|

市場調査レポート

商品コード

1740812

バルブ遠隔制御システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Valve Remote Control System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| バルブ遠隔制御システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月23日

発行: Global Market Insights Inc.

ページ情報: 英文 128 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

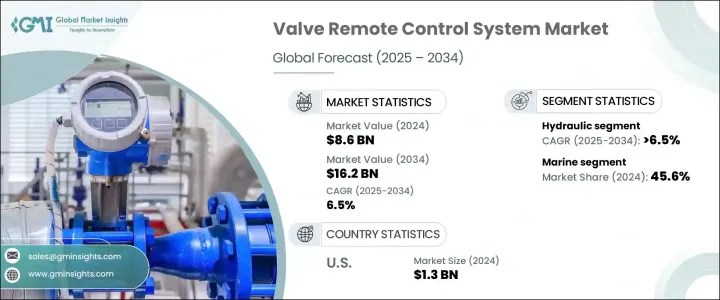

世界のバルブ遠隔制御システム市場は、2024年には86億米ドルと評価され、自動化技術の採用が増加し、緊急漏出防止と安全遵守における遠隔システムの重要な役割によって、CAGR 6.5%で成長し、2034年には162億米ドルに達すると予測されています。

これらのシステムは、パイプライン内の流体の流れを遮断し、対応時間を大幅に短縮し、環境および操業上の損害のリスクを最小限に抑える上で重要な役割を果たしています。あらゆる産業が業務効率、安全性、規制遵守を重視するようになるにつれ、堅牢でインテリジェントなバルブ制御ソリューションに対する需要は高まり続けています。

バルブの遠隔制御システムは、企業がインフラのスマート化やデジタルトランスフォーメーションを推進する上で不可欠なものとなっています。石油・ガス、海運、水処理、化学処理、公益事業などの業界は、リアルタイムの流体管理を強化し、手動介入への依存を減らすために、これらのシステムを採用しています。重要なオペレーションにおいて、より速く、より安全で、より応答性の高いシステムを求めるニーズが、自動バルブ技術への投資を後押ししています。異常気象、地政学的緊張、世界のエネルギー需要がインフラの回復力に更なる圧力をかける中、遠隔バルブ制御は説得力のある解決策を提供します。データ駆動がますます進む世界では、これらのシステムを産業用IoTプラットフォーム、SCADA、AIベースの予知保全ツールと統合する能力は、単なるボーナスではなく、急速に必需品になりつつあります。企業はまた、モジュール性、拡張性、サイバーセキュアな接続性を提供するソリューションを優先しており、従来の機械的操作からスマートで適応性の高い制御アーキテクチャへのシフトを示唆しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 86億米ドル |

| 予測金額 | 162億米ドル |

| CAGR | 6.5% |

この成長に拍車をかけている主な要因は、緊急遮断弁の採用です。緊急遮断弁は、オペレーターが数秒以内に問題箇所を隔離できるようにし、漏出やその他の大惨事の可能性を減らします。この技術的優位性は、ますます厳しくなる世界の安全規制と相まって、リスクの高い産業全体に広範なインフラのアップグレードを促しています。リモートバルブシステムは、安全なコントロールセンターからの集中操作を可能にするため、危険な遠隔環境での自動化を推進する動きは、市場の勢いをさらに加速させています。海運、石油化学精製、廃水処理など、精度とスピードが譲れない分野では、これらのシステムがミッションクリティカルな資産であることが証明されつつあります。

空気圧バルブ遠隔制御システム分野だけでも、2024年には15億米ドルの売上がありました。これらのシステムは、電気部品が安全上のリスクをもたらす可能性のある産業や、常時電源に頼らずに操業を続けなければならない産業で特に人気があります。圧縮空気で作動する空圧システムは、爆発性または腐食性の環境でも、高速で信頼性の高い作動を提供します。その機械的なシンプルさ、信頼性、適応性により、ダウンタイムを削減し、システムの安全性を高めたい施設に最適なソリューションとなっています。石油・ガス施設から工業製造プラント、海洋環境まで、空圧システムはリスクの高いシナリオにおいて耐久性のあるオプションを提供します。

