|

市場調査レポート

商品コード

1740777

自動車用コントロールケーブルの市場機会、成長促進要因、産業動向分析、予測、2025~2034年Automotive Control Cables Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用コントロールケーブルの市場機会、成長促進要因、産業動向分析、予測、2025~2034年 |

|

出版日: 2025年04月16日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

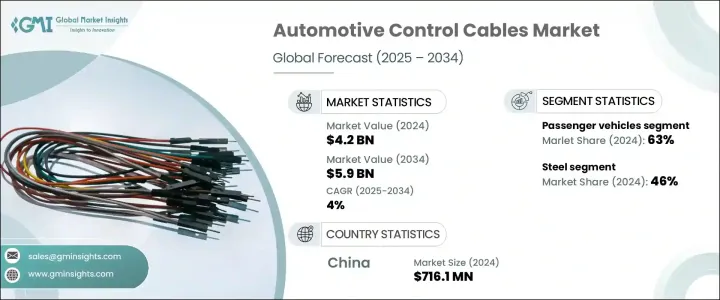

自動車用コントロールケーブルの世界市場規模は、2024年には42億米ドルとなり、特にアジア太平洋とラテンアメリカの新興経済圏における自動車生産の増加に牽引され、CAGR 4%で成長し、2034年には59億米ドルに達すると予測されています。

自動車用コントロールケーブルは、クラッチ係合、ブレーキ、ギアシフト、スロットル制御の精度を確保し、自動車性能の重要な部分を形成しています。自動車セクターの進化に伴い、車両の効率性、耐久性、ユーザーエクスペリエンスが重視され、ケーブル技術の革新が続いています。世界の自動車生産は、特に経済状況の改善と都市化が自動車販売の原動力となっている発展途上地域で急速に拡大しています。その一方で、OEMは先進的なケーブルシステムを通じて機械的信頼性と応答性を高めることに注力しています。自動車の安全性と性能に対する消費者の期待の高まりが、高品質のコントロールケーブルの需要をさらに押し上げています。さらに、世界的に排ガス規制が強化されたことで、自動車メーカーはコントロールケーブルのような機械部品を含む車両システムを最適化し、エネルギー効率を高める必要に迫られています。

電気自動車とハイブリッド車への業界の軸足は、コントロールケーブルの用途を再構築しています。電気自動車(EV)は、内燃エンジンで使用されていた従来の機械部品の一部を廃止する一方で、コントロールケーブルに新たな重要な用途をもたらします。EVの設計がより複雑になるにつれ、制御ケーブルは、HVACシステムのフラップ制御や空気分配、バッテリーコンパートメントアクセス機構、座席の移動、充電インターフェイス制御など、さまざまな機能をサポートするために適応しています。このように使用事例が進化することで、メーカーがイノベーションを起こし、新世代の自動車の需要に応える新たな機会が生まれています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 42億米ドル |

| 予測金額 | 59億米ドル |

| CAGR | 4% |

素材の種類では、スチールが引き続き自動車用コントロールケーブル市場を独占し、2024年には46%のシェアを占める。その卓越した耐久性、引張強度、コスト効率、製造の容易さにより、クラッチ、ブレーキ、スロットル用途に好んで使用されています。業界各社が燃費を向上させるためにアルミニウムや複合材料のような軽量素材を模索しているとしても、スチールは、特に高性能モデルや量販モデルにおいて、厳しい条件下での弾力性のために不可欠な存在であり続けています。OEMとアフターマーケットサプライヤーは、その手頃な価格と広く入手可能なことからスチールを好んで使用し、安定した需要を確保しています。

車種別では乗用車が市場をリードし、2024年には63%のシェアを確保し、安定した成長傾向を維持します。このリーダーシップは、生産台数の多さと、世界の小型車、中型車、高級車に対する消費者の旺盛な購買意欲を反映しています。急速な都市化、中間所得層の拡大、インドや東南アジア諸国における自動車へのアクセスの向上が、この成長の主な要因となっています。コントロールケーブルは、手動と自動の両方の機能をサポートし、全体的な運転体験と安全性を高めるために、これらの自動車に不可欠です。

