|

市場調査レポート

商品コード

1740778

ソーラーPV製造装置の市場機会、成長促進要因、産業動向分析、予測、2025~2034年Solar PV Manufacturing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ソーラーPV製造装置の市場機会、成長促進要因、産業動向分析、予測、2025~2034年 |

|

出版日: 2025年04月29日

発行: Global Market Insights Inc.

ページ情報: 英文 122 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

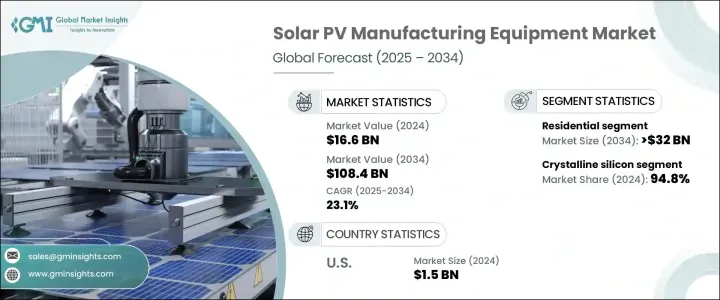

ソーラーPV製造装置の世界市場規模は、2024年に166億米ドルとなり、CAGR 23.1%で成長し、2034年には1,084億米ドルに達すると推定されています。

この市場拡大の背景には、エネルギー自給への関心の高まりと、信頼性が高く弾力性のある太陽電池部品の国内生産へのニーズの高まりがあります。地政学的不確実性の高まりは、特にウエハー、セル、モジュールなどの重要な上流部品について、各国における製造事業の現地化の必要性を高めています。こうした国内生産へのシフトは産業活動を活発化させ、ソーラーPVのインフラや設備への大規模な投資を促しています。

先端セル技術の採用が進み、ソーラーPV製造装置市場の情勢はさらに変化しています。メーカーは、高効率セルやモジュール設計の技術革新に対応できる最新鋭の生産ラインに多額の投資を行っています。こうした機能強化は、エネルギー収率を向上させるだけでなく、生産コストの最適化にも役立ちます。装置開発企業は、自動化、AIツール、機械学習をシステムに統合する傾向を強めており、これにより製造精度と拡張性が大幅に向上しています。この動向は、新規参入企業の参入障壁を下げ、既存企業には事業拡大の機会を提供しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 166億米ドル |

| 予測金額 | 1,084億米ドル |

| CAGR | 23.1% |

各国が脱炭素化目標の達成と電力消費量増加への取り組みを強化する中、太陽光発電設備に対する需要は複数の分野で高まっています。住宅、商業施設、ユーティリティの各アプリケーションで高まる太陽光発電導入のニーズを満たすため、産業規模の機械加工がこれまで以上に不可欠になっています。ポリシリコン、インゴット、ウエハー、太陽電池、完成モジュールの生産を含む川上分野は、引き続き大きな需要があり、装置市場の拡大に拍車をかけています。

貿易政策も市場力学を大きく形成しています。外国製ソーラーPV製品に対する貿易規制は、世界のメーカーにサプライチェーンの多様化を促し、生産能力を別の製造しやすい地域に移転するよう促しています。このシフトは新興産業ハブの開発を支援し、従来の供給源への依存を減らす一方で、短期的な装置価格の上昇を引き起こし、移行期間中のプロジェクトスケジュールに影響を及ぼすと予想されます。

アプリケーション別では、市場は住宅用、商業用、ユーティリティの各セグメントに分類されます。住宅用セグメントは、エネルギーコストの上昇、持続可能性に対する住宅所有者の意識の高まり、有利な規制優遇措置によって後押しされ、2034年までに320億米ドルを超えると予想されています。住宅システムにおけるスマート機能や蓄電池の統合といった技術の進歩が、住宅用太陽光発電の設置をより魅力的なものにしています。また、消費者はより大きなエネルギーの自律性を求めており、系統停電時のバックアップソリューションへの関心の高まりも、この分野の勢いに寄与しています。

技術面では、ソーラーPV製造装置市場セグメンテーションは薄膜シリコンと結晶シリコンに区分されます。結晶シリコン技術は、2024年時点で94.8%のシェアを占め、現在市場を独占しています。その優位性は、より高いエネルギー変換率、豊富な材料の入手可能性、継続的な技術強化に起因します。様々なアプリケーションの中でも、単結晶シリコンは限られたスペースでより大きな出力を提供できるため、依然として好ましい選択肢であり、住宅の屋上や高密度の商業施設や公共施設の両方に理想的です。

地域別では、北米市場の成長が顕著であり、2024年の世界市場シェアの9.6%以上を占めています。米国だけでも2022年に10億米ドルの市場価値を記録し、2023年には12億米ドル、2024年には15億米ドルに増加します。この成長を促進する上で、支援的な政策措置が重要な役割を果たしています。税額控除や生産奨励金など、国内生産を強化することを目的とした包括的な法制度は、資本コストを削減し、太陽電池サプライチェーン全体に新たな投資を誘致しています。

グローバルサプライチェーンの脆弱性が表面化し続けるなか、国内製造エコシステムが優先され、垂直統合型事業への投資が急増しています。コスト、品質、リードタイムをより確実に管理するため、原材料から最終製品の組み立てまで、生産プロセス全体を内製化する企業が増えています。また、地域企業との戦略的パートナーシップも頻繁に行われるようになり、地域の専門知識へのアクセスを提供し、市場への迅速な浸透を促しています。こうした協力関係は、技術移転を促進し、次世代ソーラー技術の商業化を加速させています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア

