|

市場調査レポート

商品コード

1740743

アミンベースの炭素回収市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Amine-Based Carbon Capture Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| アミンベースの炭素回収市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月23日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

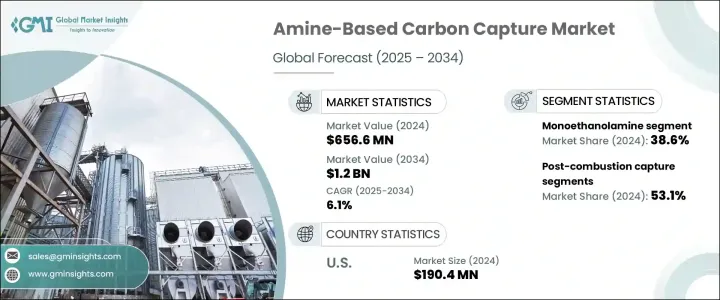

世界のアミンベースの炭素回収市場は、2024年には6億5,660万米ドルとなり、2034年にはCAGR 6.1%で成長して12億米ドルに達すると推定されています。

各国が野心的なカーボンニュートラル目標を設定する中、効率的でスケーラブル、かつ費用対効果の高い炭素回収技術に対する需要は高まり続けています。アミンベースの炭素回収は、最も信頼できるソリューションの一つとして台頭しており、既存のインフラを一新することなく排出量を大幅に削減する実用的な方法を提供しています。企業、政府、研究機関は、エネルギーおよび製造セクターを変革する可能性を認識し、先進的なアミン溶剤およびシステムの開発に多額の投資を行っています。

この市場を牽引しているのは、規制当局からの圧力だけでなく、持続可能な技術に対する投資家の関心の高まりでもあります。カーボンプライシングメカニズムが強化され、脱炭素化が企業戦略の中心になるにつれ、企業は持続可能性へのコミットメントをサポートしながらコンプライアンスを確保できる、信頼性の高い長期的ソリューションを求めています。さらに、循環型炭素経済への高まりは、CO2を回収し、リサイクルし、さらには永久的に除去する技術の必要性を強めています。このような状況において、アミンベースの炭素回収は実績のある性能と柔軟性を提供します。今日、産業規模で展開することが可能であると同時に、炭素利用・貯蔵システムとの統合など、技術革新のためのプラットフォームとしても機能します。材料科学、プロセス工学、自動化の進歩により、この市場は急速な拡大を続け、新規参入企業にも既存企業にも大きなビジネスチャンスを提供すると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 6億5,660万米ドル |

| 予測金額 | 12億米ドル |

| CAGR | 6.1% |

アミンベースの捕捉技術は、特に排ガスに二酸化炭素が多く含まれる燃焼後の用途において、その効率の高さで知られています。このプロセスは、アミン水溶液に依存してCO2を化学的に吸収し、再生段階で放出するため、溶媒を連続サイクルで再利用することができます。この技術は、既存の石炭火力発電所やガス火力発電所、その他の産業施設の改修に特に適しており、大規模な改修を必要としないです。気候変動目標を達成し、産業界の二酸化炭素排出量を削減するという緊急性の高まりが、溶剤の性能向上、CO2負荷能力の向上、再生に必要なエネルギーの削減に重点を置き、この分野の技術革新を後押ししています。

この分野で最も将来を見据えた開発のひとつが、アミンで強化した固体吸着剤を用いた直接空気捕捉です。排出源で回収するよりもエネルギー集約的ではあるが、この技術は大気から直接CO2を抽出することで、排出量を逆転させる可能性を秘めています。ネットマイナスエミッション戦略に注目が集まる中、このアプローチは気候変動技術への投資家や政府の間で注目を集めています。

最近の研究開発では、アミン系溶剤の選択性と反応性を向上させることに重点を置いており、捕捉効率を高めながら全体的な運用コストを削減することを目指しています。これには、熱安定性が高く、分解率が低い新しい溶剤の開発も含まれます。技術革新は、化学技術者、環境科学者、クリーンエネルギーの専門家を含む分野横断的な協力によって推進されており、これらすべてが炭素回収システムの大規模展開の実現可能性を高めるために取り組んでいます。こうした進歩は、セメント、鉄鋼、精製など、電化が脱炭素化への実現可能な道筋ではない難燃セクターにおいて特に重要です。

