脳梗塞治療市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Cerebral Infarction Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740797

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

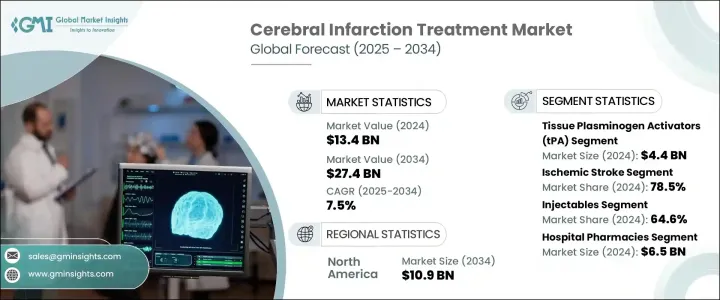

脳梗塞治療の世界市場規模は2024年に134億米ドルとなり、CAGR 7.5%で成長し、2034年には274億米ドルに達すると予測されています。

この市場は、脳卒中の有病率の増加と適時治療の重要性に対する意識の高まりにより、着実な成長を遂げています。脳梗塞は、脳への血流の途絶によって引き起こされる脳卒中の一種であり、組織の損傷につながり、治療せずに放置すると長期的な身体障害や死亡につながる可能性があります。この血流障害は通常、血栓が血管を塞ぎ、脳細胞から酸素と必須栄養素を奪うことによって引き起こされます。医療インフラと診断能力が世界的に向上するにつれ、早期発見とより効果的な治療が可能になり、治療介入への需要が高まっています。さらに、臨床研究の進歩や神経疾患に対する助成金の増加により、革新的な治療法や治療オプションの開発が加速し、市場拡大の原動力となっています。老年人口が増加し、高血圧や糖尿病などの危険因子が急増する中、より迅速で効果的な脳梗塞治療に対する需要は高まり続けています。救急医療システムと迅速な対応可能な治療オプションの出現は、患者の転帰に大きく影響しており、市場の長期的な可能性を後押ししています。

薬剤クラス別では、組織プラスミノーゲン活性化薬(tPA)、抗凝固薬、抗血小板薬、抗けいれん薬、その他の薬剤に区分されます。2023年の総市場収益は126億米ドル。2024年にはtPA分野だけで44億米ドルの売上があり、予測期間を通じてCAGR 7.8%で成長すると予想されています。組織プラスミノーゲン活性化薬は、血栓形成に関与するコアタンパク質であるフィブリンを分解することで血栓を溶解し、脳への血流を再確立し、酸素喪失に関連する損傷を最小限に抑えます。発症から数時間以内にtPAを投与することで、回復が著しく促進され、障害が軽減され、全体的な治療成績が向上することが示されています。これらの治療法は、その効率性と長期的な神経障害を軽減する能力から、現在では緊急脳卒中プロトコルに不可欠なものと考えられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 134億米ドル |

| 予測金額 | 274億米ドル |

| CAGR | 7.5% |

市場をタイプ別に分類すると、虚血性脳卒中と出血性脳卒中に分けられます。虚血性脳卒中は、2024年の売上高が105億米ドルで、市場全体の78.5%を占め、このセグメントを支配しています。この優位性は、虚血性脳卒中の世界的発生率が他のタイプと比較して高いことに起因しています。血栓溶解療法や血栓除去術のような治療は、血流を回復させ神経障害を抑えるためにますます採用されるようになっています。抗血小板薬(アスピリン、クロピドグレル)や抗凝固薬(ダビガトラン、リバーロキサバンなど)などの薬物療法は、特に心血管危険因子を有する患者において、再発予防のために日常的に処方されています。早期治療は、運動、言語、認知の回復を大幅に改善し、長期的な障害の可能性を低減させるため、市場の成長を支えています。

投与経路に基づき、市場は経口療法と注射療法に区分されます。2024年の市場全体では、注射剤が64.6%と大きなシェアを占めています。これらの治療薬は、脳卒中の急性期治療に不可欠な速効性と正確な投与量制御により、救急現場で支持されています。静脈内投与により、ヘルスケアプロバイダーは血栓溶解薬を迅速に血流に直接送り込むことができ、一刻を争う緊急時に迅速な治療効果が得られます。救急車や病院での使用に適していることから、最新の脳卒中治療システムにおける注射剤の価値が高まり、即時介入戦略の要となっています。