中国自動車用コントロールケーブル2024年の市場規模は7億1,610万米ドルで、2034年までのシェアは39%を占める。同国の強力な製造基盤、高騰する内需、積極的なEV推進が同国のリーダーシップを強化しています。有利な政府政策と拡大する輸出ネットワークは、自動車用ケーブルシステムの技術革新をさらに推進し、自動車用コントロールケーブル生産の世界的ハブとしての中国の役割を確固たるものにしています。

世界自動車用コントロールケーブル市場で事業を展開する主要企業 - Hi-Lex, Yazaki, Aptiv, Trelleborg, Cablecraft Motion Controls, Kongsberg Automotive, Lear, DURA Automotive Systems, TE Connectivity, Furukawa Electric - は、世界サプライチェーンの拡大、OEMとのパートナーシップの強化、軽量材料技術への投資、製造プロセスの自動化に注力しています。各社はまた、EVや自律走行車システムに合わせた高度なケーブルソリューションを開発するための研究開発努力も強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料サプライヤー

- 部品メーカー

- 制御ケーブル組立業者/製造業者

- ティア1自動車部品サプライヤー

- OEM(オリジナル機器メーカー)およびアフターマーケット販売業者

- 利益率分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 他国による報復措置

- 業界への影響

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 乗用車と商用車の世界生産の増加

- EVとハイブリッド車への移行

- 制御ケーブルの定期的なメンテナンスと交換の必要性

- ケーブル設計と材料の継続的な革新

- 業界の潜在的リスク&課題

- ドライブバイワイヤ技術への移行の増加

- 厳格かつ進化する環境規制

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推定・予測:ケーブル別、2021-2034年

- 主要動向

- クラッチケーブル

- アクセルケーブル

- ブレーキケーブル

- ギアシフトケーブル

- ハンドブレーキケーブル

- スロットルケーブル

- その他

第6章 市場推定・予測:材料別、2021-2034年

- 主要動向

- 鋼鉄

- PVC(ポリ塩化ビニル)

- ナイロン

- ゴムコーティング

- その他

第7章 市場推定・予測:車両別、2021-2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 二輪車

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第8章 市場推定・予測:アプリケーション別、2021-2034年

- 主要動向

- エンジン制御

- トランスミッション制御

- ブレーキシステム

- HVACシステム

- その他

第9章 市場推定・予測:販売チャネル別、2021-2034年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推定・予測:地域別、2021-2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Aptiv

- Bergen Cable Technology

- Cablecraft Motion Controls

- Conwire

- DURA Automotive Systems

- Furukawa Electric

- Hi-Lex

- Kongsberg Automotive

- Kuster Holding

- Lear

- Lexco Cable

- Orscheln Products

- Sila Group

- Sumitomo Electric Industries

- Suprajit Engineering

- TE Connectivity

- Trelleborg

- Triumph Group

- Venus Industrial

- Yazaki

The Global Automotive Control Cables Market was valued at USD 4.2 billion in 2024 and is estimated to grow at a CAGR of 4% to reach USD 5.9 billion by 2034, driven by rising vehicle production, particularly across emerging economies in Asia-Pacific and Latin America. Automotive control cables form a vital part of vehicular performance, ensuring precision in clutch engagement, braking, gear shifting, and throttle control. As the automotive sector evolves, a strong emphasis on vehicle efficiency, durability, and user experience continues to fuel innovation in cable technologies. Global automotive production is scaling up rapidly, especially in developing regions where improving economic conditions and urbanization drive automobile sales. Meanwhile, OEMs are focusing on enhancing mechanical reliability and responsiveness through advanced cable systems. Increasing consumer expectations around vehicle safety and performance further boosts demand for high-quality control cables. Additionally, stricter emissions regulations globally are pushing automakers to optimize vehicle systems, including mechanical components like control cables, to achieve better energy efficiency.

