有機乾燥ディスティラーズグレイン飼料の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Organic Dried Distiller's Grain Feed Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740813

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

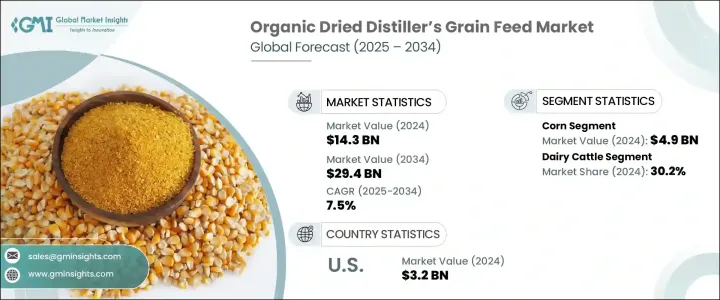

世界の有機乾燥ディスティラーズグレイン飼料市場は、2024年には143億米ドルと評価され、オーガニック畜産物に対する需要の高まりと、持続可能で環境に配慮した農業慣行への業界全体の後押しにより、CAGR 7.5%で成長し、2034年には294億米ドルに達すると推定されています。

消費者の嗜好がよりクリーンで倫理的な食品へと急速にシフトする中、畜産セクターは有機的で再生可能な飼料システムとの協調を強く求められています。有機DDGは、栄養ニーズと有機適合のギャップを埋める重要なソリューションとして、ますます台頭してきています。また、世界の貿易の混乱は、弾力性があり追跡可能なサプライチェーンの重要性を高めており、有機DDGを従来の飼料に代わる実行可能な選択肢としてさらに位置づけています。有機認証基準が強化され、動物福祉と持続可能性をめぐる認識が深まるにつれ、生産者は規制の期待と消費者の信頼の両方を満たすため、有機飼料投入を急速に採用しています。家禽から乳牛、肉牛に至るまで、畜産業界全体において、有機DDGは現在、栄養プログラムにおいて重要な原料となっており、性能の信頼性と有機認証との整合性の両方を提供しています。この成長軌道は、既存市場および新興市場における継続的な投資、規制枠組みの進化、インフラ開拓によって支えられています。

ここ数年、エタノール生産者が有機穀物投入にシフトし、生産施設の認証を求めるようになったため、有機認証DDGの供給量は大幅に増加しています。こうした開発は、持続可能で透明性の高い農業サプライ・チェーンに対する要求が新たな高みに達している時期に行われました。生産者と飼料メーカーは、持続可能性の目標と市場の需要の両方に合致する有機ソリューションの採用に、かつてないほど熱心に取り組んでいます。北米は、有機農業のエコシステムが確立されているため、市場導入において引き続きリードしています。しかし、アジア太平洋地域は、各国が有機生産モデルに投資し、認証と流通インフラを強化しているため、急速に追い上げています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 143億米ドル |

| 予測金額 | 294億米ドル |

| CAGR | 7.5% |

トウモロコシを主原料とする乾燥ディスティラーズ・グレインは、2024年に49億米ドルの収益を上げ、2034年までCAGR 7%で成長すると予測され、依然として支配的な原料です。トウモロコシは広く入手可能で、デンプン含量が高く、エタノール発酵効率が高いため、有機DDG生産に適した作物です。タンパク質とエネルギーが豊富なトウモロコシ由来のDDGの栄養密度は、有機畜産システムに特に適しています。この一貫性は、厳しい有機認証基準を満たすために高品質の飼料投入に依存している生産者にとって不可欠です。畜産生産者が引き続き栄養とコンプライアンスを優先しているため、トウモロコシベースのDDGは有機飼料分野でリーダーシップを維持すると予想されます。

動物への応用という点では、乳牛が最大の消費者セグメントです。2024年に43億米ドルと評価され、CAGR 7.8%で成長すると予測されるこのセグメントは、有機DDGが酪農の食事ニーズをサポートする上で重要な役割を担っていることを反映しています。合成添加物や抗生物質の使用を制限する有機酪農場では、タンパク質と食物繊維を自然に供給する有機DDGへの依存度が高まっています。これは、乳生産量の維持に役立つだけでなく、牛群全体の健康と活力をサポートします。有機乳製品への需要が世界的に高まるにつれ、栄養豊富で有機準拠の飼料の重要性は、この分野の中心的存在となるに違いないです。

