|

市場調査レポート

商品コード

1740781

商用スタンバイガス発電機の市場機会、成長促進要因、産業動向分析、予測、2025~2034年Standby Commercial Gas Gensets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 商用スタンバイガス発電機の市場機会、成長促進要因、産業動向分析、予測、2025~2034年 |

|

出版日: 2025年04月15日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

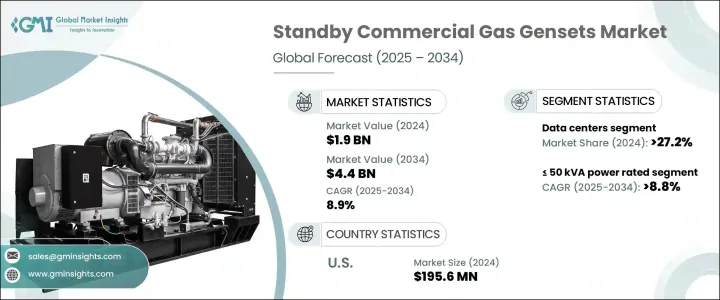

世界の商用スタンバイガス発電機市場は2024年に19億米ドルと評価され、CAGR 8.9%で成長し、2034年には44億米ドルに達すると推定されています。

ヘルスケア、小売業、製造業などの重要な商業分野でエネルギーの信頼性への注目が高まっていることが、スタンバイ発電機ソリューションの需要を促進しています。これらのシステムは、送電網の故障、停電、緊急事態の際に安定したバックアップ電力を供給する能力により、引き続き強い支持を得ています。世界中の企業がユーティリティインフラの老朽化、異常気象、デジタル依存の高まりによる電力途絶のリスクの高まりを認識する中、スタンバイ発電機の役割はさらに重要になっています。持続可能な事業へのシフト、エネルギー効率の高いシステムへの投資の急増、環境意識の高まりが、従来のディーゼルオプションよりもガスベースの発電機への移行を後押ししています。商用スタンバイガス発電機は、もはやオプションとは見なされていませんが、現代のレジリエンス計画には不可欠な要素です。運用コストの低さ、排出規制強化への適合性、スマートエネルギーシステムとの迅速な統合により、あらゆる産業で将来対応可能なインフラとして好まれています。市場はまた、IoTベースのモニタリング、ハイブリッドシステムの互換性、予知保全機能などの技術革新を目の当たりにしており、重要な用途におけるガス発電機の価値提案をさらに強化しています。

商業ビル、データセンター、小売スペースの増加により、電源バックアップのニーズが再構築され、中断のないオペレーションを優先する企業が増えています。頻繁な送電網の不安定化、時代遅れの電源フレームワーク、天候に起因する停電が、セクターを超えた幅広い採用を後押ししています。よりクリーンな燃焼技術を重視する規制や、低排出ガスシステムに対する政府のインセンティブにより、従来のディーゼルシステムと比較してガス発電機が魅力的なソリューションとなっています。企業は、運転効率だけでなく、メンテナンスの必要性の低さ、ライフサイクル価値の向上、次世代エネルギー基準への対応性からも、ガス発電機を支持しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 19億米ドル |

| 予測金額 | 44億米ドル |

| CAGR | 8.9% |

定格電力125kVA~200kVAセグメントは、2034年までに7億米ドルの売上が見込まれます。このカテゴリーは、通信インフラ、特に災害復旧準備に重点を置いたモバイルタワーや商業ハブ向けに需要があります。持続可能な運用と災害への備えに対する意識の高まりが、コスト、柔軟性、性能の最適なバランスを提供する中容量発電機への投資を後押ししています。

2024年のデータセンター向け商用スタンバイ発電機の市場シェアは27.2%でした。デジタル経済が拡大する中、特にエッジコンピューティングや超大規模クラウドモデルの採用により、発電機はデータの継続性を確保するために不可欠になっています。スマート診断、自動化対応コントローラー、高度な負荷管理システムの統合により、ダウンタイムほぼゼロを目指す事業者にとってスタンバイ発電機が不可欠となっています。

