|

市場調査レポート

商品コード

1740803

水なし染色技術の市場機会、成長促進要因、産業動向分析、2025~2034年予測Waterless Dyeing Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 水なし染色技術の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年04月25日

発行: Global Market Insights Inc.

ページ情報: 英文 250 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

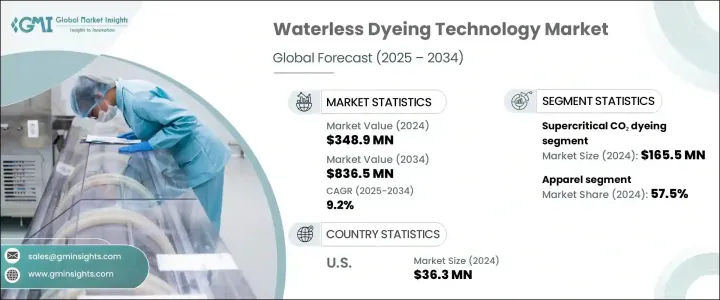

水なし染色技術の世界市場は、2024年には3億4,890万米ドルとなり、CAGR 9.2%で成長し、2034年には8億3,650万米ドルに達すると予測されています。

この技術を取り巻く関心の高まりは、特に過剰な水の消費と汚染で悪名高い業界において、環境に配慮した特性と強く結びついています。従来の繊維染色法は、淡水の大量使用と有毒な廃水により、最も資源集約的で環境破壊的な手法のひとつであり続けています。水不足や汚染、気候変動に対する世界の懸念が強まるなか、繊維産業はより持続可能な代替手段への転換を迫られています。水なし染色技術は、環境への影響を軽減するだけでなく、よりクリーンな生産方法に対する消費者と規制当局の両方の需要の高まりに応える、将来を見据えたソリューションを提供します。繊維製造におけるよりクリーンな技術の開発は、戦略上不可欠なものとなりつつあります。染色時の水の必要性をなくす、あるいは大幅に削減する技術革新は、大きな支持を集めています。世界の意識の高まりと規制の圧力に対応するため、メーカーは、排出量の削減、効率の向上、ウォーターフットプリントの削減を約束する、より持続可能な手法を採用しつつあります。

水なし染色技術市場は、技術タイプ別に超臨界CO2染色、空気染色、その他に区分されます。このうち、超臨界CO2染色は、2024年の市場規模が1億6,550万米ドルで、このセグメントを支配しており、予測期間中のCAGRは約9.9%で成長すると予想されています。この方法は、水や刺激の強い化学薬品を使わずに染料を繊維に運ぶ能力で際立っています。超臨界状態の二酸化炭素を使用するため、繊維に深く浸透し、効率的に色を吸収することができます。このプロセスは、廃水排出を大幅に削減し、染色作業を合理化します。この技術は、ブランドが持続可能性の基準を満たし、環境フットプリントを削減することを目指しているため、ますます採用が進んでいます。企業がグリーン・イニシアティブに沿ったより効率的な製造工程を目指す中、高度な染色システムの需要は伸び続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 3億4,890万米ドル |

| 予測金額 | 8億3,650万米ドル |

| CAGR | 9.2% |

用途別では、市場はアパレル、ホームテキスタイル、工業用テキスタイル、テクニカルテキスタイルに分けられます。アパレル分野は57.5%のシェアで市場をリードし、2025年から2034年までのCAGRは9.5%と予測されます。ファッション分野での環境に配慮した生産の必要性が、この成長に重要な役割を果たしています。衣料用に生産される膨大な量の繊維製品と汚染削減の緊急性を考えると、無水染色は実行可能でインパクトのある解決策を提示しています。環境への影響がしばしば批判されるファッション業界は、現在、水の使用をなくし、工程における有害物質の存在を減らす技術を積極的に模索しています。特にアパレル製造では、水を代替溶剤に置き換えたり、非液体アプローチに頼ったりする染色技術が好まれるようになっています。

繊維の種類別に分類すると、市場には綿、ポリエステル、ナイロン、ビスコース、リネン、その他が含まれます。ポリエステルは2024年に圧倒的な繊維タイプとして浮上し、予測期間中も主導的地位を維持すると予想されます。手頃な価格で弾力性があり、広く使用されていることで知られるポリエステルは、水なし染色法から多大な恩恵を受けています。従来のポリエステル染色には、高温、大量の水、さまざまな有害物質が必要でした。対照的に、水なし染色、特に超臨界CO2を使用した染色では、染料分子を効率的に浸透させることができ、堅牢度が向上し、化学薬品の使用量も最小限に抑えられます。これらの利点により、水なし染色は特に現代の繊維製造工程に適しています。