米国の有機乾燥ディスティラーズグレイン飼料市場は2024年に32億米ドルを生み出し、CAGR 7.3%で成長すると予想されています。この成長の原動力となっているのは、再生農業への関心の高まりと、持続可能で透明性の高い畜産物を好む消費者の動向です。米国の飼料メーカーは、有機DDGをパフォーマンスと環境目標の両方をサポートする栄養計画に組み込むことで、迅速に適応しています。有機エタノール生産の製品別を再利用するという循環型農業における有機DDGの役割を考えると、生産性と持続可能性の両方を高めたいアメリカの生産者にとって、有機DDGは魅力的な選択肢になりつつあります。

Flint Hills Resources、Archer Daniels Midland Company(ADM)、Green Plains Inc.、POET LLC、Valero Energy Corporationなどの主要企業は、拡張と認証取得に積極的に投資しています。これらの主要企業は、有機基準を満たすために施設をアップグレードし、有機穀物サプライヤーと協力し、特定の家畜栄養要件に対応するために製品ラインをカスタマイズしています。戦略的パートナーシップと、トレーサビリティと透明性の重視の高まりは、進化する有機飼料の展望の中で長期的成長を目指すこれらの企業の市場戦略を定義し続けています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 供給側の影響(原材料)

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国、2021-2024

- 主要輸入国、2021-2024

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- オーガニック動物製品に対する消費者の需要の増加

- 有機畜産・養鶏の拡大

- 政府の支援と有機認証政策

- 持続可能で循環的な農業慣行の重視

- 業界の潜在的リスク&課題

- 認証された有機原料の入手が限られている

- 従来の飼料に比べて生産・加工コストが高め

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:ソース別、2021-2034

- 主要動向

- トウモロコシ

- 小麦

- 米

- 大麦

- ソルガム

- オート麦

- ライ麦

- キビ

- その他

第6章 市場推計・予測:動物の種類別、2021-2034

- 主要動向

- 乳牛

- 肉牛

- 豚

- 家禽

- アクア

- その他の動物の種類

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- 動物飼料

- バイオエネルギー生産

- 肥料と土壌改良剤

- その他

第8章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- オンライン

- オフライン

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Bayer Animal Health

- ADM

- Agrifeeds

- Alcogroup SA

- Chimique India

- COFCO Biochemical(Anhui)Co. Ltd.

- Feedpedia

- Furst-McNess Company

- Greenfield Global Inc.

- Gulshan Polyols Ltd.

- Kemin Industries、Inc.

- Midas Overseas

- Nutrigo Feeds Pvt Ltd

- Poet LLC

- Valero Energy Corporation

目次

The Global Organic Dried Distiller's Grain Feed Market was valued at USD 14.3 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 29.4 billion by 2034, driven by the rising demand for organic livestock products and an industry-wide push toward sustainable, eco-conscious farming practices. With consumer preferences rapidly shifting toward cleaner, ethically sourced food, the livestock sector is under mounting pressure to align with organic and regenerative feed systems. Organic DDGs are increasingly emerging as a key solution, bridging the gap between nutritional needs and organic compliance. Global trade disruptions have also heightened the importance of resilient, traceable supply chains-further positioning organic DDGs as a viable alternative to conventional feed. As organic certification standards tighten and awareness surrounding animal welfare and sustainability deepens, producers are rapidly adopting organic feed inputs to meet both regulatory expectations and consumer trust. Across the livestock industry, from poultry to dairy and beef cattle, organic DDGs are now a crucial ingredient in nutrition programs, offering both performance reliability and alignment with organic certifications. This growth trajectory is supported by continued investments, evolving regulatory frameworks, and infrastructure developments across established and emerging markets.

Over the past few years, the supply of certified organic DDGs has grown considerably, as ethanol producers shift toward organic grain inputs and seek certification for their production facilities. These developments come at a time when the demand for sustainable and transparent agricultural supply chains is reaching new heights. Producers and feed manufacturers are more eager than ever to embrace organic solutions that align with both sustainability goals and market demand. North America continues to lead in market adoption due to its well-established organic agriculture ecosystem. However, the Asia-Pacific region is quickly catching up, as countries invest in organic production models and enhance their certification and distribution infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.3 Billion |

| Forecast Value | $29.4 Billion |

| CAGR | 7.5% |

Corn-based dried distiller's grain remains the dominant feedstock, generating USD 4.9 billion in revenue in 2024 and projected to grow at a 7% CAGR through 2034. Corn's widespread availability, high starch content, and efficiency in ethanol fermentation make it a preferred crop for organic DDG production. The nutritional density of corn-derived DDGs, rich in protein and energy, also makes it especially well-suited for organic livestock systems. This consistency is vital for producers who rely on quality feed inputs to meet stringent organic certification standards. As livestock producers continue to prioritize nutrition and compliance, corn-based DDG is expected to retain its leadership in the organic feed segment.

