モジュール式変電所の市場機会、成長促進要因、産業動向分析、予測、2025~2034年

Modular Substation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 121 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740776

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

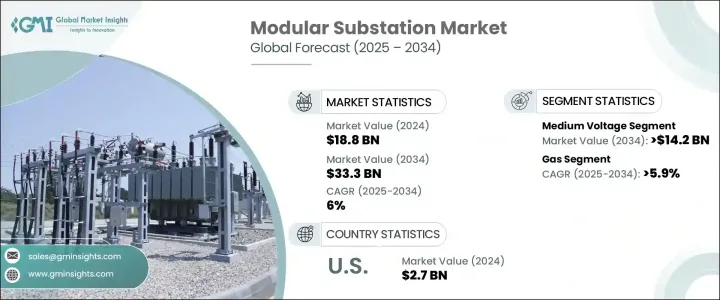

世界のモジュール式変電所市場は、2024年に188億米ドルと評価され、急速な都市化、産業の拡大、再生可能エネルギー源の国家送電網への統合の増加により、CAGR 6%で成長し、2034年には333億米ドルに達すると推定されています。

世界の電力需要が急増し続ける中、モジュール式変電所は電力インフラの近代化に不可欠なソリューションとして勢いを増しています。そのプレハブ式で拡張性の高い設計は、迅速な配備を可能にし、特にスペースに制約のある都市環境や、従来の変電所が実用的でない遠隔地では極めて重要です。

世界中の政府と電力会社は、送電網の回復力とスマートグリッドのアップグレードを優先しており、モジュール式変電所のような柔軟でコスト効率の高いソリューションの必要性をさらに高めています。こうした変電所は、再生可能エネルギープロジェクトの支援に加え、脱炭素化目標にも合致しており、国家送電網の全体的な効率と持続可能性を高めています。エネルギー安全保障の重視の高まりは、電化イニシアティブへの大規模投資と相まって、今後10年間でモジュール式技術へのシフトを加速させる舞台となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 188億米ドル |

| 予測金額 | 333億米ドル |

| CAGR | 6% |

モジュール式変電所は、その明確な利点にもかかわらず、高額な初期投資コストや規制上のハードルといった課題に直面しています。変圧器や開閉装置のような輸入部品に対する関税は、特に海外サプライヤーへの依存度が高い地域では、製造コストを高騰させています。このような経済的圧力は、小規模な電力会社や新興経済諸国で事業を展開する電力会社にとって、モジュール技術の採用を躊躇させる要因となっています。複雑な許認可プロセスや、大型モジュール式ユニットの輸送と設置に関連するロジスティクスの複雑さも、プロジェクトの遅れを生じさせる。こうした障壁を克服するには、現地製造への的を絞った投資、戦略的なサプライチェーンマネジメント、モジュール式変電所の迅速な展開を促す規制枠組みの合理化が必要です。

11kVから33kVまでの中電圧セグメントは、2034年までモジュール式変電所市場をリードし、その市場規模は142億米ドルに達すると予測されています。中電圧システムは、人口密度の高い都市や成長する農村地帯に効率的に配電する上で重要な役割を果たしています。運転容量と展開速度のバランスがとれているため、送電網の強化、ネットワークの拡大、急速な電化プロジェクトに重点を置く電力会社にとって好ましい選択肢となっています。

ガス絶縁モジュール式変電所の需要も増加傾向にあり、このセグメントは2034年までCAGR 5.9%で成長すると予想されています。コンパクトな設計、高い安全基準、密集した環境での強力な性能で知られるガス絶縁ユニットは、大都市圏や工業地帯で不可欠なものとなっています。その密閉された筐体は、重要な部品を過酷な環境要因から保護し、メンテナンスの必要性を大幅に削減し、運転寿命を延ばします。

米国モジュール式変電所市場は2024年に27億米ドルに達し、老朽化した送電網システムの近代化を推し進める米国がその原動力となっています。電化の進展、再生可能エネルギー発電の導入、分散型発電の重視に伴い、モジュール式変電所は送電網の耐障害性を高め、異常気象時の信頼できる電力供給を確保するために不可欠となっています。世界市場をリードする主なプレーヤーは、ABB, Eaton Corporation, Siemens, General Electric, Schneider Electricなどで、いずれも技術革新、戦略的パートナーシップ、スマートグリッド機能の拡大に注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略的ダッシュボード

