乾燥ベビーフードの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Dried Baby Food Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 300 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740793

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

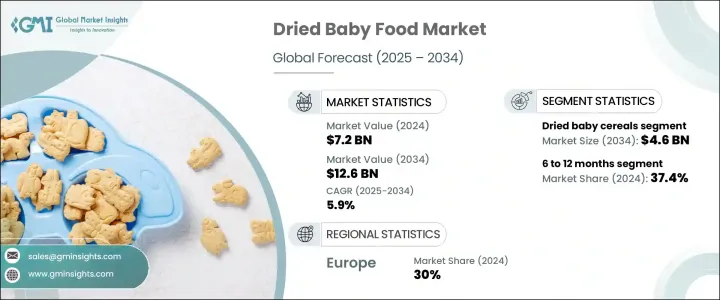

乾燥ベビーフードの世界市場は、2024年に72億米ドルと評価され、2034年にはCAGR 5.9%で成長し、126億米ドルに達すると予測されています。

多忙なライフスタイル、可処分所得の増加、乳幼児の健康に対する保護者の意識の高まりが、先進地域と開発途上地域の需要を押し上げています。親が乾燥ベビーフードを選ぶ理由は、保存期間の長さ、利便性、栄養価の高さです。市場の歴史的な拡大は、特に時間の節約と安全な授乳オプションが重要な都心部において、赤ちゃんの栄養に対する認識が進化していることと関連づけることができます。

核家族化や共働き世帯の増加に伴い、コンパクトで旅行にも便利な乳児用食品へのシフトも顕著です。利便性と携帯性は、栄養と使いやすさの両方を優先する、時間に制約のある介護者にとって不可欠な要素となっています。その結果、メーカーは忙しいライフスタイルにシームレスにフィットする、軽量でリシーラブル、1回分ずつの包装に注目しています。これらの形態は、準備時間を短縮し、無駄を最小限に抑え、衛生面でも優れているため、現代の子育てのニーズに理想的です。オーガニック、非遺伝子組み換え、クリーンラベル製品への動向は、購買者の嗜好を変化させ、世界市場で持続的な需要を支えています。親は子供の食べ物に何が入っているかについてますます慎重になりつつあり、透明性の高い原材料調達と最小限の加工を施した処方に対する需要の急増につながっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 72億米ドル |

| 予測金額 | 126億米ドル |

| CAGR | 5.9% |

製品カテゴリーのうち、乾燥ベビー用シリアル分野は、プロバイオティクス、ビタミン、必須ミネラルを含む、栄養強化、アレルゲンフリー、消化しやすいシリアルへの需要の急増に影響され、CAGR 6.1%で成長し、2034年までに46億米ドルに達すると予想されます。新製法は現在、幼児期の健康に対する懸念の高まりに対応するため、クリーンな原材料と強化された栄養プロファイルに焦点を当てています。この市場では、グルテンフリーやオーガニックなど、特定の食事ニーズに対応したイノベーションが進んでいます。

年齢ベースの嗜好に基づくと、2024年には6~12ヵ月のカテゴリーが37.4%で最大のシェアを占め、2034年までのCAGRは6.5%で成長すると予想されます。この乳幼児の開発段階では、より複雑な食感や栄養成分を導入する必要があり、便利な小分け済みミールの需要に拍車をかけています。リシーラブル容器や使い捨てパウチなどのパッケージング革新により、これらの製品は働く親にとってさらに実用的なものとなっています。共働き世帯の増加や調理済み製品の人気の高まりも、このセグメントの原動力となっています。市場は拡大しているもの、特にコストに敏感な地域では、価格面での懸念が成長をやや抑制する可能性があります。

欧州乾燥ベビーフード 2024年の市場シェアは30%で最大、栄養意識の高さと乳幼児の食品安全に対する規制当局の支援が原動力プレミアム・ベビーフードやオーガニック・ベビーフードの選択肢に対する需要の高まりが、引き続き同地域全体の製品開発を形成しています。市場の拡大は、強力な購買力と欧州の家庭におけるクリーン・ラベル製品の人気の高まりによっても支えられています。強力な規制の枠組みに加え、欧州は高い購買力にも恵まれているため、高品質のベビーフード製品に対する需要が高まっています。

Companies such as Abbott Laboratories, The Hain Celestial Group, Sprout Foods Inc., Meiji Holdings Co.Ltd.、Nestle S.A.、Hero Group、Holle Baby Food GmbH、Arla Foods amba、Ella's Kitchen Limited、Plum PBC、Danone S.A.、FrieslandCampina、Bellamy's Organic Pty Ltd、Riri Baby Food Co.Ltd.、Gerber Products Company、The Kraft Heinz Company、Beech-Nut Nut Nrition Corporation、Topfer GmbH、HiPP Internationalが市場でのプレゼンス向上に積極的に取り組んでいます。大手ブランドは、製品の多様化、持続可能な調達、クリーンラベルの革新に投資しています。その多くは、オーガニック製品ラインを拡大し、現地の流通業者と提携し、パッケージングを改良して棚への訴求力を高めています。さらに、各社は世界な働きかけを強化し、顧客の利便性を向上させるために、デジタル・エンゲージメントとeコマース・チャネルを増やしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国

