cutting and coagulation with exceptional precision while limiting harm to the surrounding tissue. This translates to a lower rate of post-operative infections and complications. With advancements in vessel sealing capabilities, improved thermal control, and ergonomic tool designs, these instruments continue to enhance procedural outcomes. The heightened focus on precision and tissue conservation supports their growing use in surgical fields such as neurosurgery, orthopedics, gynecology, and others, further driving market expansion. The adoption of newer devices compatible with robotic and laparoscopic systems also reinforces their position in standardized surgical protocols.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.4 Billion |

| Forecast Value | $7.2 Billion |

| CAGR | 5.2% |

These devices operate using high-frequency electrical energy applied through a bipolar configuration, where the current flows only through the tissue between two forceps-like electrodes. This design ensures localized energy delivery and minimal tissue trauma. The market is segmented based on product types, with categories including bipolar electrosurgical generators, bipolar electrosurgical instruments, and accessories and consumables. Among these, bipolar electrosurgical generators accounted for the highest revenue share at 47.2% in 2024. These generators act as the core energy source for all connected instruments and accessories, making them essential for any electrosurgical setup. Their high cost compared to reusable instruments and accessories contributes significantly to overall market revenue.

Bipolar electrosurgical instruments are further divided into forceps, scissors, and probes or electrodes. While these tools are widely used across various surgical procedures, their affordability relative to generators places them as mid-level revenue contributors within the segment. Generators, being capital-intensive and indispensable for system functionality, maintain a dominant hold on product-based segmentation.

Based on application, the market is categorized into general surgery, neurosurgery, cardiovascular surgery, gynecological surgery, and other specialized fields. General surgery led the segment with a market share of 40.4% in 2024. The prevalence of age-related conditions such as gallbladder disease, appendicitis, and hernias has grown alongside the expanding global elderly population. Older adults are more likely to undergo surgical procedures due to the higher frequency of degenerative and chronic illnesses, which boosts the demand for reliable and safe surgical tools like bipolar devices. Their efficiency in managing bleeding and enabling precise incisions makes them a preferred choice across general surgery departments.

By end user, the market is segmented into hospitals, ambulatory surgical centers, specialty clinics, and academic or research institutions. Hospitals dominated this segment, with revenue amounting to USD 2.5 billion in 2024. Their focus on enhancing patient safety, improving procedural accuracy, and reducing recovery time has spurred investments in advanced surgical equipment. Bipolar devices offer key advantages such as minimal thermal spread, reduced bleeding, and fewer accidental burns, supporting better clinical outcomes and shorter procedure durations. As hospitals continue to upgrade to equipment that is compatible with cutting-edge surgical systems, including robotics and laparoscopic tools, the demand for bipolar electrosurgical devices is expected to climb.

Regionally, North America plays a pivotal role in shaping market trends. The bipolar electrosurgical devices market in the United States alone is projected to rise from USD 1.8 billion in 2024 to USD 2.9 billion by 2034. A surge in lifestyle-related diseases, including cardiovascular disorders, diabetes, and obesity, has led to a growing number of surgeries. As chronic conditions become more prevalent, the need for efficient, precision-driven surgical instruments becomes more pressing. Bipolar electrosurgical units meet these clinical demands effectively, reinforcing their value across U.S. healthcare facilities.

The competitive landscape of the bipolar electrosurgical devices market features a blend of global and regional players offering tailored solutions to meet rising surgical demands. Leading companies such as Medtronic, Johnson & Johnson, B. Braun, Stryker, and Olympus together represent approximately 65% of the global market. These organizations compete through continuous innovation, product customization, and pricing strategies to maintain relevance across both developed and emerging markets. In cost-sensitive regions, domestic players challenge multinational brands by delivering affordable, quality devices, prompting global leaders to adapt their approach while ensuring compliance with safety and performance standards.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for minimally invasive surgeries

- 3.2.1.2 Rising prevalence of chronic diseases and surgical interventions

- 3.2.1.3 Technological advancements in electrosurgical devices

- 3.2.1.4 Expansion of outpatient surgical centers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced electrosurgical systems

- 3.2.2.2 Risk of complications such as burns, nerve damage, surgical smoke

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on the Industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook and future considerationsTrump administration tariffs

- 3.4.1 Impact on trade

- 3.5 Industry value chain analysis

- 3.6 Raw material analysis

- 3.7 Regulatory landscape

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive dashboard

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Bipolar electrosurgical generators

- 5.3 Bipolar electrosurgical instruments

- 5.3.1 Bipolar forceps

- 5.3.2 Bipolar scissors

- 5.3.3 Bipolar probes and electrodes

- 5.4 Accessories and consumables

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 General surgery

- 6.3 Neurosurgery

- 6.4 Gynecological surgery

- 6.5 Cardiovascular surgery

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty clinics

- 7.5 Academic and research institutes

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Applied Medical

- 9.2 B Braun

- 9.3 Boston Scientific

- 9.4 Bovie Medical

- 9.5 BOWA Medical

- 9.6 ConMed

- 9.7 Encision

- 9.8 Erbe Elektromedizin

- 9.9 Johnson and Johnson

- 9.10 KLS Martin Group

- 9.11 Medtronic

- 9.12 Olympus

- 9.13 Smith and Nephew

- 9.14 Stryker

- 9.15 Zimmer Biomet

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日