モノエタノールアミン(MEA)セグメントは、2024年の市場シェアで38.6%を占めました。二酸化炭素への強い親和性と安定したカルバマート化合物を形成する能力で知られるMEAは、化学吸収システムの要であり続けています。その信頼性、運用の安定性、広く入手可能なことから、特にレガシーエネルギーインフラストラクチャにおける燃焼後回収の有力な選択肢となっています。

燃焼後回収技術は2024年に53.1%のシェアで市場をリードしたが、その主な理由は既存システムへのシームレスな統合です。操業の中断を最小限に抑えながら炭素排出を削減できるため、産業界はこの方法を好んでいます。数十年にわたるパイロット試験、商業プロジェクト、工学的改良に支えられ、燃焼後回収は最も実用的で広く採用されているソリューションであり続けています。

米国のアミンベースの炭素回収市場は、2024年に1億9,040万米ドルと評価されました。税額控除などの連邦政府の優遇措置と柔軟な州レベルの規制が相まって、米国は炭素回収技術革新の主要市場となっています。環境保護庁(Environmental Protection Agency)と州当局の委任によるクラスVI坑井の迅速な許可は、プロジェクトのスケジュールを短縮し、投資家の信頼を高めており、導入をさらに加速させています。

業界の主要企業には、 Toshiba Energy Systems & Solutions, Linde PLC, Mitsubishi Heavy Industries, Fluor Corporation, Koch-Glitsch, Shell CANSOLV, BASF SE, Pentair, Carbon Clean, and GEA Groupなどがあります。これらの企業は、溶剤再生効率の向上、モジュール式炭素回収装置の立ち上げ、パイロットプロジェクトから本格的な商業運転へのスケールアップに注力しています。これらの企業の努力は、幅広い産業用途における次世代アミンシステムのコスト削減と拡張性の向上に役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 主要メーカー

- 販売代理店

- 業界全体の利益率

- 供給の混乱

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国

- 主要輸入国

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 石炭火力発電所における燃焼後CO2回収におけるモノエタノールアミンの導入拡大

- 天然ガス脱硫用メチルジエタノールアミンブレンドの技術的改良

- アミン官能化固体吸着剤を使用した直接空気回収(DAC)への投資増加

- 業界の潜在的リスク&課題

- 溶媒再生に伴う高いエネルギーペナルティと運用コスト

- 特定のアミンの腐食性により、工場のインフラに高価な材料が必要になる

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:アミンの種類別、2021–2034

- 主要動向

- モノエタノールアミン

- ジエタノールアミン

- メチルジエタノールアミン

- トリエタノールアミン

- その他

第6章 市場推計・予測:用途別、2021–2034

- 主要動向

- 燃焼後回収

- 燃焼前回収

- 直接空気回収

- その他

第7章 市場推計・予測:地域別、2021–2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第8章 企業プロファイル

- BASF SE

- Carbon Clean

- Fluor Corporation

- GEA Group

- Koch-Glitsch

- Linde PLC

- Mitsubishi Heavy Industries

- Pentair

- Shell CANSOLV

- Toshiba Energy Systems &Solutions

The Global Amine-Based Carbon Capture Market was valued at USD 656.6 million in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 1.2 billion by 2034, as global efforts ramp up to combat greenhouse gas emissions, particularly carbon dioxide released from power plants and heavy industries. As countries set ambitious carbon neutrality goals, demand for efficient, scalable, and cost-effective carbon capture technologies continues to rise. Amine-based carbon capture is emerging as one of the most dependable solutions, offering a practical way to significantly reduce emissions without overhauling existing infrastructure. Companies, governments, and research institutions are heavily investing in the development of advanced amine solvents and systems, recognizing their potential to transform the energy and manufacturing sectors.

This market is driven not only by regulatory pressure but also by growing investor interest in sustainable technologies. As carbon pricing mechanisms tighten and decarbonization becomes central to corporate strategies, businesses are seeking reliable, long-term solutions that ensure compliance while supporting sustainability commitments. Moreover, the growing push for circular carbon economies is reinforcing the need for technologies that capture, recycle, and even permanently remove CO2 ,In this context, amine-based carbon capture offers a proven track record of performance and flexibility. It can be deployed at industrial scale today while also serving as a platform for innovation, including integration with carbon utilization and storage systems. With advancements in material science, process engineering, and automation, this market is expected to continue expanding rapidly, offering significant opportunities for new entrants and established players alike.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $656.6 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 6.1% |

Amine-based capture technology is known for its high efficiency, particularly in post-combustion applications where flue gases are rich in carbon dioxide. The process relies on aqueous amine solutions to chemically absorb CO2 which is then released during the regeneration phase, allowing the solvent to be reused in continuous cycles. This technology is especially well-suited for retrofitting existing coal and gas-fired power plants, as well as other industrial facilities, without the need for extensive modifications. The increasing urgency to meet climate targets and reduce industrial carbon footprints is pushing innovation in this field, with an emphasis on improving solvent performance, increasing CO2 loading capacity, and reducing the energy required for regeneration.