- 主要輸入国

- サプライチェーンと流通分析

- 原材料調達

- 製造プロセス

- 脱水技術

- 凍結乾燥法

- 品質管理

- パッケージングイノベーション

- 持続可能なパッケージ

- スマートパッケージング

- 便利な機能

- 流通ネットワーク

- 伝統的な小売業

- eコマース

- 消費者直販

- サプライチェーンの課題

- 原材料の入手可能性

- エンドツーエンドの品質管理

- ロジスティクス

- サプライチェーンの最適化

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 世界の規制基準

- 地域ガイドライン

- FDA(米国)

- EFSA(EU)

- FSSAI(インド)

- CFDA(中国)

- その他の地域規制

- 品質と安全基準

- 重金属と汚染物質

- 栄養所要量

- ラベルと主張

- 包装の安全性

- オーガニック認証基準

- 規制上の課題と戦略

- 将来の規制動向

- 影響要因

- 促進要因

- 女性の労働力参加率の向上

- 乳児栄養への意識向上

- 都市化とライフスタイルの変化

- 利便性と長い保存期間

- 業界の潜在的リスク&課題

- 手作りベビーフードを好む

- 厳格な規制基準

- 新興市場における価格感応性

- サプライチェーンの混乱

- 市場機会

- オーガニックおよびクリーンラベル製品

- 強化された機能的な乾燥ベビーフード

- 新興市場への進出

- EコマースとD2Cモデル

- 市場の課題

- 重金属汚染の懸念

- 競争的な価格圧力

- 消費者の嗜好の変化

- 持続可能性に関する懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

- 消費者行動と嗜好

- 消費者の人口統計

- 購入決定要因

- 栄養価

- ブランド信頼

- 価格感度

- 利便性

- オーガニックと天然成分

- 消費者の購買パターン

- オンラインvs.オフライン

- サブスクリプションモデル

- サマリー買い

- 消費者の意識と教育

- 文化的および地域的な嗜好

- ソーシャルメディアとインフルエンサーの影響

- 技術革新と製品開発

- 処理技術

- 高度な脱水

- 栄養素の保存

- クリーンラベル方式

- 原料の革新

- スーパーフード

- 代替タンパク質

- 天然保存料

- パッケージングイノベーション

- 生分解性/堆肥化可能な素材

- アクティブでインテリジェントなパッケージング

- ポーションコントロール

- デジタル統合

- QRコードとトレーサビリティ

- モバイルアプリ

- Eコマースの最適化

- 研究開発と将来の動向

- 処理技術

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 乾燥ベビーシリアル

- 乾燥ベビーフード

- 乾燥したベビースナックとフィンガーフード

- ドライフルーツと野菜のピューレ

- フリーズドライベビーフード

第6章 市場推計・予測:ソース別、2021-2034

- 主要動向

- オーガニック

- 従来型

第7章 市場推計・予測:年齢別、2021-2034

- 主要動向

- 4~6ヶ月

- 6~12ヶ月

- 12~24ヶ月

- 24ヶ月以上

第8章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- スーパーマーケットとハイパーマーケット

- 専門店

- コンビニエンスストア

- オンライン小売

- 薬局とドラッグストア

- その他

第9章 市場推計・予測:包装形態別、2021-2034

- 主要動向

- ポーチ

- 瓶やボトル

- 缶

- 箱とカートン

- その他

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- Nestle S.A.

- Danone S.A.

- Abbott Laboratories

- Hero Group

- Mead Johnson Nutrition Company

- The Hain Celestial Group、Inc.

- HiPP International

- The Kraft Heinz Company

- Plum、PBC

- Ella's Kitchen Limited

- Gerber Products Company

- Sprout Foods、Inc.

- Beech-Nut Nutrition Corporation

- Bellamy's Organic Pty Ltd

- Arla Foods amba

- FrieslandCampina

- Meiji Holdings Co.、Ltd.

- Topfer GmbH

- Holle Baby Food GmbH

- Riri Baby Food Co.、Ltd.

目次

The Global Dried Baby Food Market was valued at USD 7.2 billion in 2024 and is estimated to grow at a CAGR of 5.9 % to reach USD 12.6 billion by 2034, driven by the increasing preference for easy-to-prepare and nutritionally balanced infant meals. Busy lifestyles, rising disposable incomes, and growing parental awareness about infant health are pushing demand across developed and developing regions. Parents choose dried baby food for its long shelf life, convenience, and nutritional value. The market's historic expansion can be linked to the evolving perception of baby nutrition, particularly in urban centers where time-saving and safe feeding options are critical.