流通チャネル別では、病院薬局が2024年に最大の売上シェアを占め、65億米ドルを生み出しました。このような環境では、医師の管理下で救命薬に直接アクセスできるため、特に緊急性を要する治療には重要です。病院薬局はまた、薬の種類、投与方法、副作用に関するガイダンスを提供するなど、患者教育においても重要な役割を果たしています。ヘルスケアチームとの連携により、治療計画の遵守率が向上し、患者の転帰が改善されます。さらに、投薬管理やサポートプログラムなどのサービスは、長期的な治療の成功を促進します。

地域別では、北米が主要市場の地位を占めており、2024年の売上高は54億米ドル、2034年には109億米ドルに達すると予測されています。米国が最大の貢献者で、2023年の売上高は47億米ドルでした。同地域の高いヘルスケア支出、高度な医療インフラ、脳卒中治療に対する意識の高まりが、同地域の支配的地位を維持しています。この地域では心血管疾患の罹患率が高まっており、効果的な治療に対するニーズがさらに高まっています。

市場全体の約45%を占める主要企業には、アボット・ラボラトリーズ、ベーリンガーインゲルハイム、F.ホフマン・ラ・ロシュ、ノボ・ノルディスクなどの企業が含まれます。これらの企業は、戦略的な製品イノベーション、強固な流通網、規制に関する専門知識を通じて、市場をリードし続けています。ヘルスケア機関や公衆衛生機関とのパートナーシップは、研究活動を促進し、治療へのアクセスを向上させています。また、啓発キャンペーンやデジタル・プラットフォームの影響力の高まりも、より多くの人々が適時に治療を受けることを促し、市場の成長に寄与しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 心血管疾患の有病率の上昇

- 医薬品開発におけるイノベーション

- 脳卒中治療薬の研究開発の強化

- 高齢者人口の増加

- 業界の潜在的リスク&課題

- 薬の副作用

- 厳格な規制枠組み

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 国別の対応

- 業界への影響

- 供給側の影響(製造コスト)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(消費者のコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(製造コスト)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- パイプライン分析

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:薬剤クラス別、2021-2034

- 主要動向

- 組織プラスミノーゲン活性化因子(tPA)

- 抗凝固薬

- 抗血小板薬

- 抗けいれん薬

- その他の薬物クラス

第6章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- 虚血性脳卒中

- 出血性脳卒中

第7章 市場推計・予測:投与経路別、2021-2034

- 主要動向

- オーラル

- 注射剤

第8章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 病院薬局

- 小売薬局

- オンライン薬局

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Abbott Laboratories

- Amgen

- Amneal Pharmaceuticals

- AstraZeneca

- Boehringer Ingelheim

- Bayer

- Biogen

- Daiichi Sankyo Company

- F. Hoffmann-La Roche

- Merck &Co.

- Novartis

- Novo Nordisk

- Otsuka Holdings

- Pfizer

- Sanofi

目次

The Global Cerebral Infarction Treatment Market was valued at USD 13.4 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 27.4 billion by 2034. This market is witnessing steady growth due to the increasing prevalence of stroke and rising awareness about the importance of timely treatment. Cerebral infarction, a form of stroke caused by an interruption in blood flow to the brain, leads to tissue damage and, if left untreated, can result in long-term disability or death. This interruption is typically caused by a blood clot blocking a vessel, depriving brain cells of oxygen and essential nutrients. As medical infrastructure and diagnostic capabilities improve globally, earlier detection and more effective treatments are becoming available, pushing the demand for therapeutic interventions. Additionally, advances in clinical research and increased funding for neurological disorders are accelerating the development of innovative therapies and treatment options, driving market expansion. With a growing geriatric population and a surge in risk factors like hypertension and diabetes, the demand for more responsive and effective cerebral infarction treatments continues to climb. The emergence of emergency care systems and rapid-response treatment options has significantly influenced patient outcomes, thus boosting the market's long-term potential.