地域別では、米国が2024年に3,630万米ドルの評価額で北米市場をリードし、予測期間中にCAGR 9.8%で成長すると予測されています。この成長の主因は、環境規制の強化と従来の繊維染色慣行の改革への取り組みです。持続可能性が繊維政策の中核となるにつれ、製造業者は水の使用量を削減し、排出を最小限に抑え、より厳しい基準に準拠するソリューションを採用するよう、ますます強く求められています。このため、繊維セクターでは、よりクリーンな技術や循環型経済へのアプローチへの全国的なシフトが促されています。

水なし染色技術業界は、水の使用量と有毒廃棄物を削減する超臨界CO2染色やプラズマ治療などのイノベーションを通じて進歩しています。DyeCO2のような主要企業は、廃水処理コストを削減する環境に優しいソリューションを推進しています。業界が循環型経済の実践へとシフトする中、動向にはエネルギー効率の高いモジュール式染色、リサイクル可能な素材、カーボンニュートラルなどが含まれます。エシカルファッションの需要の高まり、規制の強化、協力体制の強化は、持続可能な実践を加速させ、繊維サプライチェーン全体で水なし染色技術の採用を後押ししています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- サプライヤーの情勢

- 貿易分析

- 利益率分析

- 技術概要

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 環境の持続可能性に関する懸念

- 規制圧力とコンプライアンス

- 持続可能な製品に対する消費者の需要

- 世界パートナーシップと業界連携

- 業界の潜在的リスク&課題

- 初期資本投資額が高め

- 生地の互換性が限られている

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:技術種別、2021-2034

- 主要動向

- 超臨界CO2染色

- 空気染色

- その他

第6章 市場推計・予測:繊維の種類別、2021-2034

- 主要動向

- コットン

- ポリエステル

- ナイロン

- ビスコース

- リネン

- その他

第7章 市場推計・予測:用途別、2021-2034

- 主要動向

- 衣服

- ホームテキスタイル

- 産業用繊維

- テクニカルテキスタイル

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 繊維メーカー

- ファッションブランド

- 化学薬品および染料メーカー

第9章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 直接

- 間接的

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- AirDye

- Alchemie Technology

- Archroma

- Deven Supercriticals Pvt. Ltd

- DMS Dilmenler Makina ve Tekstil San. Tic. A.S..

- DyeCoo

- eCO2Dye

- Guangdong Exponent Envirotech Ltd.

- HISAKA WORKS、LTD

- Kingfull Machinery CO2 Ltd

- Kornit Digital

- NTX

- Shanghai Singularity Imp&exp Company Limited

- Twine Solutions

- Xefco Pty Ltd

The Global Waterless Dyeing Technology Market was valued at USD 348.9 million in 2024 and is estimated to grow at a CAGR of 9.2% to reach USD 836.5 million by 2034. The surge in interest surrounding this technology is strongly linked to its environmentally conscious attributes, especially in an industry notorious for its excessive water consumption and pollution. Conventional textile dyeing methods continue to be among the most resource-intensive and environmentally damaging due to the heavy use of freshwater and the toxic wastewater they produce. As global concerns over water scarcity, pollution, and the broader implications of climate change intensify, the textile industry is being pushed to shift toward more sustainable alternatives. Waterless dyeing technology offers a forward-looking solution that not only helps reduce environmental impact but also meets the growing demand from both consumers and regulators for cleaner production methods. The development of cleaner technologies in textile manufacturing is becoming a strategic imperative. Innovations that eliminate or drastically reduce the need for water during dyeing are gaining significant traction. In response to increasing global awareness and regulatory pressure, manufacturers are embracing more sustainable practices that promise lower emissions, higher efficiency, and reduced water footprints.

The waterless dyeing technology market is segmented by technology type into supercritical CO2 dyeing, air dyeing, and others. Among these, supercritical CO2 dyeing dominated the segment with a market value of USD 165.5 million in 2024 and is expected to grow at a CAGR of approximately 9.9% during the forecast period. This method stands out for its ability to carry dyes into fibers without using water or harsh chemicals. It employs carbon dioxide in its supercritical state, which allows for deep fiber penetration and efficient color absorption. The appeal lies in its eco-friendly nature, high dye uptake, lower energy use, and recyclability of CO2 ,This process significantly cuts down on wastewater discharge and streamlines dyeing operations. The technology is increasingly being adopted as brands aim to meet sustainability benchmarks and reduce their environmental footprints. As companies aim for more efficient manufacturing processes that align with green initiatives, the demand for advanced dyeing systems continues to grow.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $348.9 Million |