One of the most forward-looking developments in this space is direct air capture using solid sorbents enhanced with amines. Although more energy-intensive than capturing emissions at the source, this technology holds the potential to reverse emissions by extracting CO2 directly from the atmosphere. As attention shifts toward net-negative emission strategies, this approach is gaining traction among climate tech investors and governments alike.

Recent R&D efforts are focused on improving the selectivity and reactivity of amine-based solvents, aiming to reduce overall operational costs while enhancing capture efficiency. This includes the development of new solvent formulations with higher thermal stability and lower degradation rates. Innovations are being driven by cross-sector collaboration involving chemical engineers, environmental scientists, and clean energy specialists, all working toward making carbon capture systems more viable for large-scale deployment. These advancements are particularly important in hard-to-abate sectors like cement, steel, and refining, where electrification is not a feasible path to decarbonization.

The monoethanolamine (MEA) segment accounted for a dominant 38.6% market share in 2024. Known for its strong affinity to carbon dioxide and its ability to form stable carbamate compounds, MEA remains a cornerstone of chemical absorption systems. Its reliability, operational consistency, and widespread availability have made it a go-to choice for post-combustion capture, particularly in legacy energy infrastructure.

Post-combustion capture technologies led the market with a 53.1% share in 2024, largely because of their seamless integration into existing systems. Industries favor this method as it allows them to reduce carbon emissions with minimal disruption to operations. Supported by decades of pilot testing, commercial projects, and engineering improvements, post-combustion capture continues to be the most practical and widely adopted solution.

The United States Amine-Based Carbon Capture Market was valued at USD 190.4 million in 2024. Federal incentives like tax credits, coupled with flexible state-level regulations, have made the U.S. a leading market for carbon capture innovation. Fast-track permitting for Class VI wells by the Environmental Protection Agency and delegated state authorities has shortened project timelines and boosted investor confidence, further accelerating deployment.

Key industry players include Toshiba Energy Systems & Solutions, Linde PLC, Mitsubishi Heavy Industries, Fluor Corporation, Koch-Glitsch, Shell CANSOLV, BASF SE, Pentair, Carbon Clean, and GEA Group. These companies are focusing on enhancing solvent regeneration efficiency, launching modular carbon capture units, and scaling up pilot projects into full-scale commercial operations. Their efforts are helping to drive down costs and improve the scalability of next-generation amine systems across a wide range of industrial applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Key manufacturers

- 3.1.2 Distributors

- 3.1.3 Profit margins across the industry

- 3.1.4 Supply disruptions

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic Industry Responses

- 3.2.4.1 Supply Chain Reconfiguration

- 3.2.4.2 Pricing and Product Strategies

- 3.2.4.3 Policy Engagement

- 3.2.5 Outlook and Future Considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major Exporting Countries

- 3.3.2 Major Importing Countries

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increasing deployment of monoethanolamine in post-combustion CO2 capture in coal-fired power plants

- 3.7.1.2 Technological improvements in methyldiethanolamine blends for natural gas sweetening

- 3.7.1.3 Rising investments in direct air capture (DAC) using amine-functionalized solid sorbents

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High energy penalty and operational costs associated with solvent regeneration

- 3.7.2.2 Corrosiveness of certain amines, requiring expensive materials for plant infrastructure

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Type of Amines, 2021–2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Monoethanolamine

- 5.3 Diethanolamine

- 5.4 Methyldiethanolamine

- 5.5 Triethanol amine

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Application, 2021–2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Post-combustion capture

- 6.3 Pre-combustion capture

- 6.4 Direct air capture

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Region, 2021–2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 BASF SE

- 8.2 Carbon Clean

- 8.3 Fluor Corporation

- 8.4 GEA Group

- 8.5 Koch-Glitsch

- 8.6 Linde PLC

- 8.7 Mitsubishi Heavy Industries

- 8.8 Pentair

- 8.9 Shell CANSOLV

- 8.10 Toshiba Energy Systems & Solutions