In terms of animal application, dairy cattle represent the largest consumer segment. Valued at USD 4.3 billion in 2024 and forecasted to grow at a CAGR of 7.8%, this segment reflects the critical role that organic DDG plays in supporting the dietary needs of dairy operations. Organic dairy farms, which restrict the use of synthetic additives and antibiotics, increasingly rely on organic DDGs to deliver protein and fiber naturally. This not only helps maintain milk production levels but also supports overall herd health and vitality. As demand for organic dairy products grows globally, the importance of nutrient-rich, organically compliant feed will only become more central to the sector.

The United States Organic Dried Distiller's Grain Feed Market generated USD 3.2 billion in 2024 and is expected to grow at a 7.3% CAGR. This growth is fueled by increased interest in regenerative agriculture and consumer trends favoring sustainable, transparently sourced animal products. US feed manufacturers are adapting swiftly by integrating organic DDGs into nutrition plans that support both performance and environmental goals. Given their role in circular agriculture-repurposing by-products of organic ethanol production-organic DDGs are becoming an attractive choice for American producers looking to boost both productivity and sustainability.

Leading companies such as Flint Hills Resources, Archer Daniels Midland Company (ADM), Green Plains Inc., POET LLC, and Valero Energy Corporation are actively investing in expansion and certification. These key players are upgrading facilities to meet organic standards, collaborating with organic grain suppliers, and tailoring their product lines to cater to specific livestock nutrition requirements. Strategic partnerships and a growing emphasis on traceability and transparency continue to define the market strategies of these firms as they position themselves for long-term growth in the evolving organic feed landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-Side Impact (Raw Materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.1 Supply-Side Impact (Raw Materials)

- 3.2.3 Demand-Side Impact (Selling Price)

- 3.2.3.1 Price transmission to end markets

- 3.2.3.2 Market share dynamics

- 3.2.3.3 Consumer response patterns

- 3.2.4 Key companies impacted

- 3.2.5 Strategic industry responses

- 3.2.5.1 Supply chain reconfiguration

- 3.2.5.2 Pricing and product strategies

- 3.2.5.3 Policy engagement

- 3.2.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries, 2021-2024 (Kilo Tons)

- 3.3.2 Major importing countries, 2021-2024 (Kilo Tons)

- 3.4 Supplier landscape

- 3.5 Profit margin analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increasing consumer demand for organic animal products

- 3.8.1.2 Expansion of organic livestock and poultry farming

- 3.8.1.3 Government support and organic certification policies

- 3.8.1.4 Emphasis on sustainable and circular agricultural practices

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Limited availability of certified organic raw materials

- 3.8.2.2 High production and processing costs compared to conventional feed

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Corn

- 5.3 Wheat

- 5.4 Rice

- 5.5 Barley

- 5.6 Sorghum

- 5.7 Oats

- 5.8 Rye

- 5.9 Millet

- 5.10 Others

Chapter 6 Market Estimates & Forecast, By Animal Type, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dairy cattle

- 6.3 Beef cattle

- 6.4 Swine

- 6.5 Poultry

- 6.6 Aqua

- 6.7 Other animal types

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Animal feed

- 7.3 Bioenergy production

- 7.4 Fertilizers & Soil amendments

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Online

- 8.3 Offline

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Bayer Animal Health

- 10.2 ADM

- 10.3 Agrifeeds

- 10.4 Alcogroup SA

- 10.5 Chimique India

- 10.6 COFCO Biochemical (Anhui) Co. Ltd.

- 10.7 Feedpedia

- 10.8 Furst-McNess Company

- 10.9 Greenfield Global Inc.

- 10.10 Gulshan Polyols Ltd.

- 10.11 Kemin Industries, Inc.

- 10.12 Midas Overseas

- 10.13 Nutrigo Feeds Pvt Ltd

- 10.14 Poet LLC

- 10.15 Valero Energy Corporation

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日