- 戦略的ダッシュボード

- 企業ベンチマーク

- イノベーションとテクノロジーの情勢

第5章 市場規模・予測:製造装置別、2021-2034年

- 主要動向

- シリコン装置

- インゴット装置

- ウエハー装置

- セル装置

- モジュール装置

第6章 市場規模・予測:技術別、2021-2034年

- 主要動向

- 結晶シリコン

- 薄膜

第7章 市場規模・予測:アプリケーション別、2021-2034年

- 主要動向

- 住宅

- 商業

- ユーティリティ

第8章 市場規模・予測:地域別、2021-2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

- メキシコ

第9章 企業プロファイル

- Adani Solar

- Emmvee

- First Solar

- Goldi Solar

- Grew Solar

- JA Solar

- LDK Solar

- Premier Energies

- RenewSys

- Servotech Renewable Power System

- Tata Power Solar

- Tongwei Solar

- Trina Solar

- Vikram Solar

- Waaree Energies

The Global Solar PV Manufacturing Equipment Market was valued at USD 16.6 billion in 2024 and is estimated to grow at a CAGR of 23.1% to reach USD 108.4 billion by 2034. This expansion is driven by the increasing focus on energy independence and the growing need for reliable and resilient domestic production of solar components. Rising geopolitical uncertainties have intensified the urgency for countries to localize manufacturing operations, especially for critical upstream components such as wafers, cells, and modules. This shift toward domestic production is enhancing industrial activity and encouraging major investments in solar PV infrastructure and equipment.

Growing adoption of advanced cell technologies is further reshaping the landscape of the solar PV manufacturing equipment market. Manufacturers are heavily investing in state-of-the-art production lines capable of handling innovations in high-efficiency cell types and module designs. These enhancements not only improve energy yields but also help optimize production costs. Equipment developers are increasingly integrating automation, AI tools, and machine learning into their systems, which is significantly improving manufacturing precision and scalability. This trend is lowering entry barriers for new players and providing opportunities for existing companies to expand operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.6 Billion |

| Forecast Value | $108.4 Billion |

| CAGR | 23.1% |

As countries ramp up efforts to meet decarbonization goals and tackle rising electricity consumption, demand for solar equipment is intensifying across multiple sectors. Industrial-scale machinery fabrication is becoming more vital than ever to meet the rising need for solar deployment across residential, commercial, and utility applications. The upstream segment, which includes the production of polysilicon, ingots, wafers, solar cells, and finished modules, continues to experience substantial demand, fueling the expansion of the equipment market.

Trade policies are also shaping the market dynamics significantly. Trade restrictions on foreign solar PV products are prompting global manufacturers to diversify their supply chains and relocate production capacities to alternative manufacturing-friendly regions. While this shift supports the development of emerging industrial hubs and reduces dependency on traditional supply sources, it is expected to cause a short-term increase in equipment prices and affect project timelines during the transition.

By application, the market is categorized into residential, commercial, and utility segments. The residential segment is expected to surpass USD 32 billion by 2034, bolstered by rising energy costs, increased homeowner awareness of sustainability, and favorable regulatory incentives. Technological advancements, such as the integration of smart features and battery storage in home systems, are making residential solar installations more appealing. Consumers are also seeking greater energy autonomy, and their growing interest in backup solutions during grid outages is contributing to the sector's momentum.

In terms of technology, the solar PV manufacturing equipment market is segmented into thin film and crystalline silicon categories. Crystalline silicon technology currently dominates the market with a 94.8% share as of 2024. Its dominance is attributed to its higher energy conversion rates, abundant material availability, and ongoing technological enhancements. Among the various applications, monocrystalline silicon remains the preferred choice due to its ability to deliver greater output in limited space, making it ideal for both residential rooftops and high-density commercial or utility installations.

Regionally, the market is witnessing notable growth in North America, which accounted for over 9.6% of the global market share in 2024-a figure expected to increase by 2034. The United States alone recorded a market value of USD 1 billion in 2022, rising to USD 1.2 billion in 2023 and USD 1.5 billion in 2024. Supportive policy measures are playing a crucial role in driving this growth. Comprehensive legislative packages aimed at bolstering domestic manufacturing, including tax credits and production incentives, are reducing capital costs and attracting new investments across the solar supply chain.

As global supply chain vulnerabilities continue to surface, domestic manufacturing ecosystems are being prioritized, leading to a surge in investment in vertically integrated operations. Companies are increasingly bringing in-house the entire production process-from raw materials to final product assembly-to ensure better control over costs, quality, and lead times. Strategic partnerships with regional firms are also becoming more frequent, providing access to local expertise and facilitating faster market penetration. These collaborations are fostering technology transfer and speeding up the commercialization of next-generation solar technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic dashboard

- 4.4 Company benchmarking

- 4.5 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Manufacturing Equipment, 2021 – 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Silicon equipment

- 5.3 Ingots equipment

- 5.4 Wafer equipment

- 5.5 Cells equipment

- 5.6 Module equipment

Chapter 6 Market Size and Forecast, By Technology, 2021 – 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Crystalline silicon

- 6.3 Thin film

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.4 Utility

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

- 8.6.4 Mexico

Chapter 9 Company Profiles

- 9.1 Adani Solar

- 9.2 Emmvee

- 9.3 First Solar

- 9.4 Goldi Solar

- 9.5 Grew Solar

- 9.6 JA Solar

- 9.7 LDK Solar

- 9.8 Premier Energies

- 9.9 RenewSys

- 9.10 Servotech Renewable Power System

- 9.11 Tata Power Solar

- 9.12 Tongwei Solar

- 9.13 Trina Solar

- 9.14 Vikram Solar

- 9.15 Waaree Energies