|

市場調査レポート

商品コード

1740761

注射針の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Needle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 注射針の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月24日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

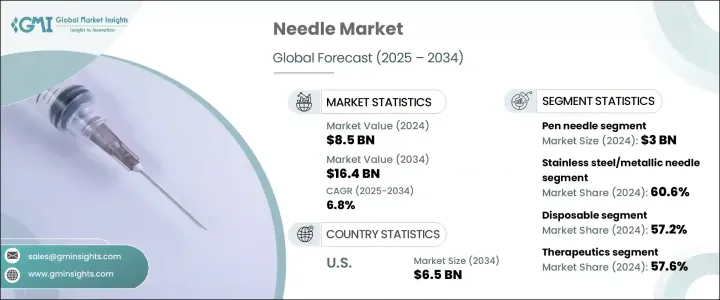

注射針の世界市場は、2024年には85億米ドルと評価され、心血管疾患、がん、呼吸器合併症、神経疾患などの慢性的な健康状態の蔓延の増加により、CAGR 6.8%で成長し、2034年には164億米ドルに達すると推定されています。

世界のヘルスケア情勢がバリューベースケアへとシフトする中、より良い患者の転帰を実現し、手技効率を高め、医療介入に伴うリスクを最小限に抑えることが重視されるようになっています。ヘルスケアプロバイダーと患者の両方が臨床の正確性、快適性、安全性を優先する中、高品質で安全設計された針への需要は高まり続けています。現代の医療現場は、診断からドラッグデリバリーまで、重要な手技をサポートする高度な注射針テクノロジーに依存しています。

注射針の小型化、先端部の鋭利化、安全機能の統合を推進する技術革新により、これらのデバイスは病院環境と在宅介護環境の両方で中心的な役割を果たしています。また、高齢者人口の拡大、低侵襲治療への嗜好の高まり、自己管理型治療の採用増加も市場の追い風となっています。感染症対策やヘルスケア従事者の安全に対する世界の意識が高まるにつれ、安全機構を強化したスマート注射針システムの必要性が一層高まっています。外来患者の処置、遠隔治療モデル、個別化医療の急増により、臨床アプリケーション全体で注射針製品の進化がさらに加速しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 85億米ドル |

| 予測金額 | 164億米ドル |

| CAGR | 6.8% |

今日のヘルスケアプロバイダーは、合併症を減らし、ケアの提供を合理化するために、精密に設計された針に依存しています。投薬、血液サンプルの採取、手術創の閉鎖など、これらのツールは現代の医療ワークフローに不可欠です。現在では、超極細チップ、シリコンコーティング、内蔵の安全機構が組み込まれ、ユーザーの使い勝手を向上させ、痛みや怪我を最小限に抑える設計となっています。これらの機能は、手技の正確性と患者の快適性を大幅に向上させ、高ストレスの医療環境において極めて重要です。ほとんどの注射針はシリンジやカテーテルと一緒に使用されるため、その互換性と信頼性は、シームレスなケアを確実に提供するために不可欠です。外来患者サービス、慢性疾患管理、在宅ケアの需要が高まる中、高度な注射針システムの市場は成長し続けています。日常的な注射や採血から複雑な外科処置まで、ヘルスケア専門家は進化するケアニーズに対応するため、信頼性が高く、無菌で生体適合性の高い注射針ソリューションに依存しています。

製品タイプ別に見ると、ペンニードル、皮下注射針、縫合針、歯科用針、採血針、鍼、その他があります。2024年には、ペンニードルの売上は30億米ドルを占め、2034年までのCAGRは6.7%と予測されています。ペンニードルの成長は、そのコスト効率、使いやすいデザイン、糖尿病治療におけるインスリン投与への高い採用率に起因しています。手先が不自由な患者や視力に問題のある患者、特に高齢者は、安全な自己注射のために特別に設計されたペンニードルが提供する手軽さと快適さから恩恵を受けています。

材料タイプ別では、ステンレス鋼および金属製注射針が2024年の市場シェアの60.6%を占めています。その人気は優れた耐食性に由来しており、高精度の手技や無菌状態での長時間の使用に理想的です。これらの材料は生体適合性に優れ、副作用を最小限に抑え、患者の安全性を高める。高温滅菌下での耐久性も、性能を損なうことなく繰り返しの使用をサポートし、病院と臨床の両方の環境で信頼できる選択肢となっています。

米国の注射針市場は、ヘルスケア技術の絶え間ない進歩と個別化治療への需要の高まりに後押しされ、2034年までに65億米ドルに達すると予測されています。特に糖尿病、がん、その他の慢性疾患による疾病負担が大きいため、先進的な注射針ベースのシステムに対する需要が高まっています。ヘルスケアイノベーター、研究機関、世界メーカーの強固なネットワークにより、米国は最先端の医療機器の製品開発と迅速な商業化でリードしています。支持的な規制の枠組み、ヘルスケアインフラへの政府投資の増加、安全性と効率性に関する国民の意識の高まりが、市場の上昇軌道にさらに貢献しています。在宅医療や遠隔医療が主流になるにつれて、ユーザーフレンドリーで安全性に最適化された注射針機器の使用は、さまざまな医療現場で急速に拡大しています。