用途別では、海洋分野が市場をリードし、2024年には45.6%の圧倒的シェアを獲得します。船舶、潜水艦、オフショアプラットフォームはすべて、燃料、バラスト、廃水システムの正確な管理を必要とするため、集中バルブ制御は有利なだけでなく不可欠なものとなっています。バルブ操作を自動化する能力は、手動介入を大幅に削減し、リアルタイムの意思決定をサポートし、船上の安全性を高めます。世界の海事オペレーターがよりインテリジェントな船舶運航を推し進める中、バルブ遠隔制御システムの需要は、特に古い船隊の近代化を目指した改造構想において高まり続けています。

米国のバルブ遠隔制御システム市場は2024年に13億米ドルを創出し、産業のアップグレードやインフラの近代化を原動力とする全国的な普及の勢いを反映しています。予知保全、デジタルモニタリング、スマートオートメーションが重視されるようになり、米国の産業界はこれらのシステムをより広範な運用プラットフォームに統合しつつあります。水道事業やエネルギー生産から重工業や海運に至るまで、企業は安全性の向上、人件費の削減、迅速な緊急対応のためにバルブの遠隔操作を活用しています。

Velan、Honeywell International、HAWE Hydraulik、Rotork、Emerson Electric、Flowserve、Valmet、KSB SE、Mowe Marine &Offshore、ATHENA ENGINEERINGといった業界の主要企業は、高度な自動化技術に多額の投資を行っています。彼らの戦略には、モジュール式でスケーラブルなシステム設計の開発、生産能力の増強、サイバーに強い通信プロトコルの確保、ニッチなバルブ技術プロバイダーの買収による市場拡大と製品提供の拡大などが含まれます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:タイプ別、2021-2034

- 主要動向

- 油圧式

- 空気圧

- 電気

- 電気油圧式

第6章 市場規模・予測:製品別、2021-2034

- 主要動向

- ボールバルブ

- グローブバルブ

- バタフライバルブ

- ゲートバルブ

- ダイヤフラムバルブ

- プラグバルブ

- チェックバルブ

- 安全弁

第7章 市場規模・予測:用途別、2021-2034

- 主要動向

- 海洋

- 発電

- 製油所

- 水と廃水処理

- 化学薬品

- その他

第8章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- マレーシア

- インドネシア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- オマーン

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第9章 企業プロファイル

- ATHENA ENGINEERING

- Emerson Electric

- Flowserve

- HAWE Hydraulik

- Honeywell International

- Hoppe Marine

- kdu

- KSB SE

- Mingda Valve

- Mowe Marine &Offshore

- Nantong Navigation Machinery

- Navalimpianti

- Rotork

- Schubert &Salzer Control Systems

- SPX FLOW

- Valmet

- ValvTechnologies

- Velan

- Wartsila

The Global Valve Remote Control System Market was valued at USD 8.6 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 16.2 billion by 2034, driven by the increasing adoption of automation technologies and the critical role of remote systems in emergency leak prevention and safety compliance. These systems play a vital role in shutting down fluid flow in pipelines, drastically reducing response times and minimizing the risk of environmental and operational damage. As industries across the board place growing emphasis on operational efficiency, safety, and regulatory compliance, the demand for robust and intelligent valve control solutions continues to rise.

Valve remote control systems are becoming indispensable as companies push toward smarter infrastructure and digital transformation. Industries such as oil and gas, maritime, water treatment, chemical processing, and utilities are embracing these systems to enhance real-time fluid management and reduce reliance on manual intervention. The need for faster, safer, and more responsive systems in critical operations is propelling investments in automated valve technologies. As extreme weather events, geopolitical tensions, and global energy demand place further pressure on infrastructure resilience, remote valve control offers a compelling solution. In an increasingly data-driven world, the ability to integrate these systems with industrial IoT platforms, SCADA, and AI-based predictive maintenance tools is not just a bonus-it's fast becoming a necessity. Businesses are also prioritizing solutions that offer modularity, scalability, and cyber-secure connectivity, signaling a shift from traditional mechanical operations to smart, adaptive control architectures.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.6 Billion |