By drug class, the cerebral infarction treatment market is segmented into tissue plasminogen activators (tPA), anticoagulants, antiplatelets, anticonvulsants, and other drugs. The total market revenue for 2023 was USD 12.6 billion. The tPA segment alone generated USD 4.4 billion in 2024 and is expected to grow at a CAGR of 7.8% throughout the forecast period. Tissue plasminogen activators help dissolve blood clots by breaking down fibrin, a core protein involved in clot formation, thus reestablishing blood flow to the brain and minimizing oxygen loss-related damage. Administering tPA within the first few hours of symptom onset has been shown to significantly improve recovery, reduce disability, and enhance overall treatment outcomes. These therapies are now considered essential in emergency stroke protocols due to their efficiency and ability to reduce long-term neurological impairment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.4 Billion |

| Forecast Value | $27.4 Billion |

| CAGR | 7.5% |

When categorized by type, the market is divided into ischemic stroke and hemorrhagic stroke. Ischemic stroke dominated the segment with a revenue of USD 10.5 billion in 2024, accounting for 78.5% of the total market. This dominance is attributed to the high global incidence of ischemic strokes compared to other types. Treatments like thrombolysis and thrombectomy are increasingly adopted to restore blood flow and limit neurological damage. Medications such as antiplatelets (aspirin, clopidogrel) and anticoagulants (including dabigatran and rivaroxaban) are routinely prescribed to prevent recurrence, particularly in patients with underlying cardiovascular risk factors. Early treatment greatly improves motor, speech, and cognitive recovery, which helps reduce the chances of long-term disability, thereby supporting market growth.

Based on the route of administration, the market is segmented into oral and injectable therapies. Injectables accounted for a significant 64.6% share of the total market in 2024. These therapies are favored in emergency settings due to their fast action and precise dosage control, essential for acute stroke treatment. Intravenous administration allows healthcare providers to quickly deliver clot-dissolving medications directly into the bloodstream, providing rapid therapeutic effects when time is critical. Their suitability in ambulances and hospital environments enhances their value in modern stroke care systems, making injectables a cornerstone of immediate intervention strategies.

In terms of distribution channels, hospital pharmacies held the largest revenue share in 2024, generating USD 6.5 billion. These settings offer direct access to life-saving drugs under medical supervision, particularly important for treatments requiring urgent attention. Hospital pharmacies also play a key role in patient education, offering guidance on medication types, administration methods, and side effects. Their integration with healthcare teams ensures better adherence to treatment plans, improving patient outcomes. Additionally, services such as medication management and support programs foster long-term treatment success.

Regionally, North America emerged as a leading market, with a revenue of USD 5.4 billion in 2024 and a projected rise to USD 10.9 billion by 2034. The United States was the largest contributor, with USD 4.7 billion in revenue in 2023. The region's high healthcare expenditure, advanced medical infrastructure, and increased awareness about stroke care have helped it maintain its dominant position. The growing incidence of cardiovascular conditions in this region further fuels the need for effective treatments.

Key market players-accounting for roughly 45% of the total share-include companies such as Abbott Laboratories, Boehringer Ingelheim, F. Hoffmann-La Roche, and Novo Nordisk. These companies continue to lead the market through strategic product innovations, robust distribution networks, and regulatory expertise. Partnerships with healthcare institutions and public health organizations are facilitating research efforts and improving treatment accessibility. Awareness campaigns and the growing influence of digital platforms are also encouraging more individuals to seek timely treatment, thus contributing to market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cardiovascular diseases

- 3.2.1.2 Innovation in drug development

- 3.2.1.3 Increasing R&D for stroke therapeutics

- 3.2.1.4 Growing number of geriatric population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Adverse effects of medications

- 3.2.2.2 Stringent regulatory framework

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of Manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to Consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of Manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Pipeline analysis

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Tissue plasminogen activators (tPA)

- 5.3 Anticoagulants

- 5.4 Antiplatelets

- 5.5 Anticonvulsants

- 5.6 Other drug classes

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Ischemic stroke

- 6.3 Hemorrhagic stroke

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 Amgen

- 10.3 Amneal Pharmaceuticals

- 10.4 AstraZeneca

- 10.5 Boehringer Ingelheim

- 10.6 Bayer

- 10.7 Biogen

- 10.8 Daiichi Sankyo Company

- 10.9 F. Hoffmann-La Roche

- 10.10 Merck & Co.

- 10.11 Novartis

- 10.12 Novo Nordisk

- 10.13 Otsuka Holdings

- 10.14 Pfizer

- 10.15 Sanofi

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日