世界の注射針業界の主要企業には、Thermo Fisher Scientific、Owen Mumford、B. Braun Medical、Terumo、Merck、Hamilton、Schreiner Group、Cardinal Health、Nipro、Novo Nordisk、Smiths Medical(ICU Medical)、Stryker、Becton, Dickinson and Company、Albert Davidなどがあります。これらの企業は、針刺し傷害のリスクを低減するため、安全機能を強化した人間工学に基づいた高精度の注射針システムの開発に注力しています。競争力を維持するため、主要企業は戦略的パートナーシップを通じて世界展開を拡大し、研究開発に多額の投資を行い、持続可能な製造方法を取り入れています。ヘルスケアのニーズが急速に進化する中、市場参入企業は、よりスマートで安全、かつコスト効率の高い注射針ソリューションを世界中に提供するため、積極的な技術革新に取り組んでいます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 慢性疾患の有病率の増加

- 注射用生物製剤の需要増加

- 針の設計における技術的進歩

- 外科手術の増加

- 業界の潜在的リスク&課題

- 代替的なドラッグデリバリー方法へのアクセス

- 厳格な規制要件

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術的情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別2021-2034

- 主要動向

- ペンニードル

- 皮下注射針

- 縫合針

- 採血針

- 歯科用針

- 鍼灸針

- その他の製品

第6章 市場推計・予測:材料別2021-2034

- 主要動向

- ガラス針

- プラスチック針

- ステンレス鋼/金属針

- ポリエーテルエーテルケトン(PEEK)針

第7章 市場推計・予測:利用形態別、2021-2034

- 主要動向

- 使い捨て

- 再利用可能/滅菌可能

第8章 市場推計・予測:用途別、2021-2034

- 主要動向

- 診断

- 採血

- 生検

- サンプル転送

- その他の診断

- 治療法

- 予防接種

- ドラッグデリバリー

- 美容処置

- インスリン投与

- 歯科

- 外科手術

- その他の治療法

第9章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- クリニック

- 診断センター

- 外来手術センター

- 在宅ケア環境

- 調査室

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- Albert David

- B. Braun Medical

- Becton、Dickinson and Company

- Cardinal Health

- Hamilton

- Merck

- Nipro

- Novo Nordisk

- Owen Mumford

- Schreiner Group

- Smiths Medical(ICU Medical)

- Stryker

- Terumo

- Thermo Fisher Scientific

The Global Needle Market was valued at USD 8.5 billion in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 16.4 billion by 2034, driven by the increasing prevalence of chronic health conditions such as cardiovascular diseases, cancer, respiratory complications, and neurological disorders. As the global healthcare landscape shifts toward value-based care, there's a growing emphasis on delivering better patient outcomes, enhancing procedural efficiency, and minimizing risks associated with medical interventions. The demand for high-quality, safety-engineered needles continues to rise as both healthcare providers and patients prioritize clinical precision, comfort, and safety. Modern medical practices depend on advanced needle technologies to support critical procedures, from diagnostics to drug delivery.

With innovations driving miniaturization, sharper needle tips, and integrated safety features, these devices play a central role in both hospital settings and home care environments. The market also benefits from the expanding elderly population, growing preference for minimally invasive treatments, and increasing adoption of self-administered therapies. As global awareness of infection control and healthcare worker safety intensifies, the need for smart needle systems with enhanced safety mechanisms becomes even more apparent. Surge in outpatient procedures, remote care models, and personalized medicine is further accelerating the evolution of needle products across clinical applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.5 Billion |

| Forecast Value | $16.4 Billion |

| CAGR | 6.8% |

Healthcare providers today rely on precision-engineered needles to reduce complications and streamline care delivery. Whether it's for administering medication, collecting blood samples, or closing surgical wounds, these tools are indispensable to modern medical workflows. Their designs now incorporate ultra-fine tips, silicone coatings, and built-in safety mechanisms to improve user experience and minimize pain or injury. These features significantly improve procedural accuracy and patient comfort, which is crucial in high-stress medical environments. Since most needles are used in conjunction with syringes or catheters, their compatibility and reliability are critical for ensuring seamless care delivery. With rising demand for outpatient services, chronic disease management, and home-based care, the market for advanced needle systems continues to grow. From everyday injections and blood draws to complex surgical procedures, healthcare professionals depend on reliable, sterile, and biocompatible needle solutions to meet evolving care needs.