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:電圧別、2021-2034年

- 主要動向

- 低

- 中

- 高

第6章 市場規模・予測:絶縁別、2021-2034年

- 主要動向

- 空気

- ガス

第7章 市場規模・予測:アプリケーション別、2021-2034年

- 主要動向

- 商業

- 工業

- ユーティリティ

第8章 市場規模・予測:地域別、2021-2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- アジア太平洋地域

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第9章 企業プロファイル

- ABB

- CHINT Global

- Doho Electric

- Eaton

- Federal Pacific

- General Electric

- Hitachi

- LS Electric

- Orecco Electric

- Schneider Electric

- Siemens

- TGOOD International

目次

The Global Modular Substation Market was valued at USD 18.8 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 33.3 billion by 2034, driven by rapid urbanization, industrial expansion, and the increasing integration of renewable energy sources into national grids. As global electricity demand continues to surge, modular substations are gaining momentum as a vital solution for modernizing power infrastructure. Their prefabricated, scalable designs enable quick deployment, especially critical in space-constrained urban settings and remote regions where traditional substations are impractical.

Governments and utilities worldwide are prioritizing grid resilience and smart grid upgrades, further boosting the need for flexible, cost-effective solutions like modular substations. In addition to supporting renewable energy projects, these substations align with decarbonization goals, enhancing the overall efficiency and sustainability of national grids. The growing emphasis on energy security, coupled with major investments in electrification initiatives, is setting the stage for an accelerated shift toward modular technologies over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.8 Billion |

| Forecast Value | $33.3 Billion |

| CAGR | 6% |

Despite their clear advantages, modular substations face challenges such as high upfront investment costs and regulatory hurdles. Tariffs on imported components like transformers and switchgear have escalated production expenses, particularly in regions heavily reliant on international suppliers. These economic pressures can discourage smaller utilities and those operating in developing economies from adopting modular technologies. Complicated permitting processes and logistical complexities associated with transporting and installing large modular units can also create project delays. Overcoming these barriers calls for targeted investments in local manufacturing, strategic supply chain management, and streamlined regulatory frameworks that encourage faster deployment of modular substations.

The medium voltage segment, spanning from 11kV to 33kV, is projected to lead the modular substation market through 2034, with its value expected to hit USD 14.2 billion. Medium voltage systems play a critical role in efficiently distributing power across densely populated cities and growing rural landscapes. Their balance between operational capacity and deployment speed makes them a preferred choice for utilities focused on grid reinforcement, network expansion, and rapid electrification projects.

Demand for gas-insulated modular substations is also on the rise, with the segment anticipated to grow at a CAGR of 5.9% through 2034. Known for their compact design, high safety standards, and strong performance in dense environments, gas-insulated units have become essential in metropolitan areas and industrial zones. Their sealed enclosures protect critical components from harsh environmental factors, significantly reducing maintenance requirements and extending operational lifespan.

The United States Modular Substation Market reached USD 2.7 billion in 2024, driven by the country's push to modernize aging grid systems. With increasing electrification, renewable energy adoption, and a focus on decentralized power generation, modular substations are proving vital for boosting grid resilience and ensuring reliable power supply during extreme weather events. Key players leading the global market include ABB, Eaton Corporation, Siemens, General Electric, and Schneider Electric, all focusing on innovation, strategic partnerships, and expanding smart grid capabilities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Voltage, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Low

- 5.3 Medium

- 5.4 High

Chapter 6 Market Size and Forecast, By Insulation, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Air

- 6.3 Gas

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Commercial

- 7.3 Industrial

- 7.4 Utility

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Italy

- 8.3.5 Russia

- 8.3.6 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 India

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Turkey

- 8.5.4 South Africa

- 8.5.5 Egypt

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 CHINT Global

- 9.3 Doho Electric

- 9.4 Eaton

- 9.5 Federal Pacific

- 9.6 General Electric

- 9.7 Hitachi

- 9.8 LS Electric

- 9.9 Orecco Electric

- 9.10 Schneider Electric

- 9.11 Siemens

- 9.12 TGOOD International

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 121 Pages

- 納期

- 2~3営業日