The industry's pivot to electric and hybrid vehicles is reshaping control cable applications. While electric vehicles (EVs) eliminate some traditional mechanical parts used in internal combustion engines, they introduce new and critical applications for control cables. As EV designs grow more complex, control cables are adapted to support various functions, such as flap control and air distribution in HVAC systems, battery compartment access mechanisms, seat movement, and charging interface controls. These evolving use cases are unlocking fresh opportunities for manufacturers to innovate and meet the demands of a new generation of vehicles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.2 Billion |

| Forecast Value | $5.9 Billion |

| CAGR | 4% |

Among material types, steel continues to dominate the automotive control cables market, accounting for a 46% share in 2024. Its exceptional durability, tensile strength, cost-efficiency, and manufacturing ease make it the preferred choice for clutch, brake, and throttle applications. Even as industry players explore lighter materials like aluminum or composites to boost fuel economy, steel remains indispensable for its resilience under demanding conditions, especially in high-performance and mass-market models. OEMs and aftermarket suppliers favor steel for its affordability and widespread availability, ensuring a steady demand.

Passenger vehicles lead the market by vehicle type, securing a 63% share in 2024 and maintaining a steady growth trend. This leadership reflects high production volumes and a surging consumer appetite for compact, mid-size, and luxury vehicles worldwide. Rapid urbanization, expanding middle-class income, and better automotive access in countries like India and throughout Southeast Asia are major factors fueling this growth. Control cables are essential across these vehicles for supporting both manual and automated functions, enhancing the overall driving experience and safety.

China Automotive Control Cables Market generated USD 716.1 million in 2024 and captured a commanding 39% share through 2034. The country's strong manufacturing base, soaring domestic demand, and aggressive EV push are strengthening its leadership. Favorable government policies and an expanding export network are further propelling innovation in automotive cable systems, solidifying China's role as a global hub for automotive control cable production.

Key companies operating in the Global Automotive Control Cables Market-Hi-Lex, Yazaki, Aptiv, Trelleborg, Cablecraft Motion Controls, Kongsberg Automotive, Lear, DURA Automotive Systems, TE Connectivity, and Furukawa Electric-are sharpening their focus on expanding global supply chains, forging deeper partnerships with OEMs, investing in lightweight material technologies, and automating manufacturing processes. Companies are also ramping up R&D efforts to engineer advanced cable solutions tailored for EVs and autonomous vehicle systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component manufacturers

- 3.2.3 Control cable assemblers/manufacturers

- 3.2.4 Tier 1 automotive suppliers

- 3.2.5 Original equipment manufacturers (OEMs) & aftermarket distributors

- 3.3 Profit margin analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures by other countries

- 3.4.2 Impact on the industry

- 3.4.2.1 Price Volatility in key materials

- 3.4.2.2 Supply chain restructuring

- 3.4.2.3 Production cost implications

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing global production of passenger and commercial vehicles

- 3.9.1.2 The shift toward EVs and hybrid vehicles

- 3.9.1.3 The need for regular maintenance and replacement of control cables

- 3.9.1.4 Continuous innovation in cable design and materials

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Increasing shift towards drive-by-wire technology

- 3.9.2.2 Stringent and evolving environmental regulations

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Cable, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Clutch cables

- 5.3 Accelerator cables

- 5.4 Brake cables

- 5.5 Gear shift cables

- 5.6 Handbrake cables

- 5.7 Throttle cables

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Steel

- 6.3 PVC (Polyvinyl Chloride)

- 6.4 Nylon

- 6.5 Rubber coated

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Two-wheelers

- 7.4 Commercial vehicles

- 7.4.1 Light Commercial Vehicles (LCV)

- 7.4.2 Medium Commercial Vehicles (MCV)

- 7.4.3 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Engine control

- 8.3 Transmission control

- 8.4 Braking system

- 8.5 HVAC system

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Aptiv

- 11.2 Bergen Cable Technology

- 11.3 Cablecraft Motion Controls

- 11.4 Conwire

- 11.5 DURA Automotive Systems

- 11.6 Furukawa Electric

- 11.7 Hi-Lex

- 11.8 Kongsberg Automotive

- 11.9 Kuster Holding

- 11.10 Lear

- 11.11 Lexco Cable

- 11.12 Orscheln Products

- 11.13 Sila Group

- 11.14 Sumitomo Electric Industries

- 11.15 Suprajit Engineering

- 11.16 TE Connectivity

- 11.17 Trelleborg

- 11.18 Triumph Group

- 11.19 Venus Industrial

- 11.20 Yazaki