| Forecast Value | $836.5 Million |

| CAGR | 9.2% |

In terms of application, the market is divided into apparel, home textiles, industrial textiles, and technical textiles. The apparel segment led the market with a 57.5% share and is projected to grow at a CAGR of 9.5% from 2025 to 2034. The need for eco-conscious production in the fashion sector is playing a key role in this growth. Given the massive volume of textiles produced for clothing and the urgency to reduce pollution, waterless dyeing presents a viable and impactful solution. The fashion industry, often criticized for its environmental impact, is now actively seeking technologies that eliminate the use of water and reduce the presence of hazardous substances in its processes. Dyeing techniques that replace water with alternative solvents or rely on non-liquid approaches are gaining preference, particularly in apparel manufacturing.

When segmented by fiber type, the market includes cotton, polyester, nylon, viscose, linen, and others. Polyester emerged as the dominant fiber type in 2024 and is expected to maintain its leading position throughout the forecast period. Known for its affordability, resilience, and widespread usage, polyester benefits immensely from waterless dyeing methods. Traditional polyester dyeing requires high temperatures, large volumes of water, and various harmful substances. In contrast, waterless dyeing-especially using supercritical CO2-allows for efficient penetration of dye molecules, better color fastness, and minimal chemical usage. These advantages make it particularly well-suited for modern textile manufacturing processes.

Regionally, the United States led the North American market with a valuation of USD 36.3 million in 2024 and is anticipated to grow at a CAGR of 9.8% during the forecast period. This growth is largely driven by mounting environmental regulations and efforts to reform conventional textile dyeing practices. As sustainability becomes a core aspect of textile policies, manufacturers are under increasing pressure to adopt solutions that reduce water usage, minimize emissions, and comply with stricter standards. This has encouraged a nationwide shift toward cleaner technologies and a circular economy approach within the textile sector.

The waterless dyeing technology industry is advancing through innovations like supercritical CO2 dyeing and plasma treatments, which reduce water usage and toxic waste. Leading companies such as DyeCO2 drive eco-friendly solutions that cut wastewater treatment costs. As the industry shifts toward circular economy practices, trends include energy-efficient modular dyeing, recyclable materials, and carbon neutrality. Growing ethical fashion demand, stricter regulations, and enhanced collaboration are accelerating sustainable practices and boosting adoption of waterless dyeing technologies across the textile supply chain.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-Side impact (Raw Materials)

- 3.2.2.2 Price volatility in key materials

- 3.2.2.3 Supply chain restructuring

- 3.2.2.4 Production cost implications

- 3.2.2.5 Demand-Side impact (Selling Price)

- 3.2.2.6 Price transmission to end markets

- 3.2.2.7 Market share dynamics

- 3.2.2.8 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Trade analysis

- 3.5 Profit margin analysis

- 3.6 Technological overview

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Environmental sustainability concerns

- 3.9.1.2 Regulatory pressures and compliance

- 3.9.1.3 Consumer demand for sustainable products

- 3.9.1.4 Global partnerships & industry collaboration

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial capital investment

- 3.9.2.2 Limited fabric compatibility

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology Type, 2021 - 2034 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Supercritical CO2 dyeing

- 5.3 Air dyeing

- 5.4 Others

Chapter 6 Market Estimates & Forecast, By Fiber Type, 2021 - 2034 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Cotton

- 6.3 Polyester

- 6.4 Nylon

- 6.5 Viscose

- 6.6 Linen

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Apparel

- 7.3 Home textiles

- 7.4 Industrial textiles

- 7.5 Technical textiles

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Textile manufacturers

- 8.3 Fashion brands

- 8.4 Chemical & dye producers

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AirDye

- 11.2 Alchemie Technology

- 11.3 Archroma

- 11.4 Deven Supercriticals Pvt. Ltd

- 11.5 DMS Dilmenler Makina ve Tekstil San. Tic. A.S..

- 11.6 DyeCoo

- 11.7 eCO2Dye

- 11.8 Guangdong Exponent Envirotech Ltd.

- 11.9 HISAKA WORKS, LTD

- 11.10 Kingfull Machinery CO2 Ltd

- 11.11 Kornit Digital

- 11.12 NTX

- 11.13 Shanghai Singularity Imp&exp Company Limited

- 11.14 Twine Solutions

- 11.15 Xefco Pty Ltd