With an increasing number of nuclear families and working parents, there's also a noticeable shift toward compact, travel-friendly food options for infants. Convenience and portability have become essential factors for time-constrained caregivers who prioritize both nutrition and ease of use. As a result, manufacturers are focusing on lightweight, resealable, and single-serve packaging that fits seamlessly into busy lifestyles. These formats reduce preparation time, minimize waste, and offer greater hygiene, making them ideal for modern parenting needs. The trend toward organic, non-GMO, and clean-label products is reshaping buyer preferences and supporting sustained demand across global markets. Parents are becoming increasingly cautious about what goes into their children's food, leading to a surge in demand for transparent ingredient sourcing and minimally processed formulations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.2 Billion |

| Forecast Value | $12.6 Billion |

| CAGR | 5.9% |

Among product categories, the dried baby cereals segment is expected to reach USD 4.6 billion by 2034, growing at a CAGR of 6.1% influenced by the surge in demand for fortified, allergen-free, and easily digestible cereals that contain probiotics, vitamins, and essential minerals. New formulations now focus on clean ingredients and enhanced nutritional profiles to address growing concerns about early childhood health. The market witness's innovation through gluten-free and organic options catering to specific dietary needs.

Based on age-based preferences, the 6 to 12-month category held the largest share in 2024 at 37.4% and is expected to grow at a 6.5% CAGR through 2034. This stage of infant development requires the introduction of more complex food textures and nutritional content, fueling demand for convenient, pre-portioned meals. Packaging innovation, such as resealable containers and single-use pouches, makes these products even more practical for working parents. The rise in dual-income households and the increasing popularity of ready-to-eat products are also driving forces in this segment. Although the market is expanding, pricing concerns may temper growth slightly, especially in more cost-sensitive regions.

Europe Dried Baby Food Market held the largest share of 30% in 2024, driven by high nutritional awareness and regulatory support for infant food safety. Increased demand for premium and organic baby food options continues to shape product development across the region. Market expansion is also supported by strong purchasing power and the rising popularity of clean-label offerings in European households. In addition to a strong regulatory framework, Europe benefits from high purchasing power, which fuels the demand for high-quality baby food products.

Companies such as Abbott Laboratories, The Hain Celestial Group, Sprout Foods Inc., Meiji Holdings Co. Ltd., Nestle S.A., Hero Group, Holle Baby Food GmbH, Arla Foods amba, Ella's Kitchen Limited, Plum PBC, Danone S.A., FrieslandCampina, Bellamy's Organic Pty Ltd, Riri Baby Food Co. Ltd., Gerber Products Company, The Kraft Heinz Company, Beech-Nut Nutrition Corporation, Topfer GmbH, and HiPP International are actively working to enhance market presence. Leading brands invest in product diversification, sustainable sourcing, and clean-label innovation. Many are expanding organic lines, partnering with local distributors, and enhancing packaging for greater shelf appeal. Additionally, companies are increasing digital engagement and e-commerce channels to strengthen global outreach and improve customer convenience.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Manufacturers

- 3.1.4 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic Industry Responses

- 3.2.4.1 Supply Chain Reconfiguration

- 3.2.4.2 Pricing and Product Strategies

- 3.2.4.3 Policy Engagement

- 3.2.5 Outlook and Future Considerations

- 3.2.6 Strategic industry responses

- 3.2.6.1 Supply chain reconfiguration

- 3.2.6.2 Pricing and product strategies

- 3.2.6.3 Policy engagement

- 3.2.7 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

- 3.4 Supply Chain and Distribution Analysis

- 3.4.1 Raw Material Sourcing

- 3.4.2 Manufacturing Processes

- 3.4.2.1 Dehydration Technologies

- 3.4.2.2 Freeze-Drying Methods

- 3.4.2.3 Quality Control

- 3.4.3 Packaging Innovations

- 3.4.3.1 Sustainable Packaging

- 3.4.3.2 Smart Packaging

- 3.4.3.3 Convenience Features

- 3.4.4 Distribution Network

- 3.4.4.1 Traditional Retail

- 3.4.4.2 E-commerce

- 3.4.4.3 Direct-to-Consumer

- 3.4.5 Supply Chain Challenges

- 3.4.5.1 Raw Material Availability

- 3.4.5.2 End-to-End Quality Control

- 3.4.5.3 Logistics

- 3.4.6 Supply Chain Optimization

- 3.5 Profit margin analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.7.1 Global Regulatory Standards

- 3.7.2 Regional Guidelines

- 3.7.2.1 FDA (U.S.)