Based on product type, the market includes pen needles, hypodermic needles, suture needles, dental needles, blood collection needles, acupuncture needles, and others. In 2024, pen needles accounted for USD 3 billion in revenue and are projected to grow at a CAGR of 6.7% through 2034. Their growth stems from their cost-efficiency, user-friendly design, and high adoption rate for insulin administration in diabetic care. Patients with limited dexterity or vision challenges, particularly elderly individuals, benefit from the ease and comfort provided by pen needles, which are specifically designed for safe self-injection.

The material type segment is led by stainless steel and metallic needles, which captured 60.6% of the market share in 2024. Their popularity comes from superior corrosion resistance, making them ideal for high-precision procedures and extended use in sterile conditions. These materials offer excellent biocompatibility, ensuring minimal adverse reactions and enhancing patient safety. Their durability under high-temperature sterilization also supports repeated usage without compromising performance, making them a reliable choice in both hospital and clinical environments.

The United States Needle Market alone is projected to reach USD 6.5 billion by 2034, fueled by continuous advancements in healthcare technologies and growing demand for personalized treatment approaches. The country's high disease burden-particularly from diabetes, cancer, and other chronic illnesses-drives strong demand for advanced needle-based systems. With a robust network of healthcare innovators, research institutions, and global manufacturers, the US leads in product development and rapid commercialization of cutting-edge medical devices. Supportive regulatory frameworks, increased government investment in healthcare infrastructure, and rising public awareness around safety and efficiency further contribute to the market's upward trajectory. As homecare and telehealth become more mainstream, the use of user-friendly, safety-optimized needle devices is expanding rapidly across various care settings.

Some of the leading players in the Global Needle Industry include Thermo Fisher Scientific, Owen Mumford, B. Braun Medical, Terumo, Merck, Hamilton, Schreiner Group, Cardinal Health, Nipro, Novo Nordisk, Smiths Medical (ICU Medical), Stryker, Becton, Dickinson and Company, and Albert David. These companies are focused on developing ergonomic, high-precision needle systems with enhanced safety features to reduce the risk of needlestick injuries. To stay competitive, key players are expanding their global reach through strategic partnerships, investing heavily in R&D, and embracing sustainable manufacturing practices. With healthcare needs evolving rapidly, market participants are actively innovating to deliver smarter, safer, and more cost-effective needle solutions across the globe.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Growing demand for injectable biologics

- 3.2.1.3 Technological advancements in needles design

- 3.2.1.4 Rising number of surgical procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Access to alternative drug delivery methods

- 3.2.2.2 Stringent regulatory requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Trump administration tariffs

- 3.6.1 Impact on trade

- 3.6.1.1 Trade volume disruptions

- 3.6.1.2 Retaliatory measures

- 3.6.2 Impact on the Industry

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.2.1.1 Price volatility in key materials

- 3.6.2.1.2 Supply chain restructuring

- 3.6.2.1.3 Production cost implications

- 3.6.2.2 Demand-side impact (selling price)

- 3.6.2.2.1 Price transmission to end markets

- 3.6.2.2.2 Market share dynamics

- 3.6.2.2.3 Consumer response patterns

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.3 Key companies impacted

- 3.6.4 Strategic industry responses

- 3.6.4.1 Supply chain reconfiguration

- 3.6.4.2 Pricing and product strategies

- 3.6.4.3 Policy engagement

- 3.6.5 Outlook and future considerations

- 3.6.1 Impact on trade

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pen needles

- 5.3 Hypodermic needles

- 5.4 Suture needles

- 5.5 Blood collection needles

- 5.6 Dental needles

- 5.7 Acupuncture needles

- 5.8 Other products

Chapter 6 Market Estimates and Forecast, By Material 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Glass needles

- 6.3 Plastic needles

- 6.4 Stainless steel/metallic needles

- 6.5 Polyetheretherketone (PEEK) needles

Chapter 7 Market Estimates and Forecast, By Usage Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Disposable

- 7.3 Reusable/Sterilizable

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Diagnostics

- 8.2.1 Blood collection

- 8.2.2 Biopsy

- 8.2.3 Sample transfer

- 8.2.4 Other diagnostics

- 8.3 Therapeutics

- 8.3.1 Vaccination

- 8.3.2 Drug delivery

- 8.3.3 Aesthetic procedures

- 8.3.4 Insulin administration

- 8.3.5 Dental

- 8.3.6 Surgical

- 8.3.7 Other therapeutics

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Clinics

- 9.4 Diagnostic center

- 9.5 Ambulatory surgical centers

- 9.6 Home care setting

- 9.7 Research laboratories

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Albert David

- 11.2 B. Braun Medical

- 11.3 Becton, Dickinson and Company

- 11.4 Cardinal Health

- 11.5 Hamilton

- 11.6 Merck

- 11.7 Nipro

- 11.8 Novo Nordisk

- 11.9 Owen Mumford

- 11.10 Schreiner Group

- 11.11 Smiths Medical (ICU Medical)

- 11.12 Stryker

- 11.13 Terumo

- 11.14 Thermo Fisher Scientific