米国の商用スタンバイガス発電機市場は、2024年に1億9,560万米ドルを創出しました。排出規制の強化、持続可能性へのコミットメントの高まり、異常気象に対する脆弱性の増大が、ヘルスケア、金融、小売セクターのガス発電機需要を押し上げています。企業は、起動時間の短縮、メンテナンスの必要性の低減、ハイブリッドエネルギーシステムとのシームレスな統合を実現する低排出ソリューションに注目しています。

商用スタンバイガス発電機の世界市場における主なプレーヤーは、Wartsila、Caterpillar、Atlas Copco、ASHOK LEYLAND、JC Bamford Excavators、Cooper、Kirloskar、MAHINDRA POWEROL、Rolls Royce、Cummins、Siemens Energy、Aggreko、Generac Power System、GENSEAL ENERGY、Green Power International、三菱重工業、Rehlko、Sudhir Powerなどです。各社は、イノベーション、ハイブリッド燃料への対応、現地生産の拡大、戦略的OEM提携、IoT対応ソリューションに注力し、市場での存在感を高め、進化する顧客の需要に応えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:出力別、2021-2034年

- 主要動向

- 50kVA以下

- 50kVA~125kVA

- 125kVA~200kVA

- 200kVA~330kVA

- 330kVA~750kVA

- 750kVA超

第6章 市場規模・予測:最終用途別、2021-2034年

- 主要動向

- 通信

- ヘルスケア

- データセンター

- 教育機関

- 政府センター

- ホスピタリティ

- 小売

- 不動産

- 商業施設

- インフラ

- その他

第7章 市場規模・予測:地域別、2021-2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ロシア

- 英国

- ドイツ

- フランス

- スペイン

- オーストリア

- イタリア

- アジア太平洋地域

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- インドネシア

- マレーシア

- タイ

- ベトナム

- フィリピン

- 中東

- サウジアラビア

- アラブ首長国連邦

- カタール

- トルコ

- イラン

- オマーン

- アフリカ

- エジプト

- ナイジェリア

- アルジェリア

- 南アフリカ

- アンゴラ

- ケニア

- モザンビーク

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- チリ

第8章 企業プロファイル

- Aggreko

- ASHOK LEYLAND

- Atlas Copco

- Caterpillar

- Cooper

- Cummins

- Generac Power System

- Genesal Energy

- Green Power International

- JC Bamford Excavators

- Kirloskar

- MAHINDRA POWEROL

- Mitsubishi Heavy Industries

- Rehlko

- Rolls Royce

- Siemens Energy

- Sudhir Power

- Wartsila

The Global Standby Commercial Gas Gensets Market was valued at USD 1.9 billion in 2024 and is estimated to grow at a CAGR of 8.9% to reach USD 4.4 billion by 2034. Increasing focus on energy reliability across critical commercial sectors like healthcare, retail, and manufacturing is driving the demand for standby genset solutions. These systems continue to gain strong traction for their ability to deliver consistent backup power during grid failures, blackouts, or emergencies. As businesses worldwide recognize the rising risks of power disruptions due to aging utility infrastructure, extreme weather events, and growing digital dependency, the role of standby gensets becomes even more critical. Shifts toward sustainable operations, surging investments in energy-efficient systems, and rising environmental consciousness are fueling the transition toward gas-based gensets over conventional diesel options. Standby commercial gas gensets are no longer seen as optional but essential components in modern resilience planning. Their lower operational costs, better compliance with tightening emission norms, and quicker integration with smart energy systems have made them a preferred choice for future-ready infrastructure across industries. The market is also witnessing technological innovations like IoT-based monitoring, hybrid system compatibility, and predictive maintenance capabilities, further strengthening the value proposition of gas gensets in critical applications.

The growth of commercial buildings, data centers, and retail spaces is reshaping power backup needs, with businesses increasingly prioritizing uninterrupted operations. Frequent grid instability, outdated power frameworks, and weather-related outages are pushing broader adoption across sectors. Regulatory emphasis on cleaner combustion technologies and government incentives for lower-emission systems are making gas gensets an attractive solution compared to traditional diesel systems. Businesses are favoring gas gensets not only for operational efficiency but also for their lower maintenance needs, improved lifecycle value, and readiness to meet next-generation energy standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $4.4 Billion |

| CAGR | 8.9% |

The >125 kVA to 200 kVA power rating segment is expected to generate USD 700 million by 2034. This category remains in demand across telecom infrastructure, particularly for mobile towers and commercial hubs focused on disaster recovery preparedness. Rising awareness around sustainable operations and disaster readiness is boosting investments in medium-capacity gensets, which offer an optimal balance between cost, flexibility, and performance.