- 3.7.2.2 EFSA (EU)

- 3.7.2.3 FSSAI (India)

- 3.7.2.4 CFDA (China)

- 3.7.2.5 Other Regional Regulations

- 3.7.3 Quality and Safety Standards

- 3.7.3.1 Heavy Metals and Contaminants

- 3.7.3.2 Nutritional Requirements

- 3.7.3.3 Labeling and Claims

- 3.7.3.4 Packaging Safety

- 3.7.4 Organic Certification Standards

- 3.7.5 Regulatory Challenges and Strategies

- 3.7.6 Future Regulatory Trends

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising Female Workforce Participation

- 3.8.1.2 Increasing Awareness of Infant Nutrition

- 3.8.1.3 Urbanization and Changing Lifestyles

- 3.8.1.4 Convenience and Longer Shelf Life

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Preference for Homemade Baby Food

- 3.8.2.2 Stringent Regulatory Standards

- 3.8.2.3 Price Sensitivity in Emerging Markets

- 3.8.2.4 Supply Chain Disruptions

- 3.8.3 Market opportunities

- 3.8.3.1 Organic and Clean Label Products

- 3.8.3.2 Fortified and Functional Dried Baby Food

- 3.8.3.3 Expansion in Emerging Markets

- 3.8.3.4. E-commerce and D2 C Models

- 3.8.4 Market Challenges

- 3.8.4.1 Heavy Metal Contamination Concerns

- 3.8.4.2 Competitive Pricing Pressure

- 3.8.4.3 Changing Consumer Preferences

- 3.8.4.4 Sustainability Concerns

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Consumer Behavior and Preferences

- 3.12.1 Consumer Demographics

- 3.12.2 Purchase Decision Factors

- 3.12.2.1 Nutritional Value

- 3.12.2.2 Brand Trust

- 3.12.2.3 Price Sensitivity

- 3.12.2.4 Convenience

- 3.12.2.5 Organic and Natural Ingredients

- 3.12.3 Consumer Buying Patterns

- 3.12.3.1 Online vs. Offline

- 3.12.3.2 Subscription Models

- 3.12.3.3 Bulk Purchases

- 3.12.4 Consumer Awareness and Education

- 3.12.5 Cultural and Regional Preferences

- 3.12.6 Impact of Social Media and Influencers

- 3.13 Technological Innovations and Product Development

- 3.13.1 Processing Technologies

- 3.13.1.1 Advanced Dehydration

- 3.13.1.2 Nutrient Preservation

- 3.13.1.3 Clean Label Methods

- 3.13.2 Ingredient Innovations

- 3.13.2.1 Superfoods

- 3.13.2.2 Alternative Proteins

- 3.13.2.3 Natural Preservatives

- 3.13.3 Packaging Innovations

- 3.13.3.1 Biodegradable/Compostable Materials

- 3.13.3.2 Active and Intelligent Packaging

- 3.13.3.3 Portion Control

- 3.13.4 Digital Integration

- 3.13.4.1 QR Codes and Traceability

- 3.13.4.2 Mobile Apps

- 3.13.4.3 E-commerce Optimization

- 3.13.5 R&D and Future Trends

- 3.13.1 Processing Technologies

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Dried baby cereals

- 5.3 Dried baby meals

- 5.4 Dried baby snacks and finger foods

- 5.5 Dried fruit and vegetable purees

- 5.6 Freeze-dried baby food

Chapter 6 Market Estimates & Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Organic

- 6.3 Conventional

Chapter 7 Market Estimates & Forecast, By Age Group, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 4–6 Months

- 7.3 6–12 Months

- 7.4 12–24 Months

- 7.5 Above 24 Months

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Supermarkets and hypermarkets

- 8.3 Specialty stores

- 8.4 Convenience stores

- 8.5 Online retail

- 8.6 Pharmacies and drugstores

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Pouches

- 9.3 Jars and bottles

- 9.4 Cans

- 9.5 Boxes and cartons

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Nestle S.A.

- 11.2 Danone S.A.

- 11.3 Abbott Laboratories

- 11.4 Hero Group

- 11.5 Mead Johnson Nutrition Company

- 11.6 The Hain Celestial Group, Inc.

- 11.7 HiPP International

- 11.8 The Kraft Heinz Company

- 11.9 Plum, PBC

- 11.10 Ella's Kitchen Limited

- 11.11 Gerber Products Company

- 11.12 Sprout Foods, Inc.

- 11.13 Beech-Nut Nutrition Corporation

- 11.14 Bellamy's Organic Pty Ltd

- 11.15 Arla Foods amba

- 11.16 FrieslandCampina

- 11.17 Meiji Holdings Co., Ltd.

- 11.18 Topfer GmbH

- 11.19 Holle Baby Food GmbH

- 11.20 Riri Baby Food Co., Ltd.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 300 Pages

- 納期

- 2~3営業日