| Forecast Value | $16.2 Billion |

| CAGR | 6.5% |

A key factor fueling this growth is the adoption of emergency shut-off valves that empower operators to isolate problem areas within seconds, reducing the likelihood of leaks and other catastrophic failures. This technological advantage, paired with increasingly stringent global safety regulations, is prompting widespread infrastructure upgrades across high-risk industries. The drive toward automation in hazardous and remote environments has further accelerated market momentum, as remote valve systems allow centralized operation from safe control centers. In sectors like marine shipping, petrochemical refining, and wastewater treatment-where precision and speed are non-negotiable-these systems are proving to be mission-critical assets.

The pneumatic valve remote control systems segment alone generated USD 1.5 billion in 2024. These systems are especially popular in industries where electrical components may pose safety risks or where operations must continue without reliance on constant power sources. Operating on compressed air, pneumatic systems offer fast, dependable actuation even in explosive or corrosive settings. Their mechanical simplicity, reliability, and adaptability make them a go-to solution for facilities looking to reduce downtime and enhance system safety. From oil and gas facilities to industrial manufacturing plants and marine environments, pneumatic systems provide a durable option in high-risk scenarios.

Within the application landscape, the marine sector leads the market, capturing a dominant 45.6% share in 2024. Ships, submarines, and offshore platforms all require precise management of fuel, ballast, and wastewater systems, making centralized valve control not only advantageous but essential. The ability to automate valve operations significantly reduces manual intervention, supports real-time decision-making, and enhances onboard safety. As global maritime operators push for more intelligent vessel operations, the demand for valve remote control systems continues to rise, especially in retrofitting initiatives aimed at modernizing older fleets.

The U.S. Valve Remote Control System Market generated USD 1.3 billion in 2024, reflecting strong nationwide adoption driven by industrial upgrades and infrastructure modernization. With a growing emphasis on predictive maintenance, digital monitoring, and smart automation, U.S. industries are integrating these systems into broader operational platforms. From water utilities and energy production to heavy industry and shipping, companies are leveraging remote valve actuation to improve safety, reduce labor costs, and ensure faster emergency response.

Key industry players-including Velan, Honeywell International, HAWE Hydraulik, Rotork, Emerson Electric, Flowserve, Valmet, KSB SE, Mowe Marine & Offshore, and ATHENA ENGINEERING-are investing heavily in advanced automation technologies. Their strategies include developing modular and scalable system designs, boosting production capacity, securing cyber-resilient communication protocols, and acquiring niche valve technology providers to expand their market reach and product offerings.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Hydraulic

- 5.3 Pneumatic

- 5.4 Electric

- 5.5 Electro-hydraulic

Chapter 6 Market Size and Forecast, By Product, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Ball valve

- 6.3 Globe valve

- 6.4 Butterfly valve

- 6.5 Gate valve

- 6.6 Diaphragm valve

- 6.7 Plug valve

- 6.8 Check valve

- 6.9 Safety valve

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Marine

- 7.3 Power generation

- 7.4 Refinery

- 7.5 Water and wastewater treatment

- 7.6 Chemical

- 7.7 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 Malaysia

- 8.4.6 Indonesia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Oman

- 8.5.4 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 ATHENA ENGINEERING

- 9.2 Emerson Electric

- 9.3 Flowserve

- 9.4 HAWE Hydraulik

- 9.5 Honeywell International

- 9.6 Hoppe Marine

- 9.7 kdu

- 9.8 KSB SE

- 9.9 Mingda Valve

- 9.10 Mowe Marine & Offshore

- 9.11 Nantong Navigation Machinery

- 9.12 Navalimpianti

- 9.13 Rotork

- 9.14 Schubert & Salzer Control Systems

- 9.15 SPX FLOW

- 9.16 Valmet

- 9.17 ValvTechnologies

- 9.18 Velan

- 9.19 Wartsila