Standby commercial gensets serving data centers accounted for a 27.2% market share in 2024. As the digital economy expands, especially with the adoption of edge computing and hyper-scale cloud models, gensets are becoming vital for ensuring data continuity. Integration of smart diagnostics, automation-ready controllers, and advanced load management systems is making standby gensets indispensable for operators aiming for near-zero downtime.

The U.S. Standby Commercial Gas Gensets Market generated USD 195.6 million in 2024. Stricter emissions regulations, growing sustainability commitments, and increased vulnerability to extreme weather are pushing demand for gas gensets across healthcare, finance, and retail sectors. Businesses are turning to low-emission solutions that deliver faster start times, reduced maintenance needs, and seamless integration with hybrid energy systems.

Key market players in the Global Standby Commercial Gas Gensets Market include Wartsila, Caterpillar, Atlas Copco, ASHOK LEYLAND, JC Bamford Excavators, Cooper, Kirloskar, MAHINDRA POWEROL, Rolls Royce, Cummins, Siemens Energy, Aggreko, Generac Power System, GENSEAL ENERGY, Green Power International, Mitsubishi Heavy Industries, Rehlko, and Sudhir Power. Companies are focusing on innovation, hybrid fuel readiness, local manufacturing expansion, strategic OEM alliances, and IoT-enabled solutions to strengthen market presence and meet evolving customer demands.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw material)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw material)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Power Rating, 2021 - 2034 ('000 Units & USD Million)

- 5.1 Key trends

- 5.2 ≤ 50 kVA

- 5.3 > 50 kVA - 125 kVA

- 5.4 > 125 kVA - 200 kVA

- 5.5 > 200 kVA - 330 kVA

- 5.6 > 330 kVA - 750 kVA

- 5.7 > 750 kVA

Chapter 6 Market Size and Forecast, By End Use, 2021 - 2034 ('000 Units & USD Million)

- 6.1 Key trends

- 6.2 Telecom

- 6.3 Healthcare

- 6.4 Data centers

- 6.5 Educational institutions

- 6.6 Government centers

- 6.7 Hospitality

- 6.8 Retail sales

- 6.9 Real estate

- 6.10 Commercial complex

- 6.11 Infrastructure

- 6.12 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 ('000 Units & USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Russia

- 7.3.2 UK

- 7.3.3 Germany

- 7.3.4 France

- 7.3.5 Spain

- 7.3.6 Austria

- 7.3.7 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.4.6 Indonesia

- 7.4.7 Malaysia

- 7.4.8 Thailand

- 7.4.9 Vietnam

- 7.4.10 Philippines

- 7.5 Middle East

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Turkey

- 7.5.5 Iran

- 7.5.6 Oman

- 7.6 Africa

- 7.6.1 Egypt

- 7.6.2 Nigeria

- 7.6.3 Algeria

- 7.6.4 South Africa

- 7.6.5 Angola

- 7.6.6 Kenya

- 7.6.7 Mozambique

- 7.7 Latin America

- 7.7.1 Brazil

- 7.7.2 Mexico

- 7.7.3 Argentina

- 7.7.4 Chile

Chapter 8 Company Profiles

- 8.1 Aggreko

- 8.2 ASHOK LEYLAND

- 8.3 Atlas Copco

- 8.4 Caterpillar

- 8.5 Cooper

- 8.6 Cummins

- 8.7 Generac Power System

- 8.8 Genesal Energy

- 8.9 Green Power International

- 8.10 JC Bamford Excavators

- 8.11 Kirloskar

- 8.12 MAHINDRA POWEROL

- 8.13 Mitsubishi Heavy Industries

- 8.14 Rehlko

- 8.15 Rolls Royce

- 8.16 Siemens Energy

- 8.17 Sudhir Power

- 8.18 Wartsilä